- We will follow what is trading in Interest Rate Derivatives markets across the election, with the latest post at the top of the blog.

- As a reminder, we have seen record volumes trading in Swap markets so far this year.

- Our 2016 blog suggests that trading was 5x more active on Election Day than average.

- 10Y and 30Y outrights, 5Y spreadovers and 5Y-30Y curve trades were the most active back in 2016.

Final Post

Below you will see our updates throughout the day. As you can see, the action ended up a touch “samey” – there wasn’t the volatility that we saw back in 2016. However, we ended the day with 5,200 trades. That beat August 5th (which I think was the previous SDR record) by a whole….six trades! Count ’em….

The market moves were fairly consistent throughout the day, apart from Spreadovers ended up tighter on the day, and traded in 1.4-2.1 times their normal volumes. But it sure was a bear steepener of a move, albeit with 30Y coming back (I guess following the digestion of the auction supply).

I won’t talk about notional or DV01 volumes too much. This is because there have been new Block Thresholds implemented – see CFTC announcement here. I’ve covered this a few times on the blog (see here) but the new sizes came into force on October 7th. Despite knowing they were coming, it doesn’t make it any easier to compare volumes pre-change and post-change!

15:05

The move is now a bit more “bear” and a little less “steepener” since the last update. 30Y yields back to the highs of the day, but 5Y30Y has “only” steepened by 5.6 basis points now:

We’ve had over 2,700 trades reported, with $80m gross DV01. On those crazy August days we were seeing over 5,000 trades reported – so activity levels are not that crazy yet, but equally we have plenty of the day left to go…..

13:00

Some of the moves are now beginning to retrace. 30Y yields are back to 17 basis points higher on the day, but the curve remains as steep as ever. The retracement has seen decent volumes trade, with $7m in gross DV01 traded in the past hour:

5Y10Y has now seen over $1m in DV01 transacted, with 2Y10Y nearly there too. That is way over the ~250k DV01 we expect to see each day in these spreads:

12:15

Halfway through my shift for the day, and the most active butterflies traded today are 5Y-10Y-30Y and 5Y-7Y-10Y, each with over $400k DV01 traded in the belly:

For curve switches, 5Y10Y activity has now overtaken 2Y10Y. 5Y30Y has also joined the club with over $800k DV01 traded:

For Spreadovers, 5Y has already traded it’s typical average daily volume, with over $2m DV01. 10Y is normally more active than 5Y but is lagging slightly today. Spreadovers give a good indication of how busy dealers are with this move:

Midday

The move does not appear to be losing momentum, with 30Y yields now 20 basis points higher on the day. 5Y Swap Spreads have seen a large amount of volume, but are only lower by 1bp compared to yesterday. The bear steepener is still very much the theme, with 5Y30Y continuing to steepen.

The pace of trading is impressive – another 200+ trades since the past update, bringing us to 1,462 trades and $37.7m DV01. If I include list trading, that total is over $40. 6m in risk traded so far. And it’s barely lunchtime! Since the beginning of the sell-off in mid-September, we have averaged $107m in gross DV01 traded each day.

10:45am

We are now 1,250+ trades into the trading day, with over $32m in DV01 traded. The bear steepener has been the theme of the London morning session, with 30Y rates 15bp higher and 5Y30Y 8 basis points steeper:

5Y10Y and 2Y10Y are by far the most active curve spreads in play, with 5Y10Y30Y the most active fly.

07:35am (6th November)

US Swap Spreads are continuing their journey into deeper and deeper negative territory. 30Y spreads have been on this journey all year, starting at -65bp at the beginning of January, and now 20 basis points lower on the year. They are another 1 basis point lower in early trading today;

07:30am (6th November)

The steepening of the curve is becoming far more apparent now. In the past ~45mins we’ve seen another 150 trades and $3m in gross DV01 trade – that is a lot of activity! 5y30y now 5 basis points steeper, and 30Y has already traded 90% of its typical daily volume (ADV).

07:00am (6th November)

It has been a real 24 hour market overnight in USD swaps. We have already had 728 trades reported, totalling $38bn in notional and $17m in DV01. 10Y the most active to date:

Yesterday’s VWAP for 10Y swaps was 3.81%, so we are 10 basis points higher so far today compared to the average trading levels yesterday. We are nearly 14bp higher compared to the close:

5y10y is very active relative to typical trading amounts, but we’ve actually seen the most trades in 2Y-10Y and 5Y-10Y-30Y this time round:

15:30 London (5th November)

As we set up for tomorrow’s trading activity, we are seeing unusually large amounts of activity in 10Y15Y30Y Butterfly so far today;

Showing;

- We’ve had 13 trades totalling nearly $500k DV01 in 10Y15Y30Y already today.

- The prices vary because not all of these are spot-starting flies. The range of spot trades is very tight, 22.25-22.375bp (i.e. 1/8th of a bp).

- 10Y12Y15Y is also unusually active.

We will update this blog with what is unusually active, and track price moves accordingly. Stay tuned!

11am London (5th November)

Ahead of the results (and any contests to the results), we would be well served to remind ourselves of the set-up going into the election itself. So, here is a quick reminder of trading conditions in USD swaps during 2024:

In terms of volumes traded, 2024 has been a record year in USD swaps;

I’ve looked at these volumes in more detail in September’s blog “USD Rates – What’s New” and October’s blog “RFR Adoption Q3 2024” covers the DV01. It is also worth noting that these record volumes are not USD specific – EUR Rates are also trading in record volumes, as shown in last week’s blog “EUR Rates – What’s New“.

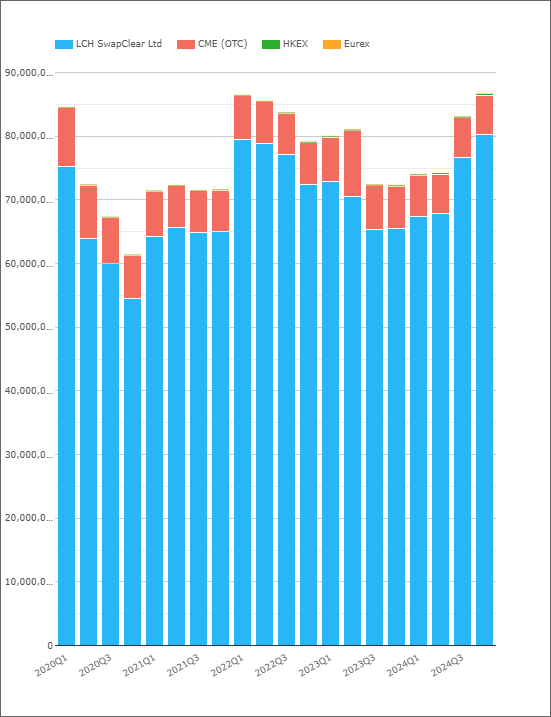

Despite banks best efforts to compress everything away (with a particular eye on their upcoming end of year GSIB scores….), this means that we head into the election with Open Interest in USD swaps at an all time high above $86Trn:

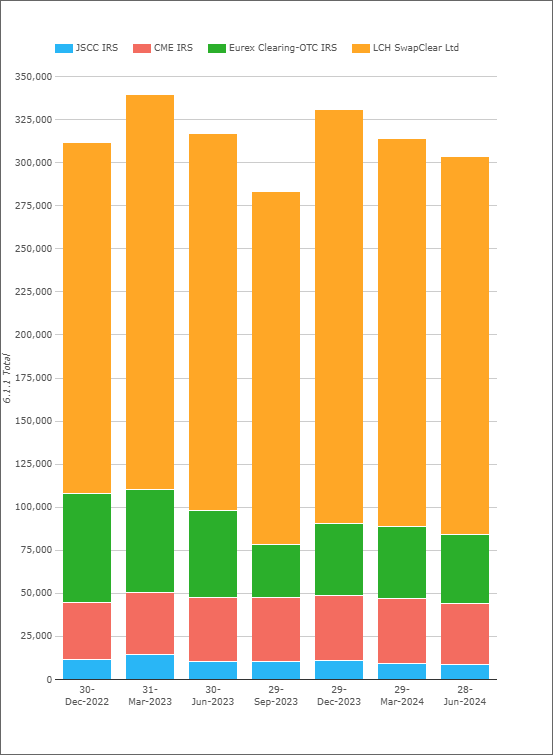

Open Interest is a pretty good measure of the risk at a CCP, but it is not perfect. It is, however, more timely than the Initial Margin disclosures we have, that suggest over $300bn was tied up in Initial Margin related to Swaps as at 28th June 2024.

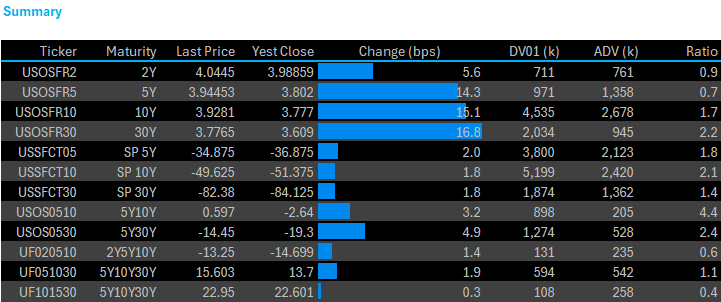

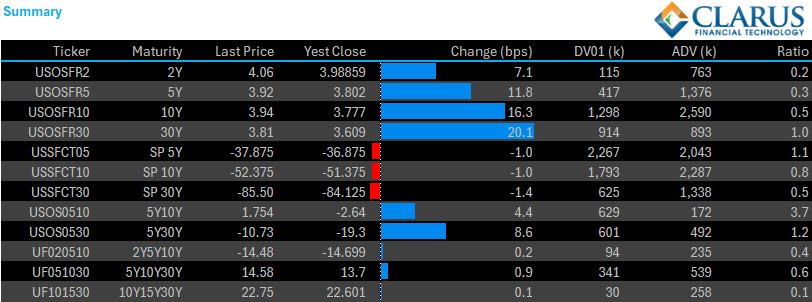

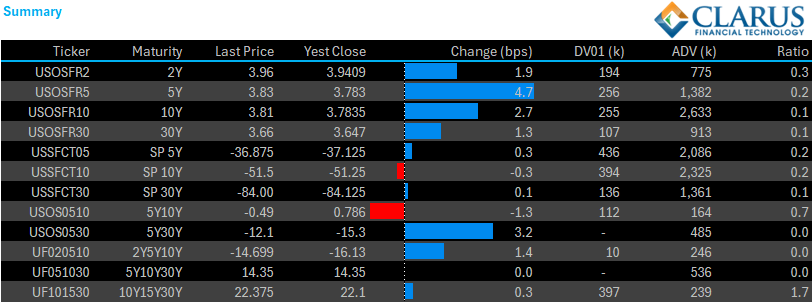

Ticker Summary

For our users looking to monitor volumes, we have our “Ticker Summary” view. For 10Y SOFR swaps;

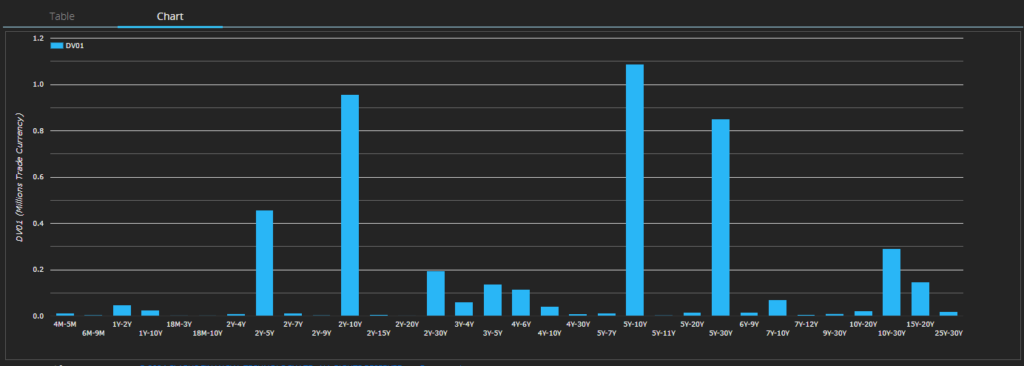

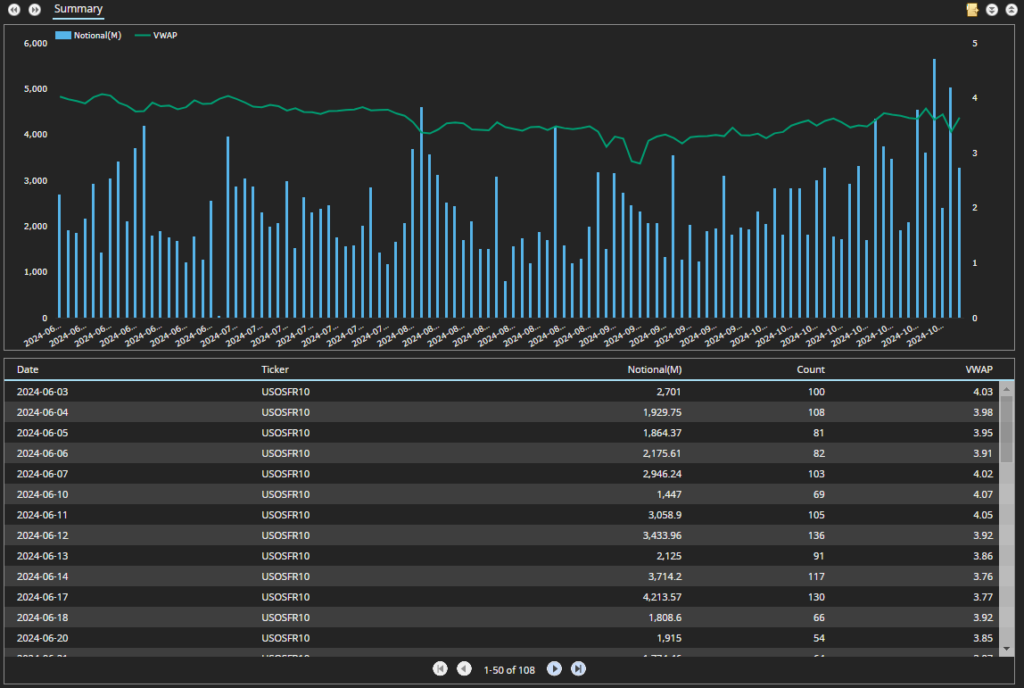

As well as our intraday trade monitors as a “tape”:

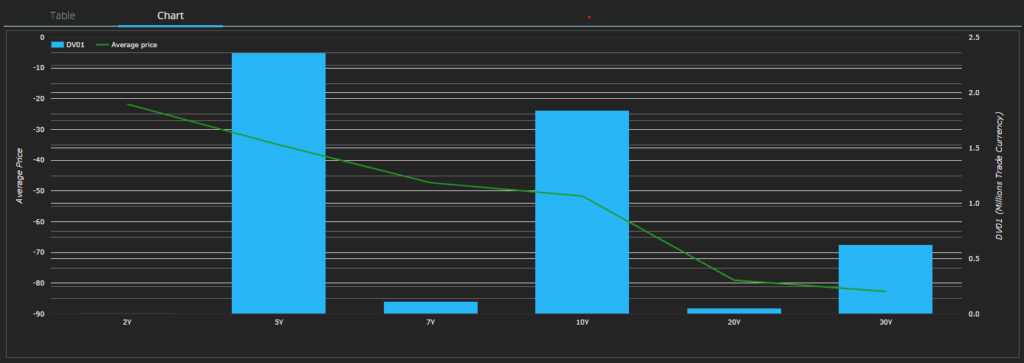

And with our charts as well: