All firms benchmark their performance. It’s relatively straightforward to compare your investment returns to the S&P 500, Dow Jones, Investment-Grade credit, or simply government bonds.

All of these are simple because they have clear indices. As such, you can look at the level of the S&P 500 on Day X and Day Y, and come up with a return that is readily comparable to your particular investment, whether you invested in a stock, a bond, a car, or pair of shoes. As long as you compare your entry and exit points, it’s quite easy to conclude “I would have done better putting $100 into the S&P than this pair of shoes”.

We all know you are probably always financially better off putting $100 into the S&P than in a pair of shoes. Case in point, however, you would probably benchmark your shoe investment to a shoe index (if there was one) to know if you outperformed the shoe market.

Taking that analogy to the world of interest rate derivatives, would it not make sense to compare your performance in trading IR Swaps to something more related, such as the performance of a benchmark IR swap?

INSPIRATION & BACKTESTING

The idea of an index came to us from a client that wanted to backtest various trading strategies. For example, trading the front-month MAC swap and rolling it to maintain roughly a 5 year exposure.

The solution to that specific problem was quite easy. Just feed our CHARM API some trade and a series of value dates, and we’ll tell you exactly how that trade, strategy, or portfolio performed. Literally a few lines of script and we can retrieve the output on my 12-trade portfolio in well under 50 milliseconds per day (via the cloud), so my backtest to 2013 took roughly 30 seconds to compute.

SMARTER IDEA – AN INDEX

It struck us, however, that really all we need to do is to come up with an index that would compute the cumulative daily returns on various standard swaps, and you could then readily compare returns based upon any “standard swap”, given an any entry and exit point. More beautifully, if we had enough indices (eg 2Y, 5Y, 10Y, etc) we could very quickly look at how common strategies such as spreads would return over time.

The best products to use in such an index would require a product that could simulate getting in and out (“rolling”) to generally maintain the duration of the strategy. The clear choice in Interest Rate Swaps is IMM Market Agreed Coupon (MAC) swaps. These are generally liquid, and we can nicely assume that rolling these contracts will be cost-effective. Most importantly, because they have standard coupons, we know they will readily compress at the clearing house (a buy will negate a sell, unlike spot starting swaps).

I was intrigued to see that the MAC swaps have changed slightly since 2013; for example there was initially a 6 year swap in June 2013, but no 12 year swap. So I chose to begin my backtest back in late 2014 when MAC swaps seem to have stuck with the same tenors of 1, 2, 3, 4, 5, 7, 9, 10, 12, 15, 20, and 30 years. And we backtested all 12 of these swaps for USD.

Some final points before we see the performance:

- We initially chose a fixed swap notional of 10 million USD. We could have alternately begun with a fixed DV01 of say 10k, however I wanted to make sure that the strategy would nicely compress each roll quarter (out of 10mm front month, into the new front month). And notional is very easy to work with when comparing returns as notional will not change from entry to exit points.

- The strategy chooses to roll the swap 7 days prior to the IMM date. We checked SDRView records to confirm that MAC swap rolls tend to occur generally evenly the calendar week prior to the IMM date, so this seems fair.

- Each new swap is put on at 0 NPV. Don’t forget these MAC swaps have standard coupons, so there is a premium on MAC swaps that we set to market rates.

- We considered expressing the results in basis points, or indexed around a “par” rate of 100. However for simplicity, we have left it measured in MTM. Hence the index begins at 0, and can go as negative as it can go positive.

- No consideration was given to funding / carry costs, such as clearing fees and margins. I believe this is fair.

- When MAC coupons changed (as they did for March and June 2015) we used the more-up-to-date coupons as they were available by our entry date and presumably the most liquid.

RESULTS

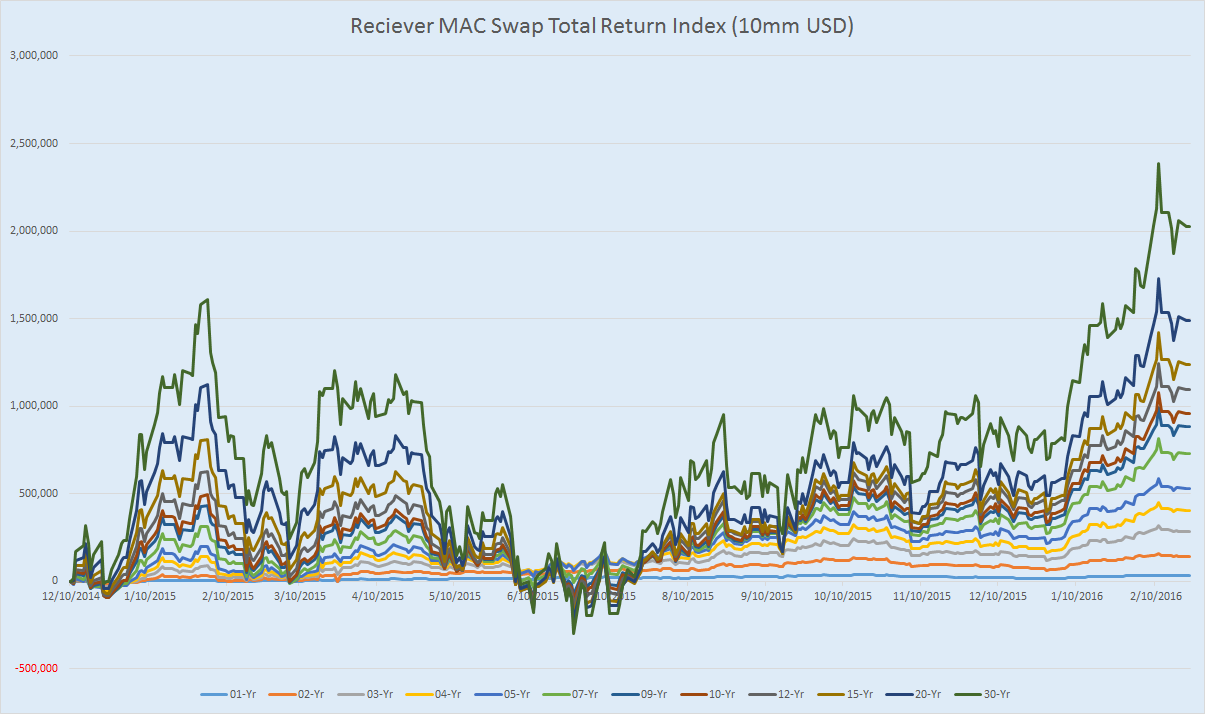

The following chart reflects the performance of all 12 indices for $10 million notional MAC swaps since 10-Dec-2014:

Interesting that a 10mm 30Y Reciever USD swap struck in December 2014 and rolled until today would have accumulated over 2mm USD of gains. Conversely, a 30Y Payer would have lost 2mm USD. So much for thinking that rates can only go up!

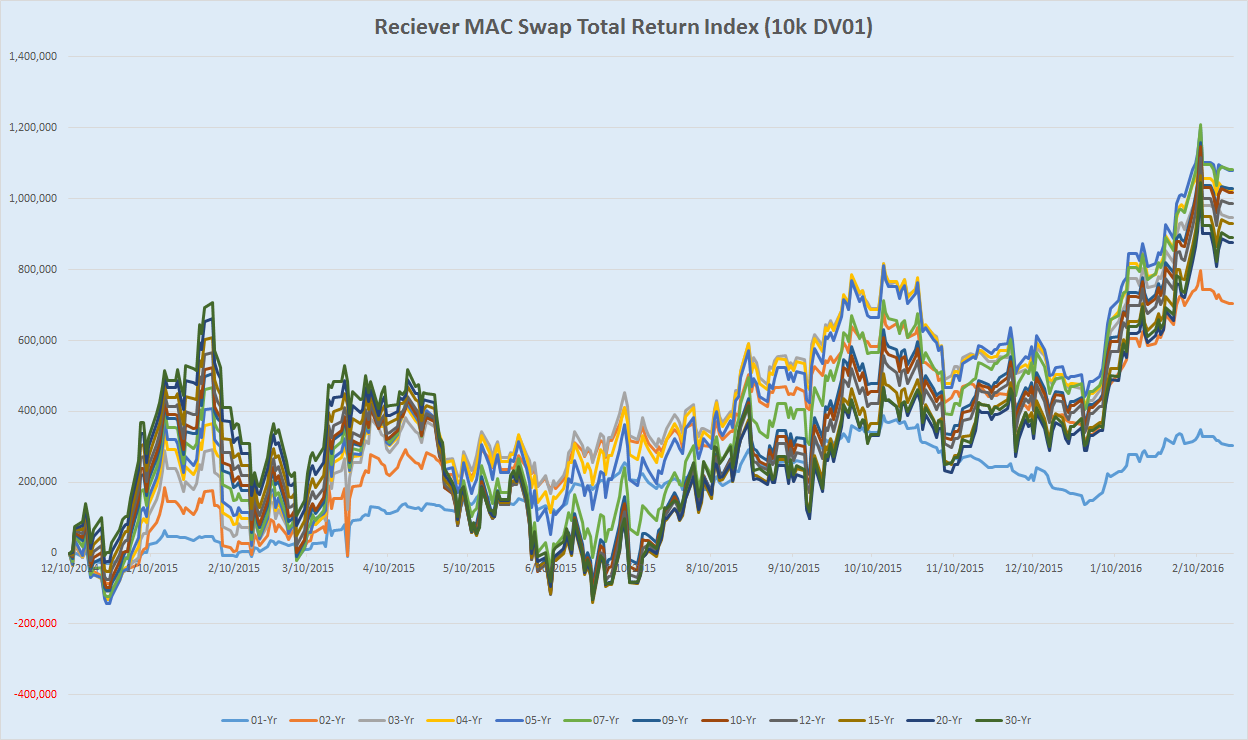

Clearly when a 30Y swap and 1Y swap have the same notional, the 30Y should always outperform, given its DV01 is maybe 25x or so larger. So, if we throw away the notion of constant notional, and target DV01 instead, we see smoother, more consistent returns across products. So here is the return on 10k DV01 sized swaps over time:

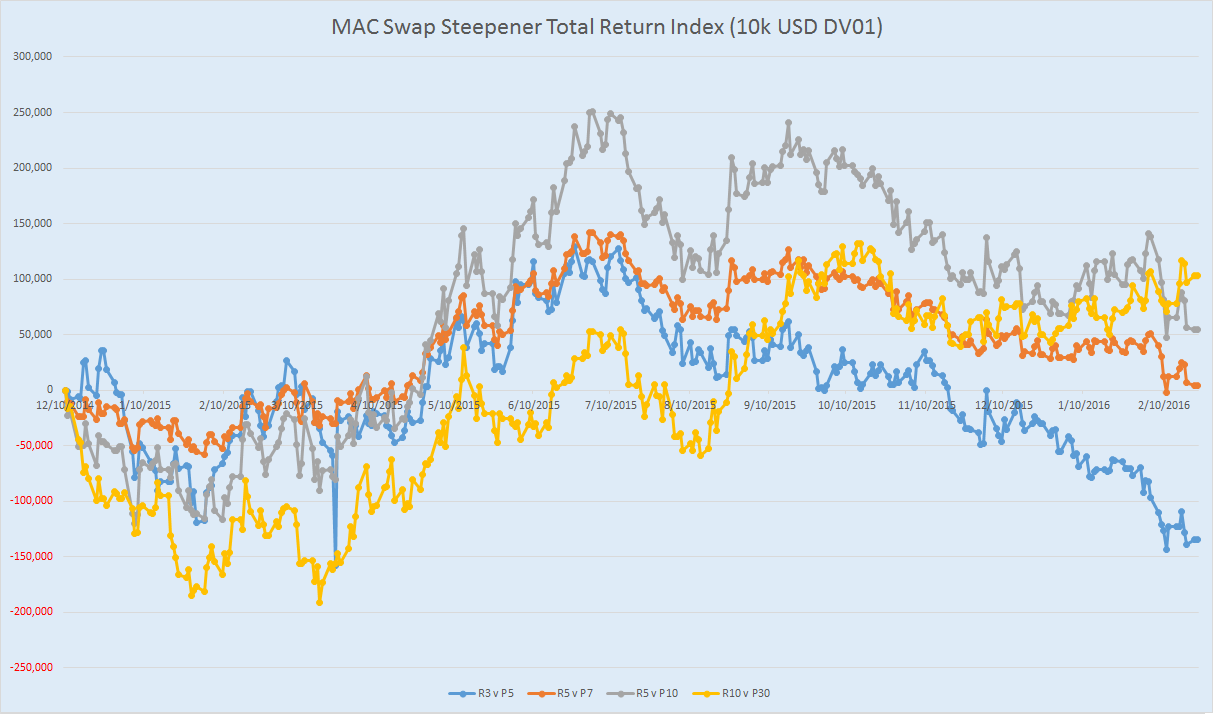

We can also leverage these indices now to benchmark the most common strategies such as spreads. Here are the most common Curve Steepeners (3v5, 5v7, 5v10, and 10v30):

Of course, if you want to benchmark your book or strategy over the past month or year (or any time period), all you need do is pluck out the index levels for the entry and exit points, measure the relative returns, and multiply by your investment amount (50k DV01 as opposed to 10k in the index).

SUMMARY

After going through this analysis, I’m scratching my head as to why I have not yet seen anything like this for interest rate swaps. Surely these would be useful metrics to have at hand.

If you can answer that – please leave us a comment below. And if you find this useful or want to learn more, please contact us so we can help.

Could also benchmark against a constant maturity IRS future?

http://www.eurexchange.com/exchange-en/products/gmex-irs-constant-maturity-futures

Thanks for the comment. Yes the GMEX CMS futures are interesting. We support the idea of CMS futures, however unfortunately, based upon our CCPView data and like many swap futures, there is no open interest in GMEX futures at Eurex yet. I would think even with CMS as a benchmark, there are valid reasons to benchmark against the most common OTC strategies that leverage either IMM/MAC or even spot starting swaps. Both could coexist.

1. You could only benchmark against futures for very standard instruments – those for which there exist IRS future “equivalents”. The idea of a swap index is more general – you can create an index for any instrument/package. Say 1yf1y, 5yf5y, 3yf(2s10s)…

2. I also like the swap index idea better because it would be exactly what the market trades: since people trade swaps a lot more than they do swap futures, a swap index is more compelling than a future-derived one

Per this TED talk there IS a market index for sports shoes, and it can beat the S&P…

https://youtu.be/1lxRXQRa72Q

Hah, yes I stand corrected then! I had no idea of the sneaker underworld. I suppose I have just never been to a shoe store at 8am on a Saturday.