On June 8, the CFTC’s Market Risk Advisory Committee’s (MRAC) Interest Rate Benchmark Reform Subcommittee voted to recommend market best practice for switching interdealer trading conventions from Libor to SOFR (see release 8394-21).

Referred to as SOFR First, it is modelled on the UK’s SONIA First and is a prioritization of interdealer trading in SOFR over LIBOR. It recommends that on July 26, 2021 and thereafter, interdealer brokers replace trading of LIBOR linear swaps with SOFR linear swaps and keeping IDB screens for Libor Swaps available for informational purposes, but not trading until October 22, 2021, after which date these screens should be turned off altogether.

Wow! Another gun has been fired in the transition from LIBOR to SOFR.

On the same day the Alternative Reference Rates Committee (ARRC) put out a supporting statement.

I can only imagine the work and upheaval to come between now and July 26…

For today, I will take a quick look at Spreadovers.

Spreadovers

In USD Swaps a large chunk of inter-dealer trading is not in outright Libor vs Fixed Swaps but in Spreadovers (to US Treasuries). So it was interesting to see a market response on the 9th of June, with the first SOFR Spreadovers trading.

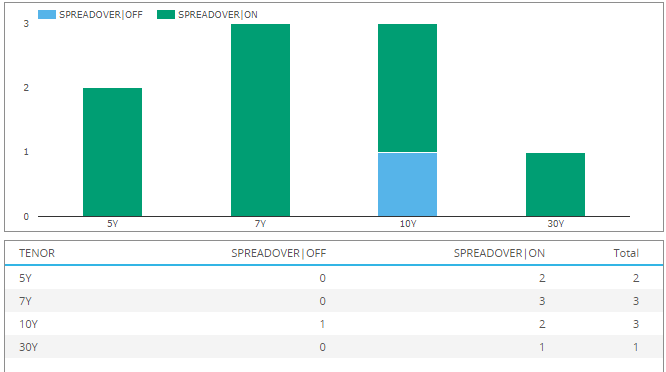

In SDRView, we can now identify these trades and on 9th June we see:

- 1 trade OFF SEF and 8 trades ON SEF

- 2 in 5Y, 3 in 7Y, 3 in 10Y and 1 in 30Y

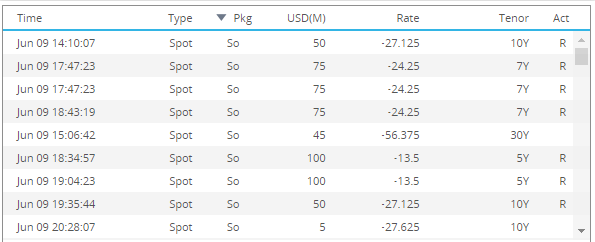

And while SDRs publish the outright fixed rate, in SDRView we can imply the actual rate:

- Time shown above is London (where I am based) and not New York

- 5Y traded twice in $100m at -13.5bps

- 7Y traded three times in $75m at -24.25bps

- 10Y traded twice in $50m at -27.125 bps

- 10Y also traded Off SEF in $5m at -27.625bps

- 30Y traded once in $45m at -56.375bps

So interesting to say the least!

Unfortunately subsequent days were a let down.

- Nothing on June 10

- 3 Off SEF trades on June 11

- Nothing on June 14

- 1 On SEF trade on June 15

- A couple this morning on June 16, as I write this…

There is the possibility that we could have failed to identify all SOFR spreadover trades, as we are still learning how to spot them from the hundreds of OIS trades reported each day. So stay tuned on that front, but at least our task is much simpler than that faced by market participants in achieving SOFR first.

That’s It for Today

There is a lot of work to do by July 26, 2021, which is less than six weeks from today.

Broker screens such as TP-ICAP’s 19901 are long established as the reference page for USD Spreadover prices and are crucial in Fixed Income markets.

Then there are quoting conventions, market making, trade booking, risk management, clearing, settlement and accounting, to check and work out any impacts.

We plan to follow SOFR First closely.

And will publish more in the lead up to July 26th.

Any comments or views, please send our way.