For some time now I have been noting, but not reading, articles about the Securities Financing Transactions Regulation (SFTR) being implemented in Europe, so today I wanted to take my first look into this regulation.

Background

The ESMA website has a good section on SFTR Reporting, so I will copy & paste liberally from that, judiciously of course, to provide an overview and then deep dive into what interests us most at Clarus; public transparency data.

Securities financing transactions include:

- a repurchase transaction;

- securities or commodities lending and securities or commodities borrowing;

- a buy-sell back transaction or sell-buy back transaction;

- a margin lending transaction.

Implementing SFTR provisions

SFTR builds on the elements of EMIR and establishes an obligation on market participants to report transactions to Trade Repositories (TRs) and establishes access to the data.

The bulk of the SFTR documentation material is rightly concerned with detailed rules and guidelines on the specifics of reporting .

A quick check on the implementing technical standards makes clear that trades/transactions between counterparties need to be reported, with fields including,

- unique transaction identifier (UTI),

- execution timestamp,

- trading venue and CCP,

- counterparty LEIs

- economic details (price, size, dates)

- security types, collateral data

- ….

So that is a great start, no lack of data there that has to be reported to TRs.

And transactions need to be reported on a T+1 basis, which is consistent with EMIR.

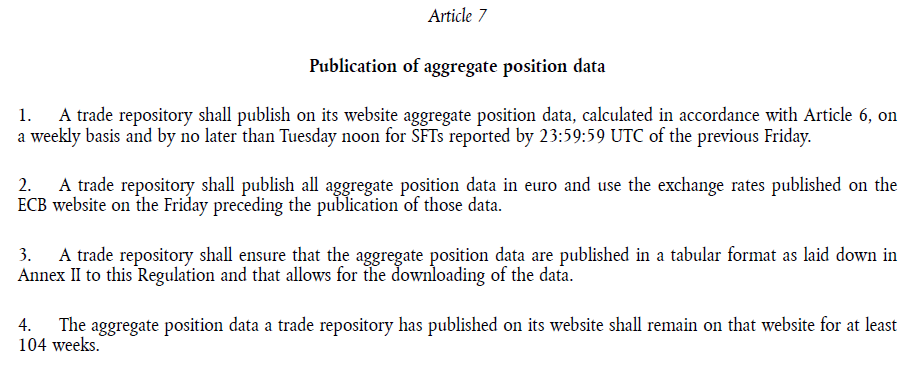

Access to Data

Let’s now turn to the section for Accessing Data on the ESMA SFTR page, which links to an RTS document and the following extract.

So aggregate position data published tuesday midnight for the the prior week, in a tabular format that allows for downloading and kept on the TRs website for 2 years.

Quite a few positives here, but the aggregate and weekly is a concern. It would be a real shame if this data ended up with as little real world value as the Derivatives data reported by TRs under EMIR.

However I am willing to hold my hand up and say I am not an expert in repos and sec lending to know if the sheer volume of transactions means trade level disclosure is impractical and would be harmful for liquidity.

Let’s press on with the details.

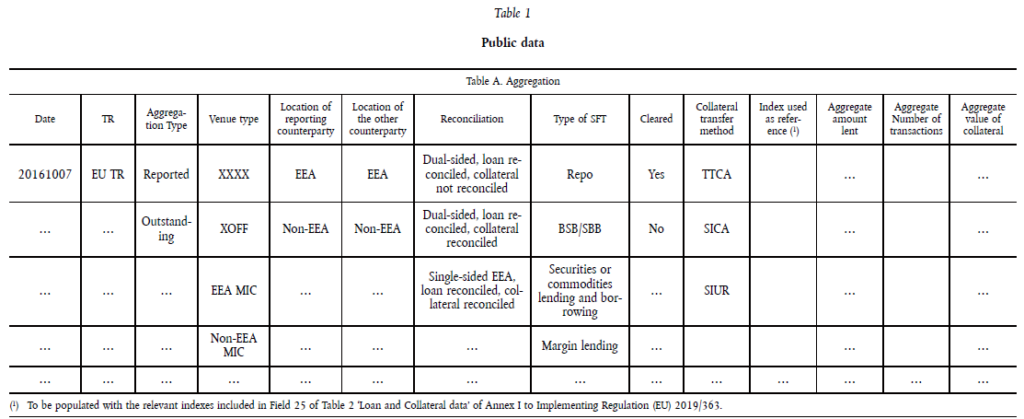

Article 6 – Position data for publication

Article 6 is titled, “Calculation of aggregate position data for publication” and provides for a weekly aggregate position report for new trades as well as an outstanding positions report.

The format for these are given in Annex II, as shown below.

So each TR will publish these reports, both weekly and outstanding position data, however the aggregation seems to be very high level and lacking granularity.

We have the amount (principal), number of transactions, value of collateral aggregated by:

- venue type,

- EEA/non-EEA location of counterparties,

- reconciliation status

- type of SFT (Repo, Sec lending, Margin lending…)

- cleared or not

- collateral transfer method

- index as reference ( EONIA, EURBOR, LIBOR, TREA, …..)

Hmm, at first glance that looks disappointing.

No breakdown by trading venue nor ccp, no currency breakdown, no identification of the country of issue of the bonds used in repos, no information on term (o/n, 1w, 1m,…), …… I could go on.

Article 5, which provides for position data that TRs need to make available to ESMA and other official sector bodies, does have some of the above detail (e.g. term) but also looks highly aggregated. Possibly to cope with the sheer volume of transaction data.

It would be a real shame if after 5 years and multi-millions of investment by market participants, we end up with no useful improvement in public transparency for SFTs.

Availability of Public Data

When can we expect to see the data?

ESMA put out a public statement on 26 March 2020, which delayed the reporting obligation for credit institutions, investment firms and relevant third-country entities from 13 April 2020 to 13 July 2020, due to the Covid-19 pandemic disruptions.

While reporting for CCPs and CSDs remains on the original phase date of 13 July 2020 and for insurance companies, pension funds on 12 October 2020.

So we will have to wait two and half months, to July 13 or rather July 24 to see the first reports for the week of July 15-19.

Final Thoughts

I have added the date in my calendar to check TR websites to see what data is published.

Let’s hope these provides new and interesting insights into Repo and Sec Lending markets.

Markets which are large and important for liquidity, maturity transformation, leverage and in terms of interconnectedness between participants.