- The CFTC has published a proposal for a new Clearing Mandate

- It covers IRS trading in 9 additional currencies

- We take a look at the detail of the proposal, the data and the timelines involved

The Proposal

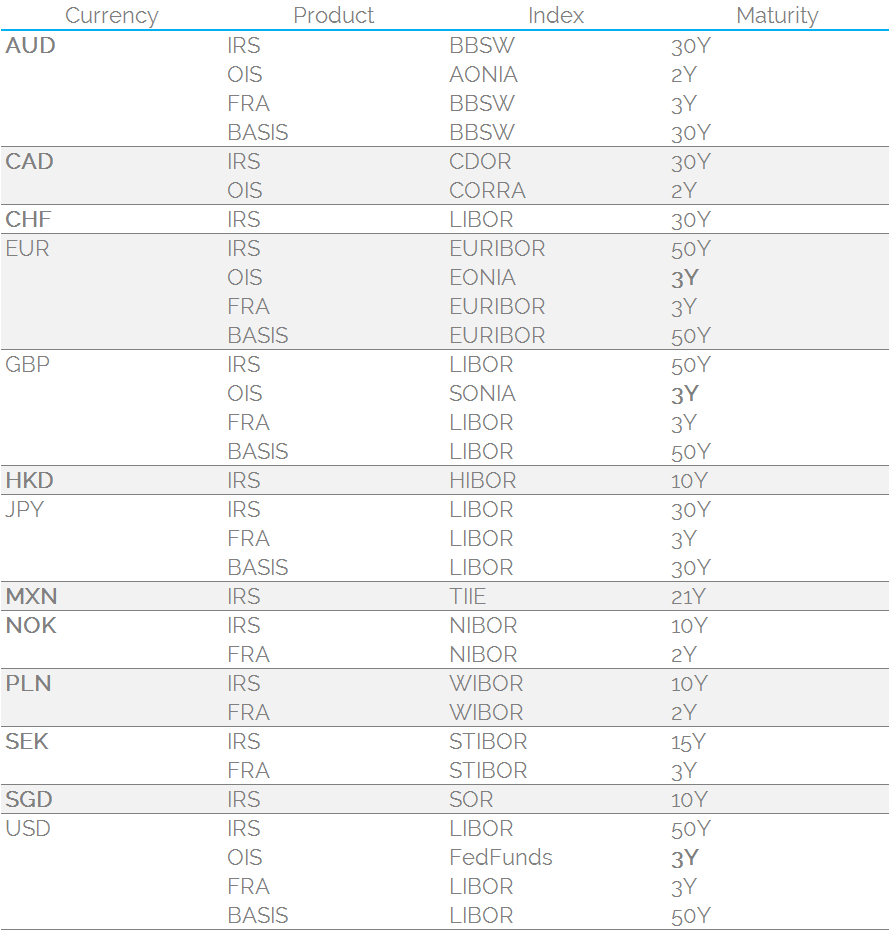

The CFTC has just proposed additional Interest Rate Swaps for clearing. There is a one-hundred-and-eight page rule proposal, which you are free to read here, or just take a look at the table below:

In summary, there are nine additional currencies, plus a maturity extension in OIS clearing for GBP, EUR and USD to 3 year maturities, from the current two.

In his keynote speech to the Global Exchange and Brokerage conference in New York last week, Chairman Massad made it clear that these additional currencies had been chosen “where local jurisdictions have mandated or are expected soon to mandate clearing”.

In the full proposal document, the CFTC also provide a great summary of the current Clearing Mandates in force (or proposed), covering:

- Australia (page 8)

- Canada (page 9)

- European Union (page 10)

- Hong Kong (page 11)

- Mexico (page 11, sadly failing to reference Tod’s blog!)

- Singapore (page 12)

- Switzerland (also page 12)

So those 108 pages now act as quite a nice reference document for anyone researching clearing mandates.

The Data

The CFTC asked the registered DCO’s for data related to this Additional Clearing Mandate. Under Regulation 39.5 (b), the following CCPs submitted data:

- LCH (fixed-floating swaps in 9 additional currencies, plus single currency basis swaps in AUD. Also, OIS out to 30 years for USD, EUR and GBP and FRA data for the additional currencies).

- CME (same as above, plus MXN)

- SGD (SGD swaps only)

- Eurex (CHF swaps, plus OIS in USD, EUR and GBP out to 30 years)

Despite footnote 33 at the bottom of Page 20 promising that these 39.5(b) submissions are available to the public here, it looks like the CCPs have requested Confidential treatment of this data as I can’t find them anywhere. If anyone else can find them, please do get in touch!

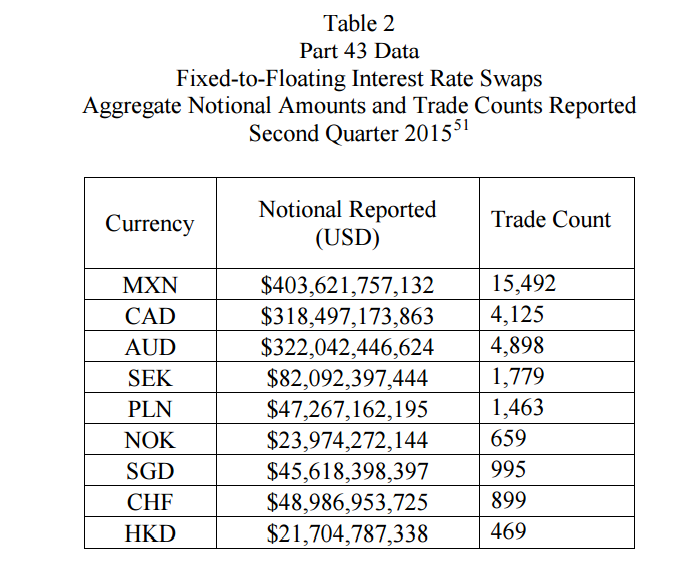

The CFTC also provide useful market analysis for the new products by way of notional amounts, trade counts and percentage of the markets that are already cleared. This is largely derived from the Part 43 data (i.e. the public SDR data) plus some Part 45 data.

Clarus Data

In light of the CFTC using the same Part 43 data that drives the Clarus SDRView products, I thought I would present some simple volume and clearing figures of our own. Regular readers will not be surprised to hear that we have reconciled our figures with the CFTC document (which covers data from April 1st 2015 to June 30th 2015) to within 5 percent (in terms of trade count). The differences are likely due to how we treat cancel/corrects.

The CFTC’s analysis of the Part 43 data yielded the following notional amounts (page 30)

Rather than compare/contrast to SDRView, I thought I would bring these up to date to cover Q2 2016 (so far). We can easily compare to 2015 using the “Compare Y/Y” flag in SDRView Res.

This analysis will prove useful to anyone responding to the CFTC proposal during this comment period.

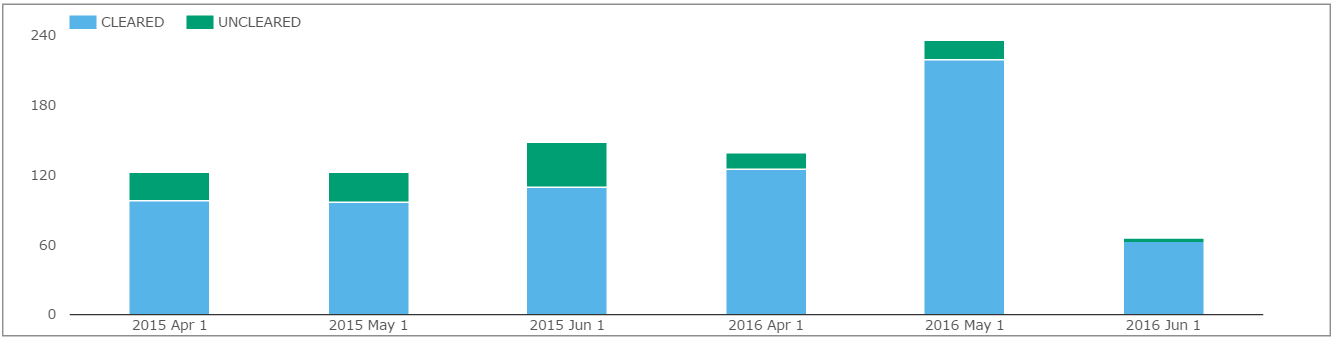

First, let’s concentrate on the “big three” – MXN, AUD and CAD.

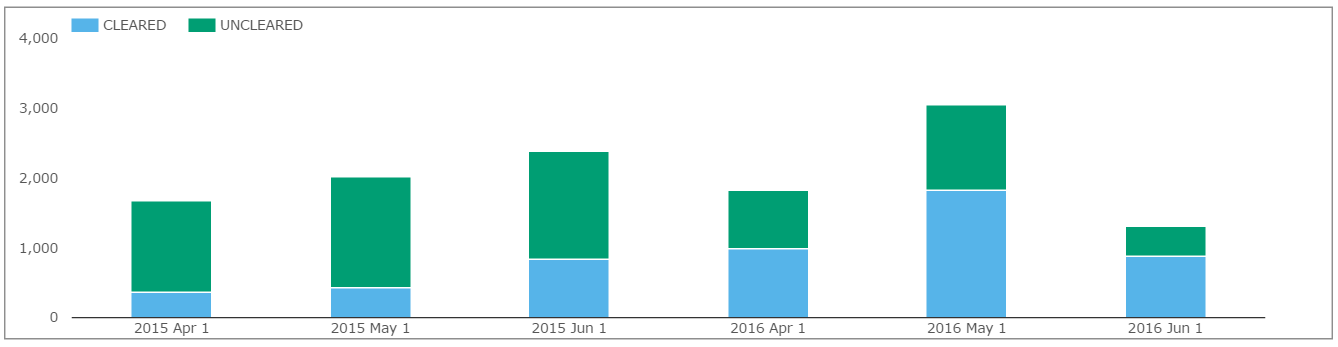

MXN

Cleared Volumes

MXN Fixed-Float swaps are the largest market of the newly proposed currencies, as measured by SDR data.

Showing:

- MXN Fixed-Float swaps traded between April-June 2015 vs the same period in 2016.

- The blue portion shows the amount that is Cleared, the green portion the amounts that were Uncleared.

- Between 2015 and 2016, the uptake of Clearing in MXN swaps has increased significantly (even before this proposed Clearing Mandate!).

- In Q2 2015, only 27% of the market was cleared.

- In Q2 2016, 59.5% of the market has been cleared. Even with half of June 2016 still to go, we have seen 2.25 times the cleared volumes in MXN swaps compared to last year.

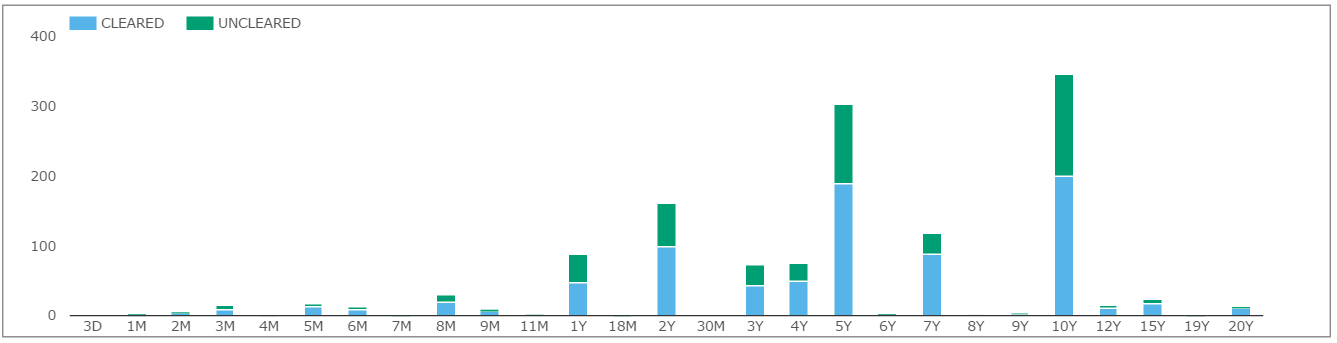

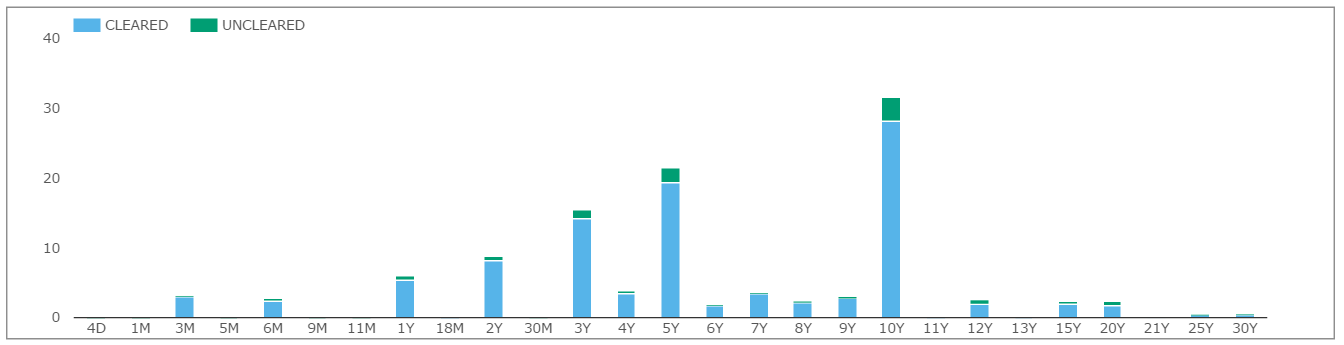

Maturities

The new clearing mandate proposal suggests a maximum maturity of 21 years. What maturities have traded in Q2 2016?

- We choose to show the DV01 profile. This prevents the large notional, short-dated trades that represent only a small amount of risk from skewing the distribution.

- There is most activity in 5Y and 10Y, with our maximum maturity 20 years.

- The split between Cleared vs Uncleared activity is fairly consistent across different tenors.

AUD

Cleared Volumes

Showing:

- AUD Fixed-Float swaps traded between April-June 2015 vs the same period in 2016.

- The blue portion shows the amount that is Cleared, the green portion the amounts that were Uncleared.

- A significant portion of the market was already cleared in 2015. This has only increased this year.

- In Q2 2015, 77% of the market was cleared.

- In Q2 2016, 92% of the market has been cleared.

- Total volume (Cleared and Uncleared) increased (by 12%) between Q2 2015 and 2016.

Maturities

The new clearing mandate proposal suggests a maximum maturity of 30 years. What maturities have traded in Q2 2016?

- Most active maturities (by DV01) are 2Y, 5Y, 10Y.

- There is also activity in 1Y and 3Y, with our maximum maturity 30 years.

- The split between Cleared vs Uncleared activity is fairly consistent across different tenors.

CAD

Cleared Volumes

Showing:

- CAD Fixed-Float swaps traded between April-June 2015 vs the same period in 2016.

- A significant portion of the market was already cleared in 2016. This has (slightly) increased this year.

- In Q2 2015, 86% of the market was cleared.

- In Q2 2016, 91% of the market has been cleared.

- Total volume (Cleared and Uncleared) has increased hugely (by 40%) between Q2 2015 and 2016.

CHF, HKD, NOK, PLN, SEK and SGD

To save running through each currency separately, we can see that the remaining six currencies are surprisingly similar in terms of volumes each month:

Showing;

- On average, SEK swaps accounted for 29% of these volumes, with CHF, SGD and PLN accounting for between 17-18% each.

- HKD and NOK are smaller at around 8-9% each.

- CHF had an outsized volume month in April 2016, accounting for 46% of the volumes. Closer inspection reveals that most of this additional volume in CHF was due to back-starting swaps.

- Excepting this “blip” in CHF volumes, overall volumes in 2016 have been lower than in 2015.

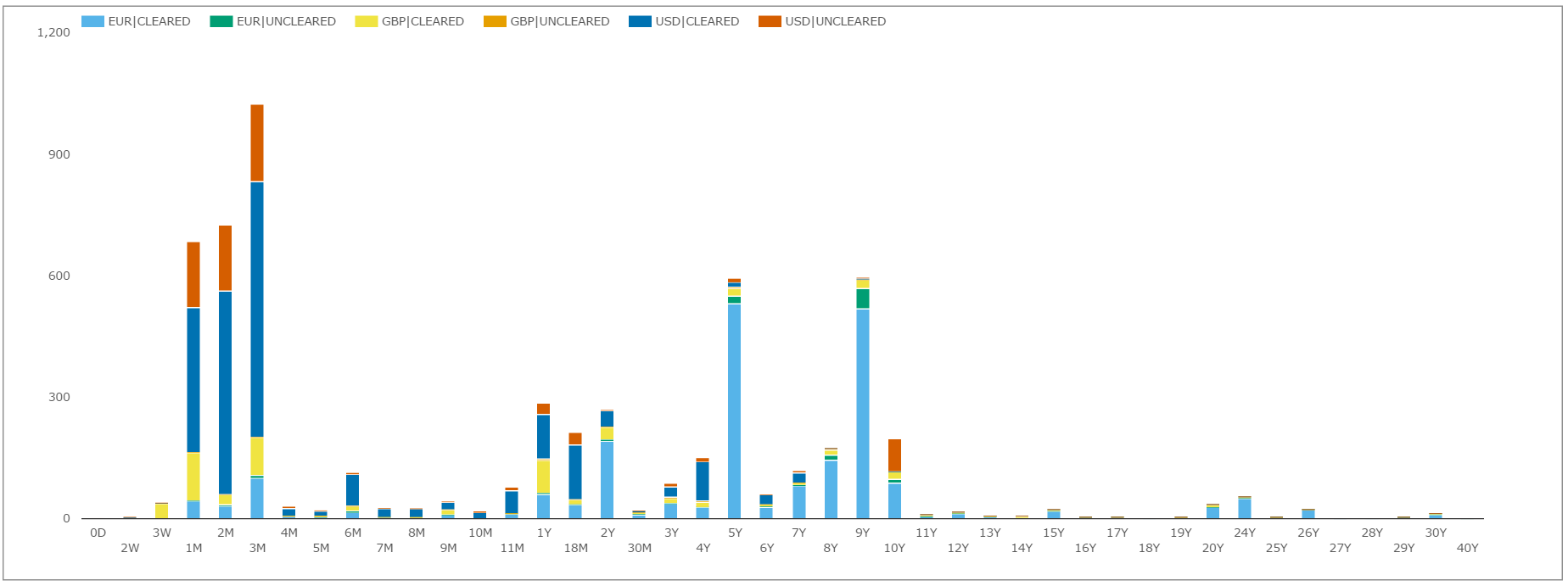

OIS

And finally on the data front, let’s take a quick look at OIS clearing. If we look at the maturity profile by trade count for EUR, GBP and USD so far in Q2 2016:

Showing;

- Number of trades per maturity bucket split by Cleared/Uncleared and currency.

- Cleared activity in EUR OIS is very active in longer maturities such as 5Y, 9Y and 10Y, but USD and GBP are not.

- We can see that the 3 year maturity is not very active, suggesting this maturity extension will have minimal impact.

Implementation Timelines

My reading of the implementation framework is as follows:

- The proposed rule is open now for public comments and this will last until early July (30 days after publication in the Federal Register).

- In Section IV “Proposed Implementation Schedule” there are some interesting points:

- Compliance will not be “phased in”. All market participants will be subject to the new mandate at the same time.

- There are two possible implementation schedules. The simplest is that all swaps under the new clearing mandate become subject to clearing 60 days after publication of the final rule. That would bring us to early/mid September 2016 at the very earliest.

- Alternatively, the CFTC may “co-ordinate implementation with non-US jurisdictions”. This means that a given swap will become subject to the CFTC’s clearing mandate “60 days after the effective date of an analogous clearing requirement”. There would be a ceiling on that of 2 years after the final rule is published.

And then, once the Mandate is in place, we can start the clock ticking on the MAT process….although maybe that is up for review?

In the meantime, feel free to get in touch if you need any data to help when drafting your comments to the CFTC.

Published today, Thursday June 16th, in the Federal Register. Better start that clock ticking…

http://www.cftc.gov/idc/groups/public/@lrfederalregister/documents/file/2016-14035a.pdf

Hi Chris,

Could I please ask what is the difference between the document published on 16 June vs the original proposal on 9th June?

Thanks,

GP

There is no difference as far as I know. There is simply a delay before it is actually published into the Federal Register. Not sure why!

Hi Chris,

So what would the CTFC mandate actually mean for the market? e.g. for $A swaps will it increase the cleared % further (already >90%)?