FRTB for Excel

Access the power of cloud-hosted FRTB analytics directly from spreadsheets

For financial firms implementing FRTB, we offer a free trial

CLARUS Excel Workbooks or Add-in

FRTB Standardised Approach

FRTB Non-Modellable Risk Factor analysis

Easy to Trial, Purchase and Start Using

Learn about FRTB NMRF

Learn about FRTB SA and IMA

Latest Posts

-

Feb, 26

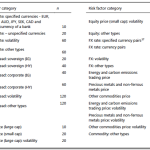

FRTB Risk Factor Eligibility Test (RFET)

In January 2019, the Basle Committee on Banking Supervision (BCBS) revised the 2016 market risk framework, generally known as the Fundamental Review of the Trading Book (FRTB) to address design and calibration issues and to provide further clarification. One of the topics of interest is an improved criteria for the identification of modellable risk factors […]

Read moreJul, 5

FRTB – Basic Approach for CVA

Introduction A core component of managing bilateral exposures is CVA – Credit Valuation Adjustment. The grandfather of all XVAs, it describes the change in exposure we have to a counterparty as a result of changes in both the mark-to-market of a derivative and the change in credit-worthiness of our counterparty. Today, we’ll look at the […]

Read more -

Jun, 19

FRTB in Excel

FRTB Calculations directly from Excel. What-If analysis of new trades via quick trade entry. We use the CRIF format to make entry of trade portfolios simple. FREE 14-day trials available here. Background FRTB in Excel from Clarus calculates the capital requirements for your portfolio in Excel. We also check whether risk factors are modellable. The […]

Read moreMar, 28

FRTB – Revisions to market risk capital requirements

The BCBS published a Consultative document in March 2018 with the title ‘Revisions to the minimum capital requirements for market risk” and in this article I look at the details. Background In January 2016, the BCBS published the standard Minimum capital requirements for market risk ( “January 2016 standard”), designed to address a number of structural shortcomings in […]

Read more -

Aug, 30

FRTB Non-Modellable Risk Factor Analysis

The FRTB Internal Model Approach requires risk factors to be checked for modellability Non-modellable risk factors are then subject to stressed capital add-ons Modellable and non-modellable is determined by applying a specific test Clarus has the Data and Analytics to perform such a test We make this available in our FRTB for Excel product Making […]

Read moreAug, 8

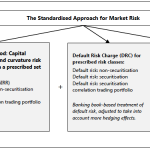

FRTB – Simplified Standardised Approach

The BCBS recently published a Consultative document on a ‘Simplified alternative to the standardised approach to market risk capital requirements” and in this article I will look at the detail of this. Standardised Approach (SA) BIS provides the following diagram to summarise the Standardised Approach. (For a re-cap of the SA see FRTB – What […]

Read more -

Mar, 28

Microservices: FRTB Modellable Risk Factors

FRTB regulations specify that non-modellable risk factors are subject to stressed capital add-ons For a risk factor to be modellable it must pass a specific test for continuously available real prices The Clarus API provides functions for the risk factor modellability test for OTC Derivatives These functions are very easy to call from many popular languages, […]

Read moreFeb, 14

FRTB Curvature Risk Charge

Various risk charges must be calculated under the Standardised Approach of the FRTB. These risk charges are split into Delta, Vega and Curvature. Curvature Risk Charge is complicated to calculate as we must record MTM changes to large input shocks. We explain the calculations involved. For Rates products, the Curvature Risk Charge is not split by tenor […]

Read more -

Feb, 7

FRTB Vega Risk Charge

Various risk charges must be calculated under the Standardised Approach of the FRTB. These risk charges are split into Delta, Vega and Curvature. Vega Risk Charge is complicated to calculate as we must build several co-variance matrices. We provide a step-by-step explanation of all of the calculations involved. We use Excel throughout to calculate and illustrate the […]

Read moreDec, 13

FRTB – Modellable Risk Factors and Non-Modellable

Following on from my article FRTB – Internal Models or Standardised Approach, I wanted to look at specific component of the Internal Model Approach (IMA), namely the fact that all risk factors are subject to a Modellable or Non-modellable requirement and non-modellable risk factors result in a higher capital charge. Background In January 2016, the Basel Committee on […]

Read more