- Conversion to the MXN RFR (F-TIIE) has commenced at CME.

- This has kick-started MXN OIS trading, with over 80% of swaps now reported versus F-TIIE.

- MXN is the 8th largest swaps market in the world.

- We have seen take-up of SEF trading by customers, with Tradeweb now enjoying a 30% market share.

I have not written about MXN Swaps since January 2020 – nearly five years! This blog couldn’t come at a more opportune time, with the MXN market undergoing a big change this week.

CME Conversion

Why the sudden interest in MXN after five years? It is those pesky Risk Free Rates (RFRs) again. MXN was not one of the eight currencies that we monitored in the RFR Adoption Indicator, but that doesn’t stop it from having its own reform agenda! And CME have just kicked off the job of converting outstanding 28-Day TIIE swaps:

This is a particularly interesting conversion exercise as, prior to this week, we haven’t seen much F-TIIE (the MXN RFR) reported to SDRs. Given there are so few trades, it is super helpful that CME have published the market standards for these new OIS trades. Summarising the new standards:

- Spot starting T+2

- 28D rolls (again! really Mexico?!)

- Floating Rate Index: MXN-TIIE ON-OIS Compound

- ACT360 both sides

- Following business day

- Settlement delay T+1

- PAA/PAI (in clearing) calculated at MXN-TIIE ON-OIS (i.e. this is the curve that you use to discount a cleared MXN OIS)

It looks like the market has chosen to persevere with the 28 day “lunar” calendar. Are they just trying to keep quants and vendors of 50-year lunar calendars happy? I have no idea why the MXN market is so tied to this convention, but Swaps traders must now associate Mexico just as strongly with lunar calendars as they do big hats and the Day of the Dead!

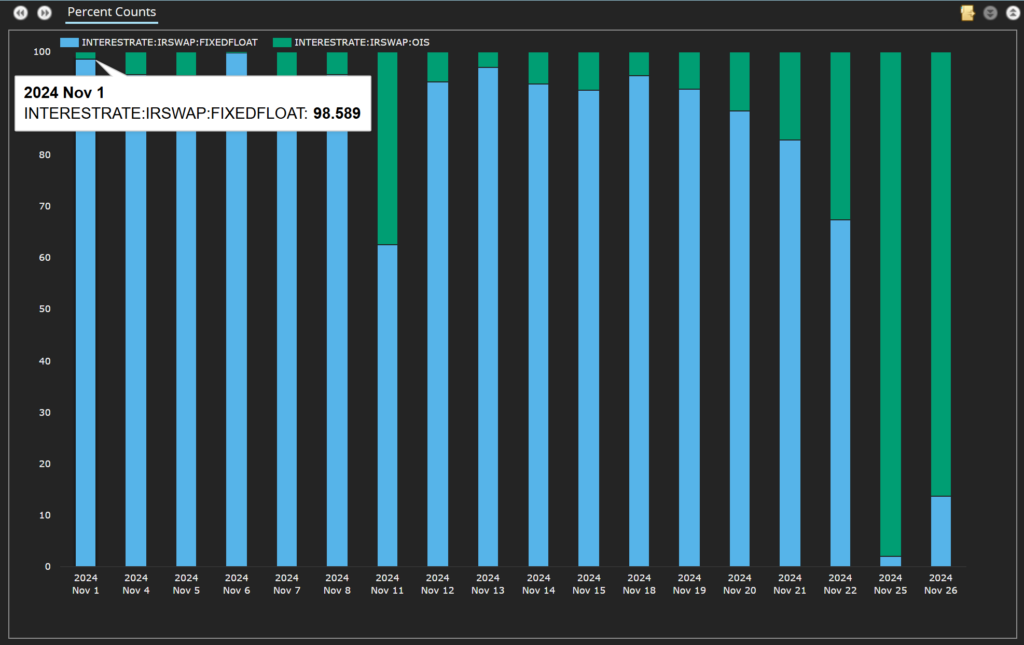

This first wave of conversion has seen trading in MXN OIS commence, with over 80% of trades reported versus F-TIIE so far this week:

In terms of the conversion, I am trying to make sense of the data as we go to press. The Open Interest at CME in MXN IRDs across both IRS and OIS appears to have increased by $1.4Trn last week (as opposed to being converted). So, pending an update, let’s just all be aware that the conversion exercise has taken place and that we now have a market in MXN OIS for the first time.

MXN is the 8th Largest Swaps Markets

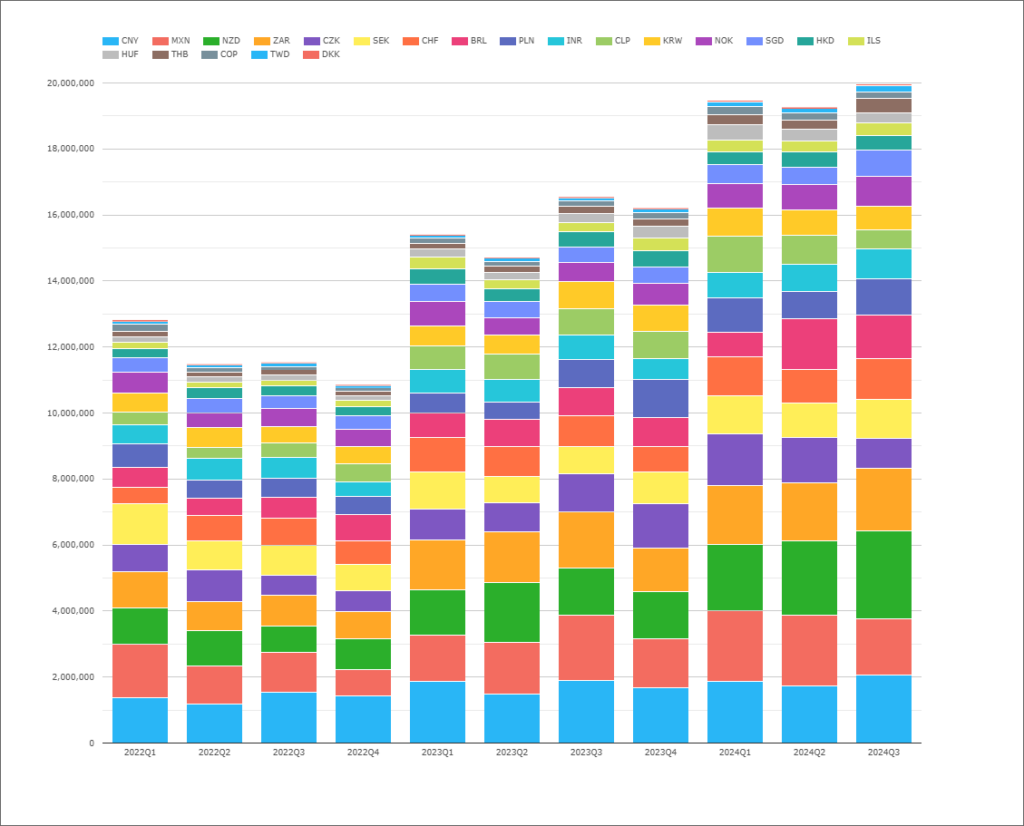

Why should we care about conversion in MXN? Because it is a really significant market:

Showing;

- Volumes in Cleared Interest Rate Derivatives from CCPView.

- The chart excludes the top six currencies by volumes (USD, EUR, GBP, JPY, AUD and CAD). These six currencies tend to represent over 95% of total cleared volumes (see Four Trends in Swaps Data).

- MXN has been the eighth largest currency in 2024, representing 10% of the volumes shown in the chart.

- MXN has seen an Average Daily Volume (ADV) of $31.4bn to the end of October 2024.

- NZD has been the seventh largest market this year, with 12% of the volumes above.

- This is quite different to five years ago when SEK was the seventh largest currency. CNY at 10% (rounded up) and ZAR at 9% round out the top ten currencies so far in 2024.

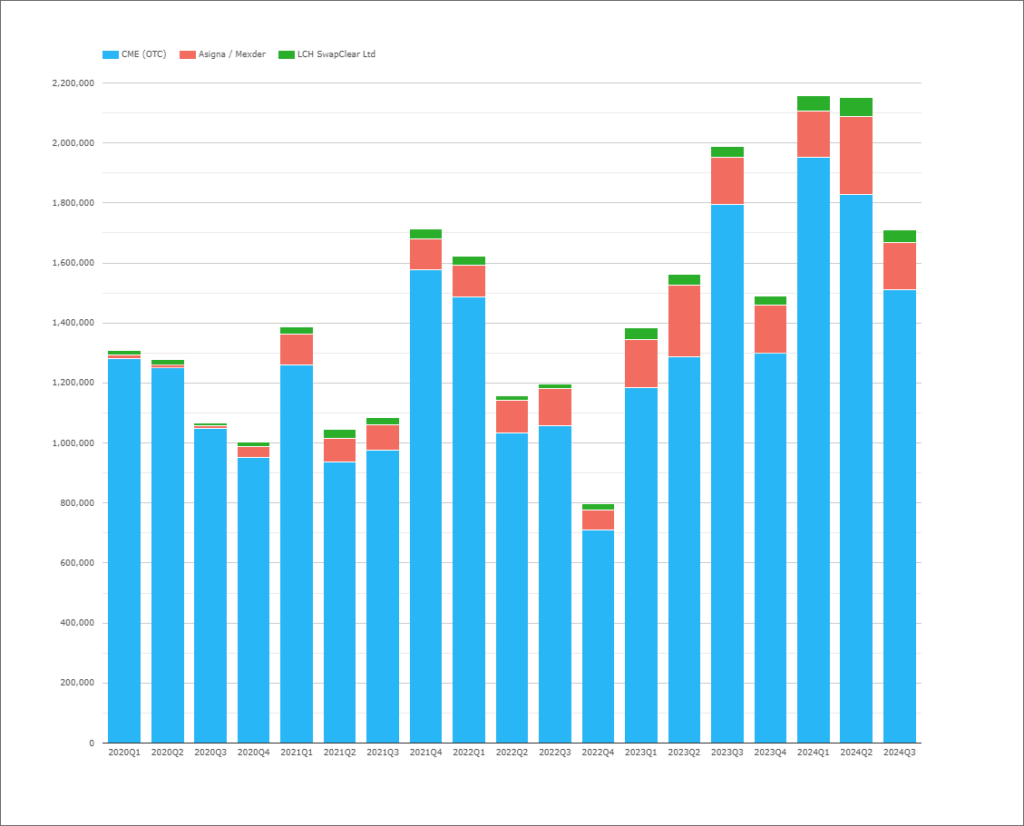

CME Dominates the MXN Market

CME enjoys a dominant market share in the cleared MXN Rates market, but Asigna/Mexder, a domestic CCP, has made in-roads in the past five years:

Showing;

- CME are the dominant CCP in Cleared MXN IRS, with a 90% market share.

- LCH SwapClear support MXN, but their volumes are very small, with less than 2% market share.

- Volumes at Asigna/Mexder have increased and now represent about 10% of the market.

- A note on volumes – they are really flying. Both Q1 and Q2 this year appear to have hit all time record volumes.

Is Clearing Still Popular in MXN?

The MXN market has always been characterised by a healthy appetite for clearing – maybe there are particular credit concerns for some local counterparties? Either way, we see clearing rates of nearly 95% in MXN swaps for 2023 and 2024.

Interestingly, the clearing rate dropped down to 75% in 2021 and 2022. It is not entirely clear why, but given that this was when MexDer started to see more volumes, and they were registered as a Foreign Board of Trade with the CFTC in May 2021, it may be related.

Such a healthy appetite for clearing should bode well for conversion exercises and for transition to the MXN RFR.

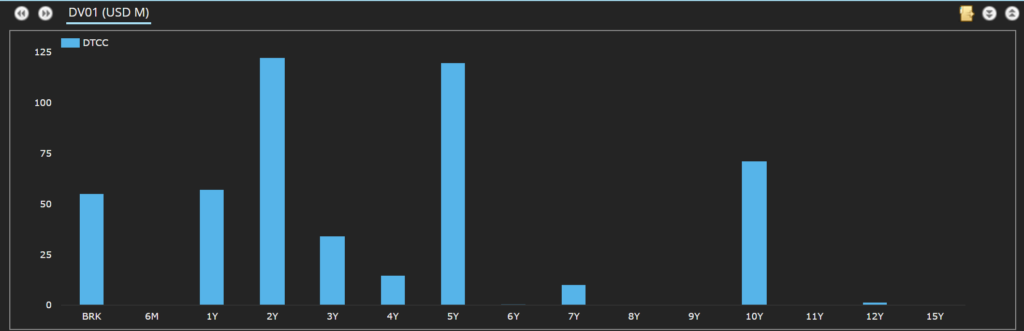

DV01 Traded

There has been significantly more short-end trading in MXN in 2024 than when we last looked in 2020:

Showing;

- Risk has been evenly split between 2Y and 5Y tenors so far this year.

- Even including 1Y and 10Y buckets, the split between short-end and long-end is very even.

- The distribution of risk highlights how standardised trading is, and particularly concentrated in benchmark tenors in MXN.

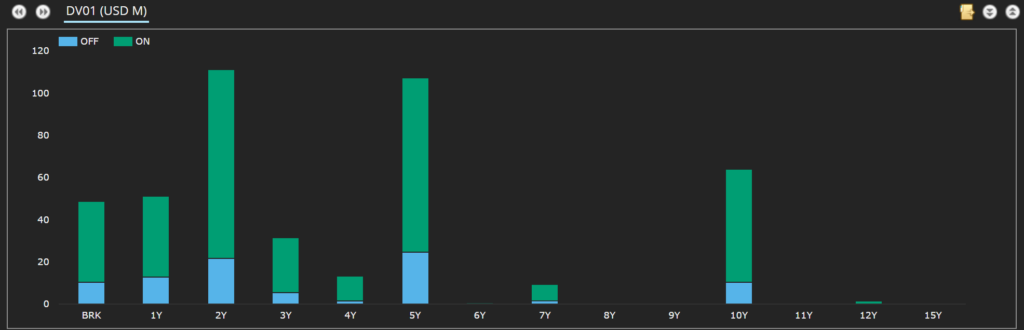

80% of Risk is Executed on-SEF

SEF trading, consistent with the standardised nature of the market and the strong appetite for clearing, is very popular in MXN Swaps. 80% of total risk reported to SDRs has been executed on-SEF so far in 2024. This doesn’t really change if you look at short-end or long-end swaps:

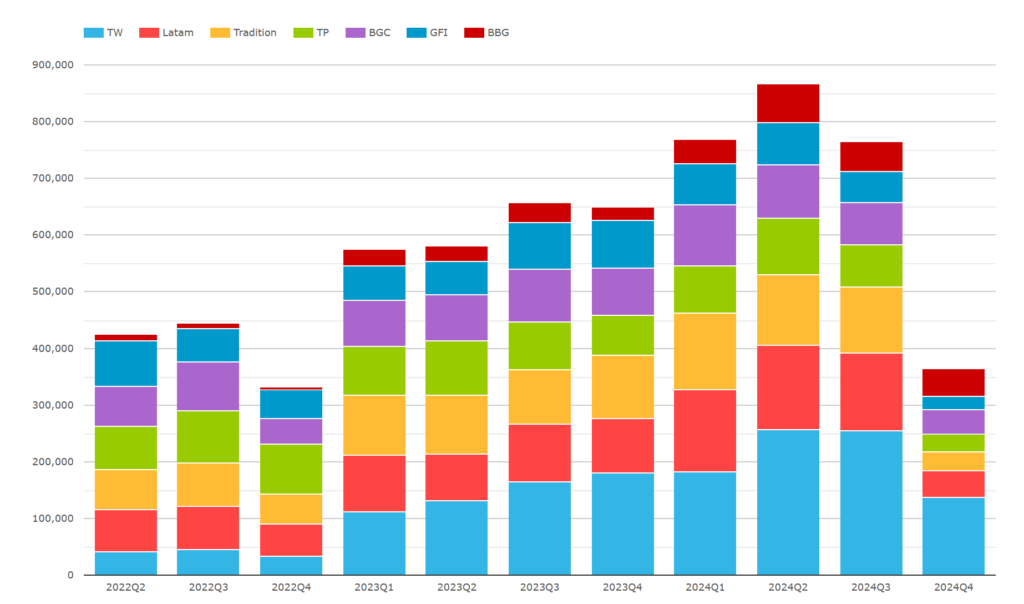

Welcome Tradeweb to the MXN market!

Looking at SEF market share, I noted last time that D2C SEFs were conspicuous by their absence. As we have seen in almost every other market, that has changed with increased adoption of MXN trading on Tradeweb:

Showing;

- Tradeweb now have a 30% market share in MXN swaps (2024 data until end of October).

- Bloomberg SEF also sees MXN volumes, with an 8% market share in 2024.

- The D2D SEFs are jostling for position as number one.

- Latam SEF has seen 17% of the market and is number one for the first time in 2024.

- Tradition are second at 15%.

- BGC (12%), TP (10%) and GFI (8%) round out a significantly different picture to the one we saw back in 2020 for the SEFs.

In Summary

- Times are changing in the MXN swaps market.

- Conversion to the MXN RFR has commenced at CME….

- …creating a MXN OIS market for the first time.

- Clients are now trading on D2C SEFs.

- I won’t leave it another five years before looking at MXN swaps again!

Would love to see this data splitting onshore mexican clients vs offshore. Im sure the market share by platforms will be very different, as well as the CCP market share.

Hi Chris, fantastic article!

One thing that crossed my mind on the MXN $1.4Trn last week increase is that this might be related to the way the conversion was done at CME: one trade was split between two different trades (a short leg still at 28D TIIE maturing on Dec-2025 and another leg with F-TIIE from Dec-2025 onwards). So one 100mm legacy MXN trade is now possibly reported as two different trades, double counting some trades

https://www.cmegroup.com/articles/files/2024/proposal-for-cme-cleared-mxn-tiie-interest-rate-swaps-2024-03.pdf

Best regards!

Thanks – it is almost definitely that. We had the same for the SOFR conversion and managed to calculate an “adjustment” to make sense of it. We will do similar for MXN.