The last couple weeks we’ve written about if and how the Uncleared Margin Rules have changed behavior of dealers to clear trades that are not clearing-mandated. The logic being that under the new Rules, it is more cost efficient to clear some trades than to have the trades exist bilaterally.

Last week we saw:

- Clear Evidence that Inflation swaps are now more actively cleared

- A glimmer of evidence that a similar behavior was emerging for FX NDF’s

Fast Forward A Week

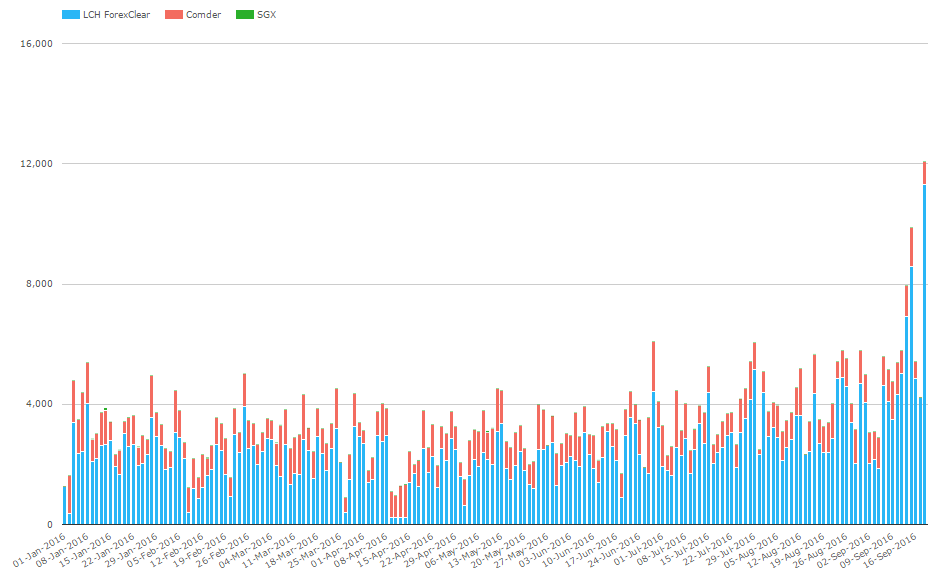

Updating the analysis now through September 20th, 2016, and it looks like NDF data is also beginning to turn. Lets start with clearing volume from CCPView:

This paints a pretty clear picture of global cleared NDF data:

- Average daily cleared volume was generally up to and around $4 bn

- Daily cleared volume in September nearly double that

- Tuesday September 20th was by far the most active day, touching $12 bn globally

- LCH accounts for seemingly all of the growth

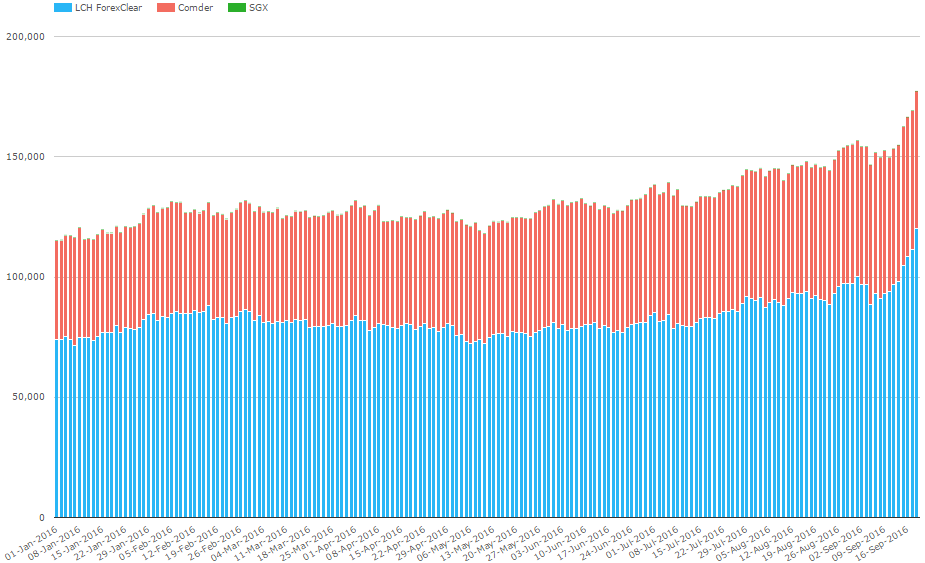

Next, Open Interest corroborates this:

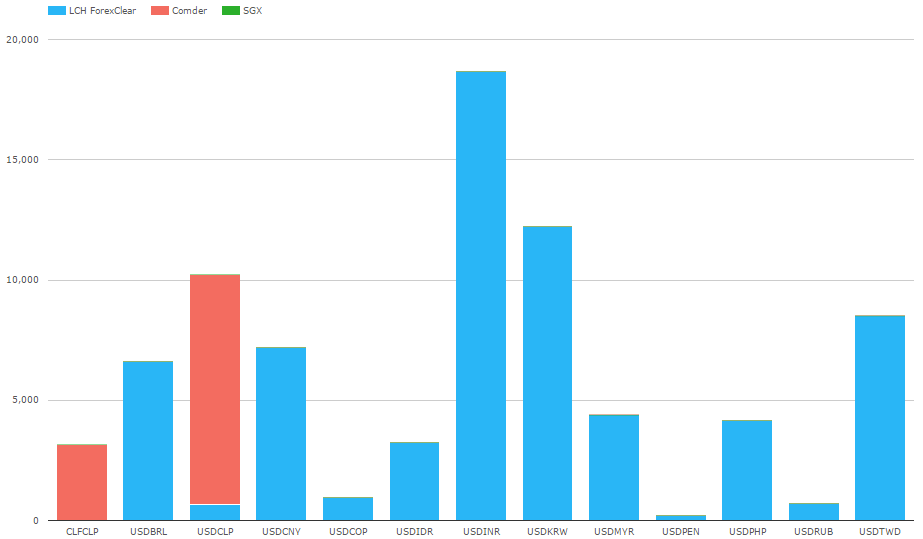

And how about by Ccy Pair, this time for the current month of September:

Where Is It Coming From?

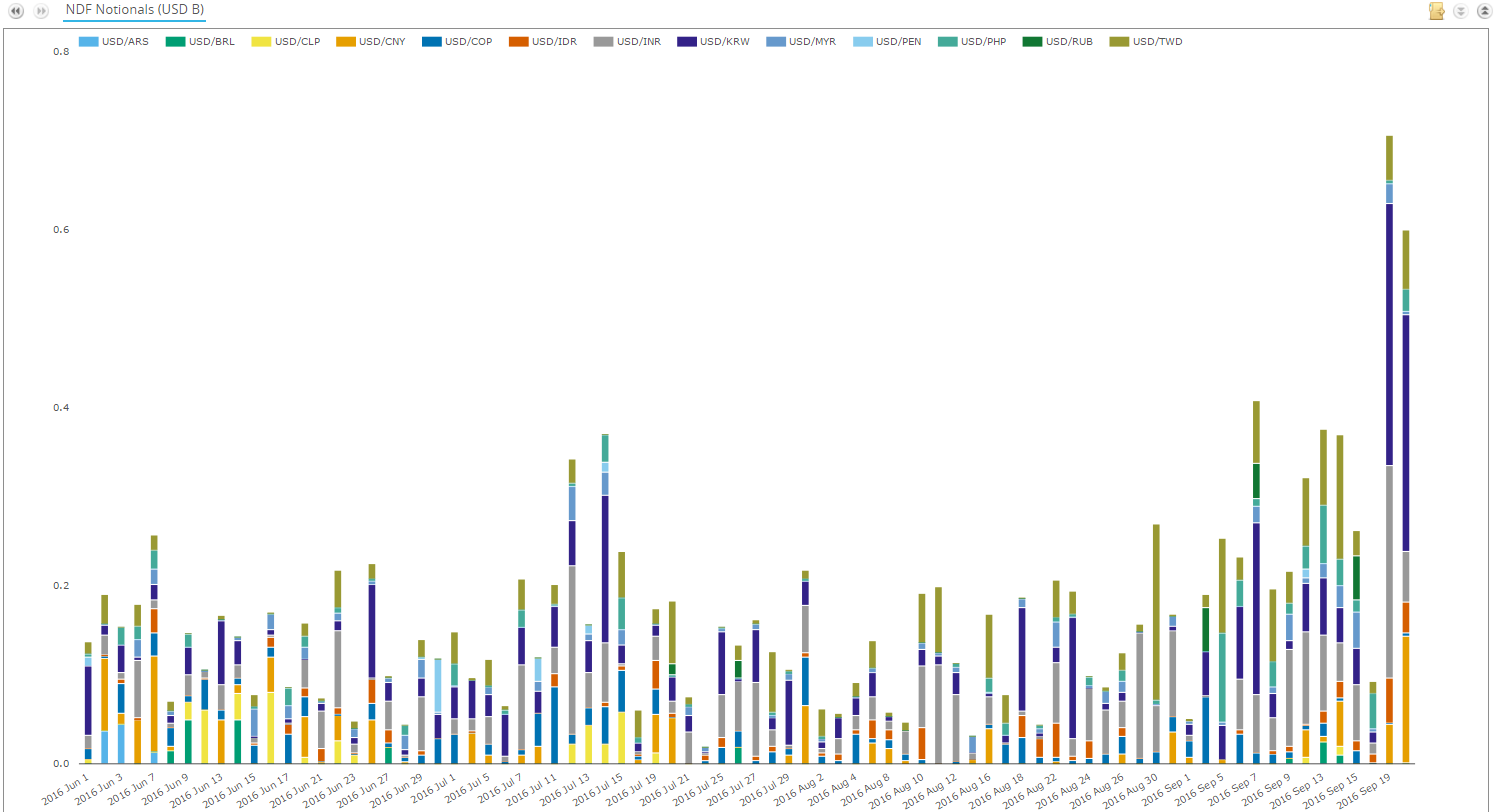

So, the global data shows a clear pick-up in cleared NDF’s. Let’s remember that the UMR’s only apply to the US and Japan at the moment, so we might expect the US SDR data to account for much of this. This next graph is cleared notional trade activity from SDRView:

This also shows a similar pickup in clearing in the month of September. However, the scale of change does not account for the global increase. If you remember back a few charts, LCH saw nearly $11 billion of cleared NDF on Sep 20. US-based SDR data shows only $0.6 billion for the same day. That is to say, the data tells us that the global movement towards NDF clearing is not necessarily coming from the new rules in the US.

So, what is driving the activity at LCH in the month of September, if it is not US-named businesses more actively clearing NDF’s?

I can think of some possible explanations for why this may not compute:

- The growth is from US-named business, but US banks and SEFs (as reporting counterparty) are simply not flagging the trades to be cleared

- The growth is from US-named business, but new trades are executed as bilateral and are cleared later in the day, due to STP for NDF’s not being readily in place

- The growth is from US-named business, but it is proper backloading of seasoned NDF’s

- The growth is from US-named business, but in some Overseas affiliate that is not trade-reporting, but is subject to UMR

- The growth is from major firms in all jurisdictions, given that the writing is on the wall when it comes to clearing efficiency

If anyone knows, please leave a comment for us.

Summary

There you have it. A few weeks into the new Rules, and we have clear evidence of behavioral changes for Inflation swaps and NDF’s. The only other clearable product that is not clearing-mandated is swaptions, which has yet to show signs of clearing activity. But cleared Inflation and NDF’s have been available for longer – perhaps its just a matter of time.