This blog covers USD Options markets in Q3 – so please note that is before the election result! This is the latest in a series of blogs covering Swaptions:

- Swaption Volumes by Strike Q1 2024

- SOFR Options – How Healthy Is The Market?

- Swaption Volumes by Strike Q2 2024

- Volumes in EUR Swaptions

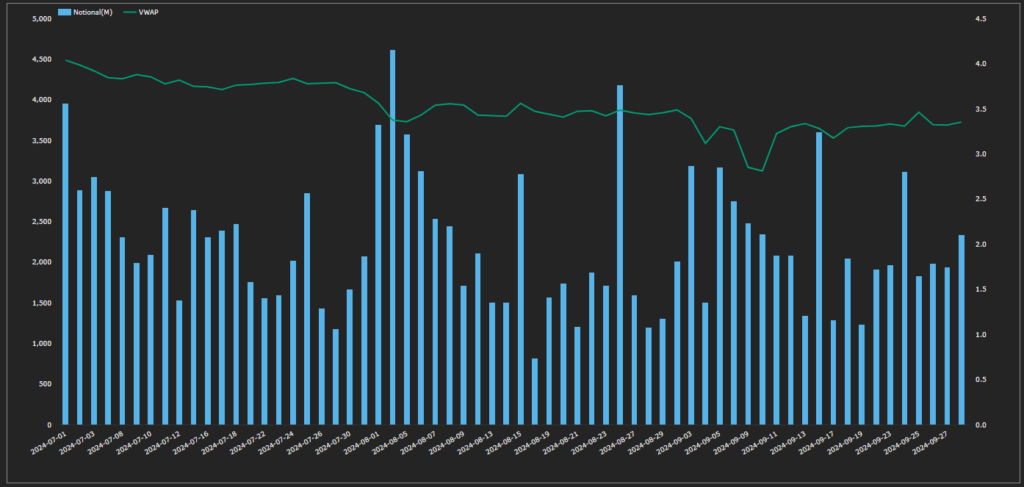

Q3 2024 was a characterised by huge volumes in underlying Swaps, with notable activity in August. There was also a lot of activity tied to changes in expected Fed policy (see the spike in Fed Funds activity here) and of course pre-election positioning. Q3 2024 saw the following daily moves in ten year SOFR swaps:

Showing;

- The daily Volume Weighted Average Price (VWAP) for 10Y USD SOFR Swaps (ticker USOSFR10).

- There was an 86 basis point range in VWAP, from 3.18% to 4.04% for 10Y SOFR swaps. This is a 30 basis point larger range than we saw in Q2!

- It’s quite incredible to look at a chart with falling yields, given what subsequently happened in the run up to the election and a 60-70bp move higher in Rates from the end of Sep.

- This is a Q3 blog though, so I must honour the data.

- The largest volume days were back in August – consistent with our blogs at the time – which saw yields fall significantly.

- Volumes then peaked again at the end of August and in the middle of September (from the lows in yield).

Notes on the Data

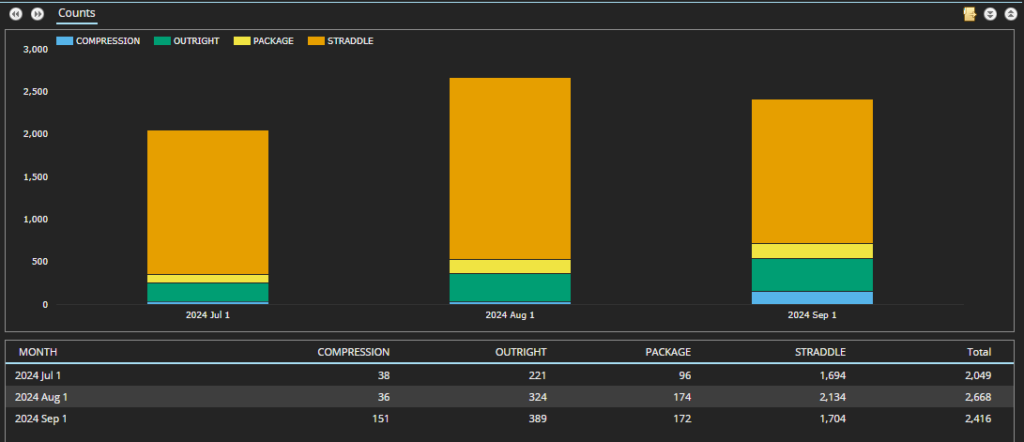

Straddles are one of the packages that Clarus identify in SDR data. They are no longer identified in the source data – see this blog for details about how the data changed. Over 80% of D2D trades are Straddles, as shown by the Q3 SDR data:

Swaptions Activity

The Year-on-Year comparison highlights the variability we see in Swaption volumes:

Trade count of all Swaptions. Source: SDRView

Showing;

- 23,500+ swaptions executed in Q3-2024, 9% lower than Q3-2023.

- July saw 25% fewer swaptions executed than the previous year.

- August saw 18% less swaptions (despite those volatile days and record volumes in swaps)…

- …but September saw 28% more swaptions executed than last year.

Swaptions Activity by Strike

SDR data for all USD Swaptions reported in Q3 2024 (including packages) can be used to create the following heatmap of Swaption activity:

The summary of Q3 2024 USD swaptions activity shows;

- The notional volume (in $ millions) of USD swaptions traded in major tenors in 25 basis point strike increments.

- This covers all expiries. A 3m10y is grouped together with a 1y10y if they were traded at the same strike.

- This covers Payers & Receivers, Straddles and all other Packages.

- It looks at new volumes traded in the quarter. This is not the same as Open Interest (such as the CME Heat Maps) but it nevertheless gives an idea of activity.

- Red areas show the “hottest” strikes and tenors, those with the most notional volume traded.

- We saw strikes all the way up to 6.75% trade in the quarter (for 1Y underlyings), with activity starting to drop-off at ~5.75% strikes for most of the underlyings.

- The highest strike with more than $1bn traded in a particular tenor saw $1.93bn of activity at a 6.25% strike versus 1Y (the underlyings are also referred to as “tails” FYI).

- The red areas largely reflect where the at-the-money rates were as vol trading is naturally concentrated around these areas. The red areas can help highlight the shape of the curve.

- The most active tenor was 1Y, with a huge $668bn traded across all strikes in Q3 2024, $130bn more than during Q2.

- There is then a big gap to activity in 10Y underlyings, with $352bn traded (similar to Q2). This is consistent with our previous analyses where 1Y and 10Y tenors see the largest notional amounts trading.

- There was an exceptional amount of activity in 1Y tails at a strike of 4.25% with over $111bn trading.

Receivers Activity

Now looking at activity only in Receivers:

- Total activity in Receivers accounted for 37% of overall Swaption activity (measured by notional) – identical to the 37% we saw in Q2 2024.

- The most active underlying was 1Y, which saw a range of strikes traded. $10bn or more traded in strikes from 3.0% all the way up to 4.75% (compared to 3.75-5.25% for the previous quarter).

- Activity in 20Y underlyings is always seemingly heavier in Receivers. Of all activity versus a 20Y tail, 50% was in Receivers (versus 25% in Payers). Activity was concentrated at the 3.5% and 4% strikes.

Payers

And for Payers only;

- Payers accounted for 39% of total Swaptions activity as measured by notional (up from 36%).

- The most active underlying and strike was 1Y 4.25%, with over $50bn traded – the most active of any 25 basis point increment across Payers and Receivers.

- The most active strike for 1Y tails was 100bp higher in Q2 at 5.25%.

- 4Y underlyings (a bit niche!) were relatively more active in Payers this quarter, with 51% of all activity in Payers. The most active strikes were 3.25-3.5% but they still only saw $2.9bn traded. 30Y tails were also pretty active in Payers, accounting for 46% of activity.

Straddles

And finally, the Straddles Heatmap:

- The range of strikes seen in Q3 was wider than Q2 in Straddles. As a reminder, a Straddle is a combination of a Receiver Swaption and Payer Swaption with the same expiry, same underlying and same strike. Therefore, if Rates do not really move, both Payer and Receiver positions will expire worthless, and the premium paid (or received) will constitute a loss (or gain).

- Straddles accounted for 25% of total swaption notional traded, down from 28% in Q2. Activity in Straddles is heavily skewed toward the D2D market.

- The most traded Straddles were 10Y underlyings at 3.5% and 1Y from 3-3.75% .

- 10Y 3.5% straddles were the most active of any instrument that we saw traded, accounting for over $43bn of activity each (these are “package adjusted” notionals, so only one leg of the Straddle notional is counted).

- Unusually, there was (just) more activity in Straddles versus 20Y tails, than there was in outright 20Y Payers.

In Summary

- Analysis of swaptions activity is a regular feature on the blog across Payers, Receivers and Straddles, allowing us to monitor quarterly trends.

- Heatmaps of option activity show the most active underlyings (tails) and strikes.

- Q3 2024 saw 9% fewer swaptions transacted than the same quarter last year.

- There was a huge amount of activity in Payers versus 1Y underlyings at 4.25% strikes.

- 10Y 3.5% Straddles saw over $43bn in activity, the most active of any single instrument.