The final no-action relief of SEF packages is due to expire November 15, 2014. Many folks have turned to us asking if this will be something that significantly impacts the amount of trades being dealt On-SEF.

BIT OF HISTORY

Back when the no-action relief was first given in May, the November 15 date was by far the longest relief given. Other packages were given a matter of weeks to months before they became MAT, but Invoice Spreads were deliberately given a seemingly long 6 months. Why such a delay for these trades?

I had appreciated that because we’re talking about packages from two separate markets (OTC swap packaged with Listed Futures), that it could be quite complex. Since then, I’ve also been hearing that it’s simply not possible under current laws. But before I try wrapping my head around all of that, I wanted to first understand these products better, and assess just how many of these packages we can see.

THE BASICS OF INVOICE SWAPS

Fundamentally, invoice swaps are a flavor of spread trades, whereby the investor is taking a view on the spread between US government debt and a similarly dated OTC interest rate swap. Essentially a play on the riskiness of the US government vs that of banks.

There are a few manifestations of playing this spread, be it:

- Spread-over-treasuries. Cash bond vs spot starting, standard tenor, OTC swap, which have been MAT’d in June. This is the garden variety for the inter-dealer market.

- Matched maturity cash bonds vs swaps. A variation of the above but where the swaps maturity date matches that of the treasury. The start dates can be either spot or IMM. This is the garden variety for hedge funds.

- Invoice spreads. OTC swap with effective date matching the delivery date of a CME bond future, and a maturity date matching that of the future’s CTD bond.

Liquidity and cost-effectiveness would seem to determine which choice the investor takes. For example, ERIS offers what I would presume to be a very cost effective play on invoice spreads whereby both legs are futures (a CME bond future with an Eris Flex swap future).

SOME DATA

So how big is this market? I pulled the August 2014 data for USD Fixed/Float swaps from SDRView, for which there were a total of 25,871 matching swap trades reported. That’s the entire USD market in the month.

BRIEF DIVERSION

Peter Madigan of Risk Magazine published an article this past week claiming that ISDA is not finding the gurth of forward starting swaps that we’ve reported on a couple occasions. The facts are still there in the August numbers I pulled. 33% of these 25,000+ trades are not a MAT’able start, and when looking at what’s traded Off-SEF, that number is 71%. I’ll also repeat what I said in my detailed post on this topic: this scale of forward starting swap behavior existed before SEF’s started.

BACK TO DATA

From the universe of 25,871 trades in August, I have first pulled out the 3,652 trades that are “Previous” starting, as these can generally be assessed to be from compression or similar process.

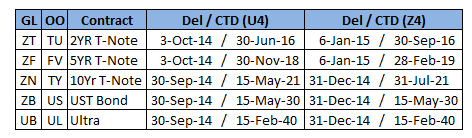

I then looked for swaps matching the following dates, expressed as “Effective Date / Maturity Date” which would match the Futures delivery date and underlying CTD maturity date:

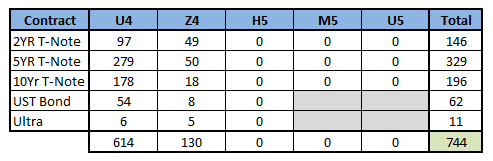

Out of the 22,219 trades in the analysis, I found 744 hits, or just over 3% of the trades done in August. The vast majority of these trades are in the first futures contract (614 trades), and nearly half of them against the 5Yr T-Note Future. I was not able to find any for the 3rd, 4th, or 5th futures contract. Note that the Treasury Bond and Ultra bond only go out to 3 contracts:

Interesting to note that of these 744 trades, 163 of them were flagged as blocks.

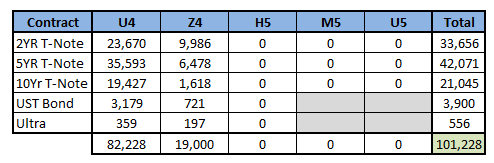

Finally, in Notional terms:

538

So will these be SEF-tradeable in November? The confusion seems to revolve around CME rule 538.

When a futures/OTC package is traded, it is done away from the exchange. This requires an “EFR” (I liken to an EFP) to get the futures registered at CME. That all works. However the new CME rule 538 says you can not do an EFR if it is a futures trade that was executed with a SEF-eligible swap.

Therein lies the rub. Dodd-Frank is saying you have to execute the OTC leg with the future. CME is saying you can’t register a future that was executed with an OTC leg.

Rule 538 went into effect in August. Prior to this, SEF’s like Tradition actually listed such OTC/Futures packages on their SEF. Alas they can no longer do that.

I presume the only reason this has not been a larger issue to date is that, except in extremely rare cases, the underlying swap for invoice spreads are not MAT, and hence not required to be executed on SEF.

SUMMARY

- Invoice spreads are one way to express views on the spread between US debt and swaps

- Invoice spreads are a significant portion of the market (3%+)

- What is going to happen come November? Particularly if more products become MAT’d, this could really be an issue.