The Commodity Futures Trading Commission (CFTC) produces a monthly cleared margin report for DCOs (CCPs) required to file daily initial margin with the CFTC’s Division of Clearing and Risk. The report aggregates initial margin from six DCOs: CME, ICE Clear Credit, ICE Clear US, ICE Clear Europe, LCH Ltd and LCH SA.

The latest report is available here for the 7-year period from Dec 2013 to Dec 2021, with monthly data points, available in Excel or as charts in a pdf.

Let’s take a look at the charts and data from the latest December 2021 report.

Initial Margin Requirements

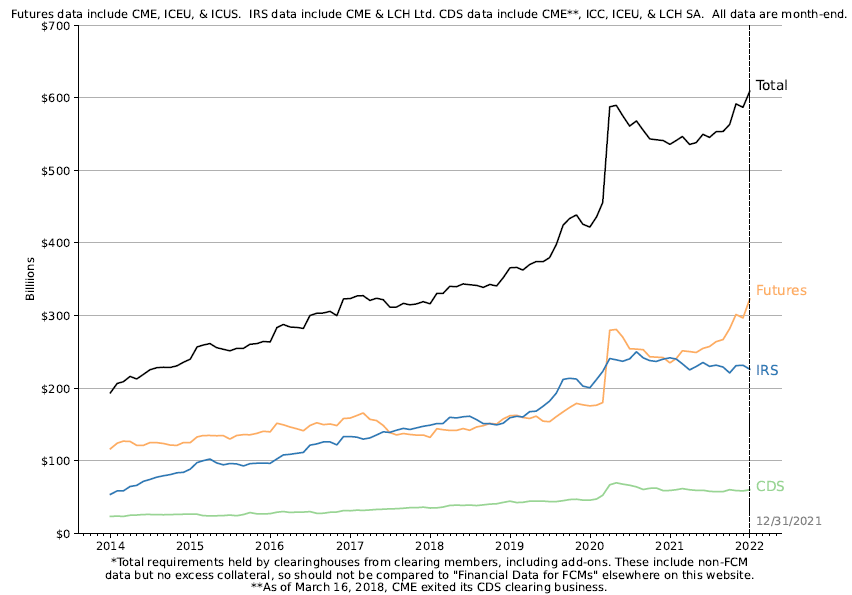

Starting with the first chart from the CFTC report, covering Total, Futures, IRS and CDS IM.

- Total IM increasing from $200 billion on Dec-13 to $600 billion on Dec-21, a 300% increase

- A steady linear trend for the first 6 years and then a sharp jump in Feb-20, particularily in Futures, resulting from a jump in volatility as the Covid-19 pandemic hit, which we covered in procyclical margins in the time of covid-19 and cme s&p500 futures margins.

- A falling off from May-20 to Apr-21, before rising to a new high on Dec-21

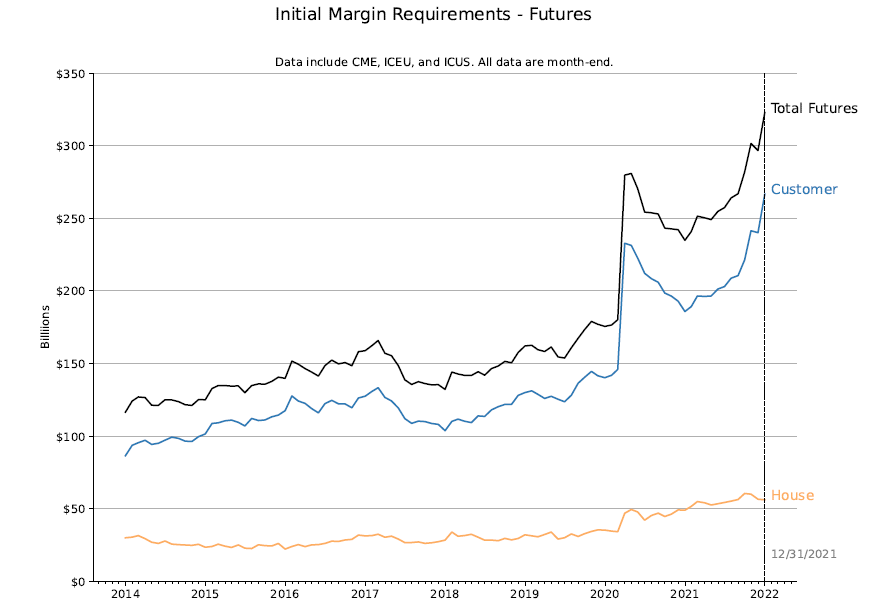

- Total IM for Futures increasing from $116 billion on Dec-13 to $323 billion on Dec-21

- At Dec-19 it was $176 billion, an increase of 51% over the first 6 years, followed by an 83% increase in the next 2 years, most of this later higher increase driven by market volatility resulting in higher margin requirements per contract due to the procyclicaility of margin models

- IM for House, up from $30 billion to $35 billion and then $56 billion, a total increase of 186%

- IM for Customers is larger, up from $86.5 billion to $140 billion and then $267 billion, an increase of 308%

- IM for Customers up from being 2.9X larger to 4.75X larger than House IM

Customer positions, more directional and increasingly larger/riskier than member House positions.

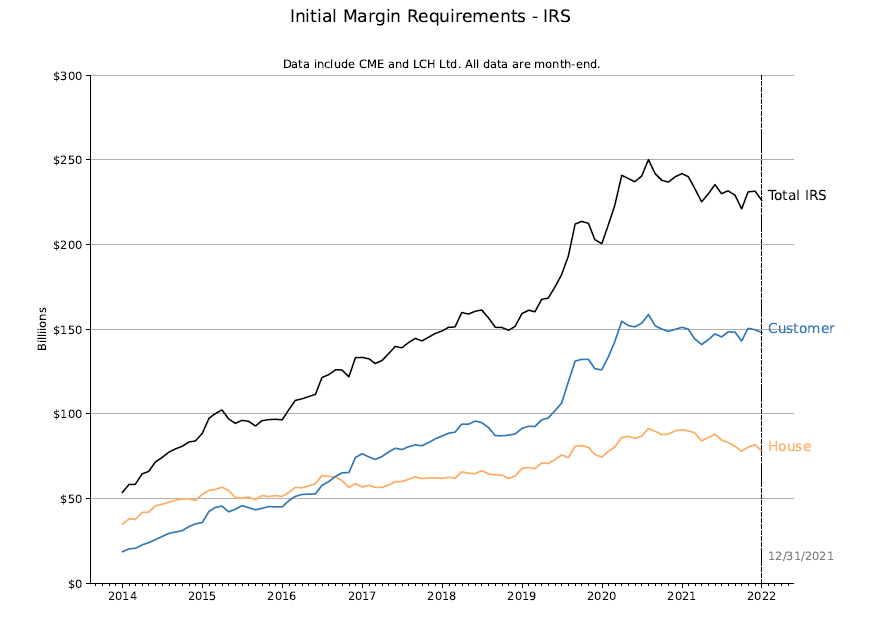

- Total IM for IRS increasing from $54 billion at Dec-13 to $200 billion at Dec-19, an increase of 370%, as more Swaps moved to clearing driven both by regulatory clearing obligations and benefits of voluntary clearing

- A high of $250 billion at Jul-20 and back down to $226 billion at Dec-21

- The lower procyclality of the IRS margin models as compared to Futures, resulting in a much lower increase in IM due to the increased volatility as Covid-19 pandemic hit (see crashing rates and swap margins)

- IM for House up from $35 billion to $78 billion over the full period

- IM for Customers up from $18.7 billion to $148 billion

- IM for Customers up from just 0.5X of House to 1.9X larger than House IM

The interesting question from this chart is have we reached the end of high growth rates in IRS clearing?

All firms subject to clearing obligations are now clearing or will the final phase of UMR in Sep-22 or the possible end of pension firm exemptions in Europe result in new sources of growth?

Only time will tell, but it does seem like the high growth rates of Dec-13 to Dec-19 are at an end and it will be down to higher interest rates leading to possibly more use of Swaps or launching new clearable swap products that may lead to growth. Swaptions, anyone?

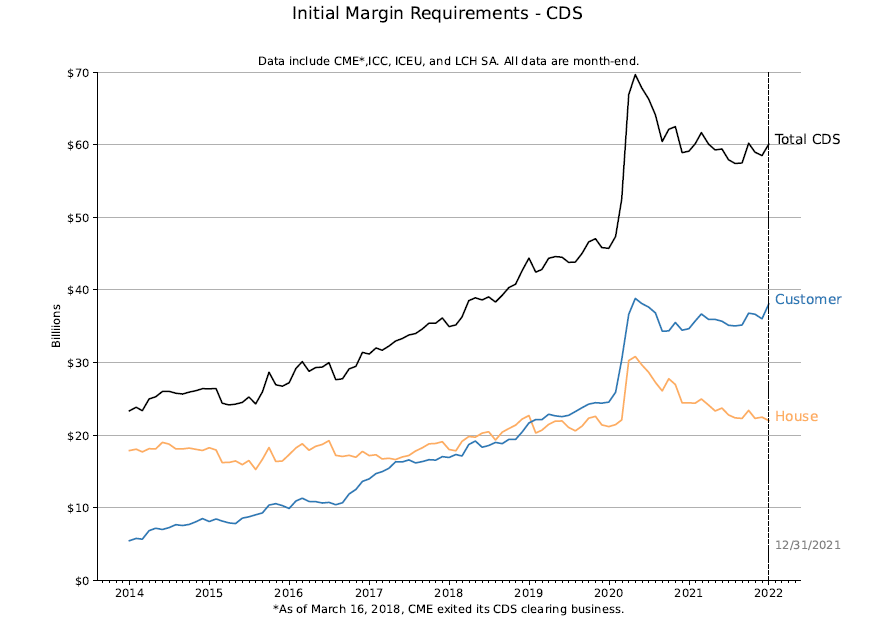

- Total IM for CDS increasing from $23 billion at Dec-13 to $46 billion at Dec-19, an increase of 51%

- A high of $70 billion at Apr-20 and back down to $60 billion at Dec-21

- CDS margin showing similar jumps in Mar-20 as Futures, as the Covid-19 pandemic hit

- IM for House up from $18 billion to $22 billion over the full period

- IM for Customers up from $5.5 billion to $38 billion

- IM for Customers up from just 0.3X of House to 1.7X larger than House IM

There is one more chart in the CFTC report, which I will not re-produce, showing that the concentartion of customer IM requirement at the 5 largest firms is:

- down from 74% to 60% for Swaps and

- flat at 55% to 57% for Futures

- for the Dec-13 to Dec-21 dates

That’s All

That’s all for today.

The CFTC report is well worth a regular look.

And throws up interesting insights and questions.

In CCPView, we have quarterly margin requirements for 43+ clearing houses.

As well as daily volumes and open interest for 20+ CCPs.

To add more color and details, such as relative share of IM, Volumes or Open Interest.

Please contact us if you are interested in a subscription.