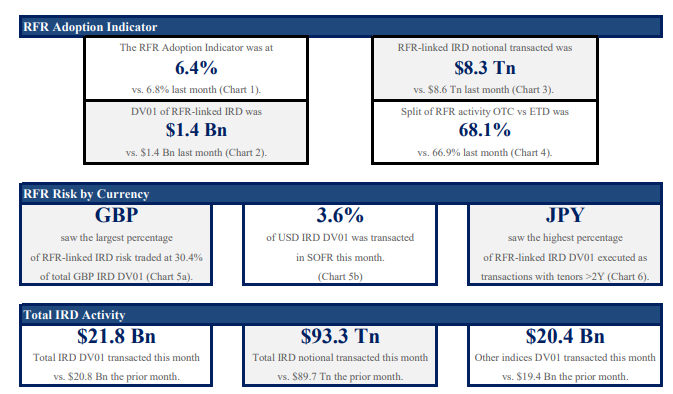

The ISDA-Clarus RFR Adoption Indicator has been published for August 2020. The headlines are:

- The RFR Adoption Indicator was at 6.4% in August 2020.

- This was pretty unchanged from 6.8% the prior month, and short of the highs hit in January 2020.

- 3.6% of all USD risk was traded in SOFR vs 3.8% last month, so no great change there.

- The discounting switch to €STR at CCPs occurred in the final days of July, so we were expecting this to have an impact on the amount of €STR risk traded during August.

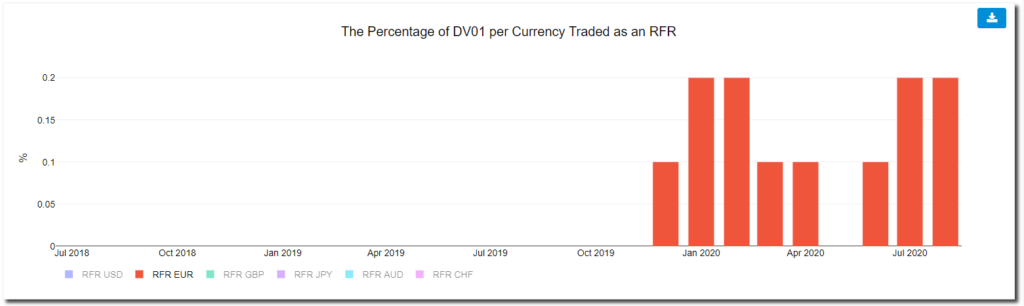

- However, €STR accounted for just 0.2% of total EUR risk traded, unchanged from the prior month.

- Indeed, even looking at the LCH €STR volumes in August, they were actually lower than in July (in notional terms).

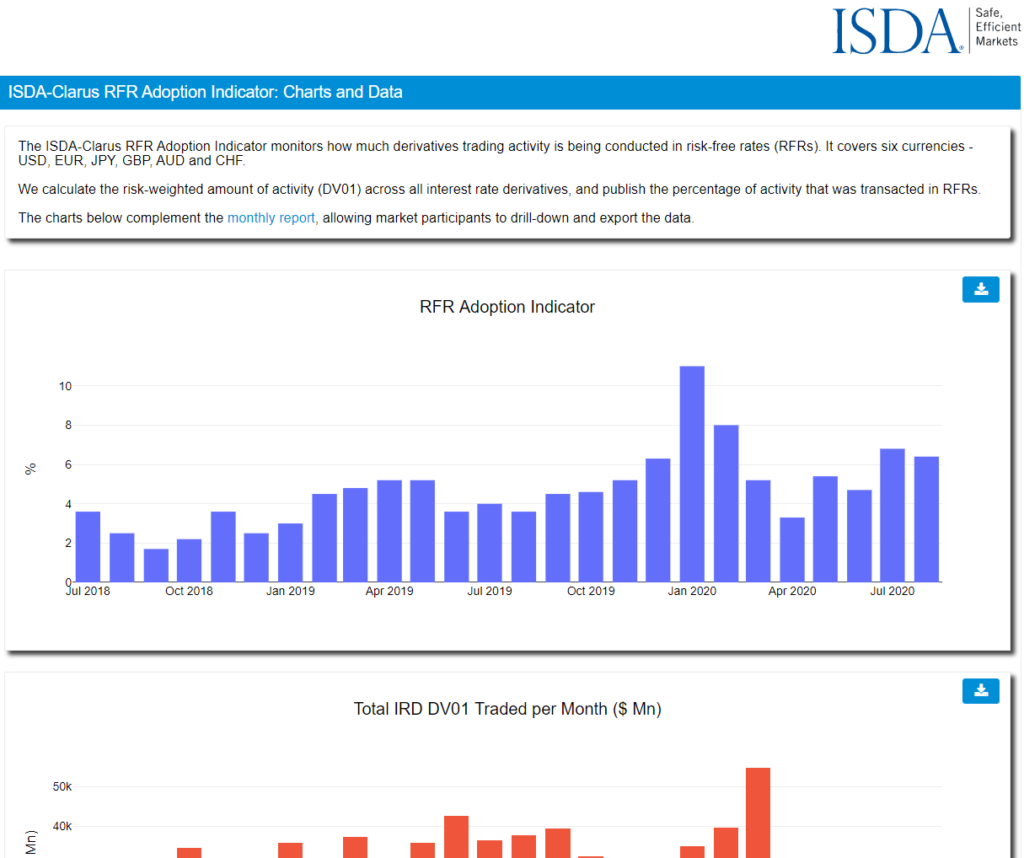

Please see rfr.clarusft.com for interactive charts (and data downloads) covering all of the measures in the ISDA-Clarus RFR Adoption Indicator:

€STR waiting to Take-off

The discounting switch in July seems to have done little for the appetite of €STR risk. Even from SDR data alone, we see that EONIA risk continues to dominate trading:

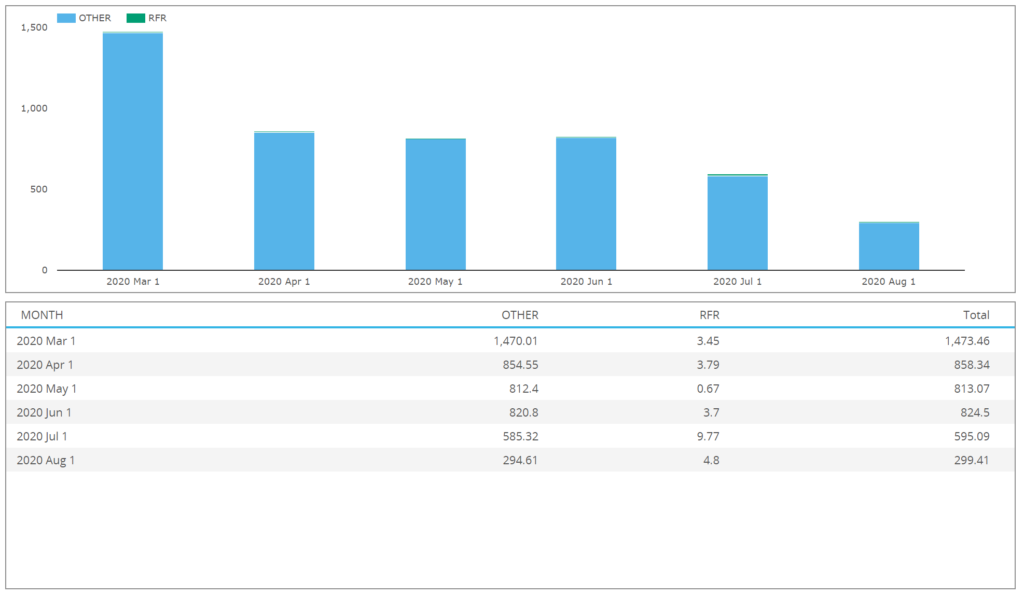

And CCPView shows that total notional amounts across both LCH and Eurex were lower for €STR products during August than July:

Whilst it might be easy to write this off as a result of “quiet” summer markets, the transition to RFRs should really be working on a different schedule to typical market behaviour.

Unfortunately, even as a proportion of the overall risk traded, there was no substantial increase in €STR activity:

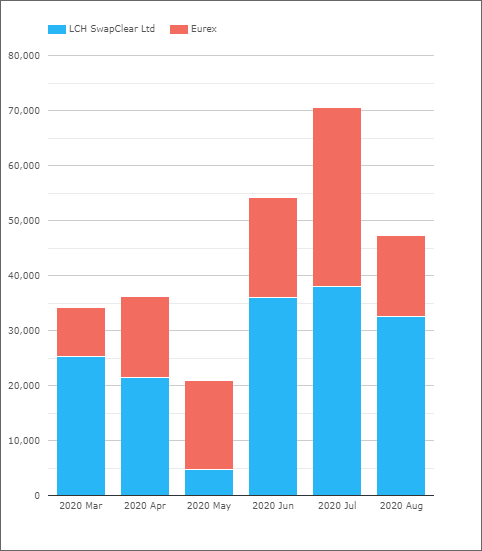

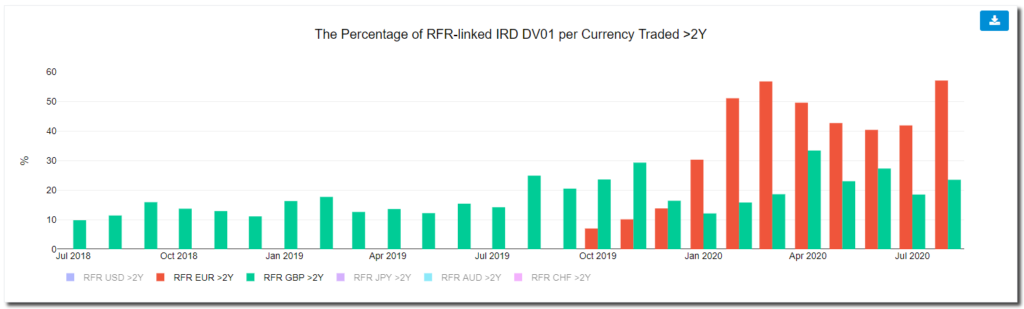

One area where things look relatively rosy for €STR is the amount of long-dated risk traded. Okay, they are small amounts, but at least 50%+ of €STR risk tends to be longer than 2 year maturities. This is considerably more than e.g. GBP SONIA:

What About SOFR?

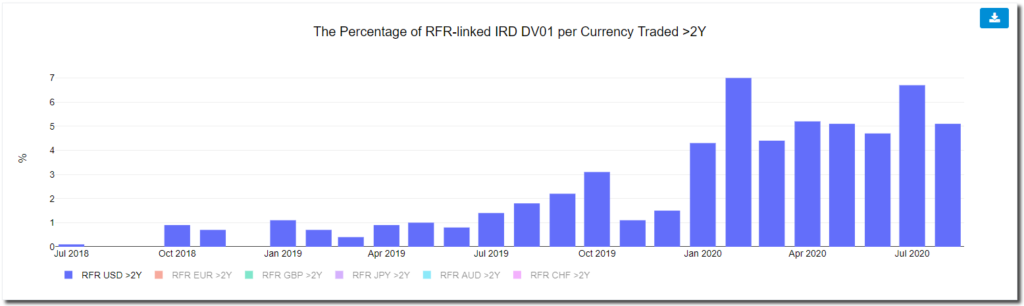

Most SOFR risk continues to be traded in futures, rather than OTC. This means that across the whole market, 95% of risk tends to be less than one year maturities:

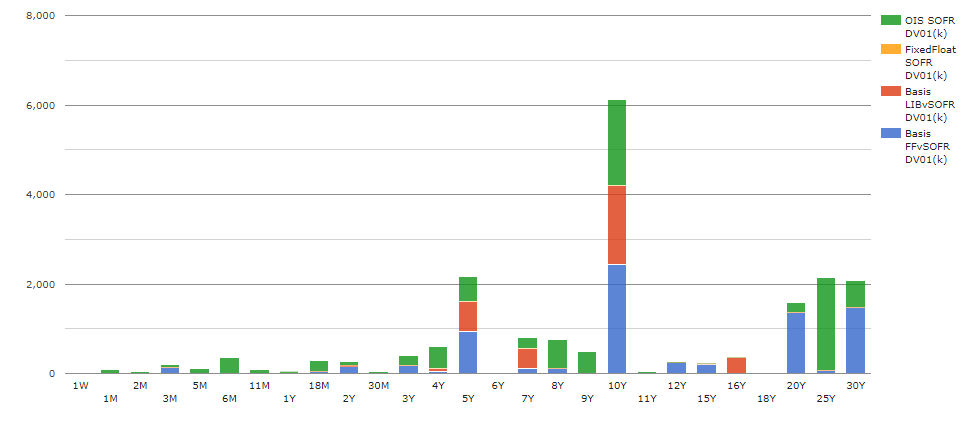

However, that doesn’t chime with the picture from OTC markets alone, where August certainly saw some interesting activity (SDR data only);

From the chart, we can see that on a DV01-basis, there was more activity in 10Y SOFR than any other area of the curve. This activity was comprised of outright OIS as well as basis trades versus both Fed Funds (EFFR) and USD LIBOR.