CME in a recent SEC filing noted its intention to start offering Clearing for MXN TIIE Interest Rate Swaps.

So I decided to look at what the data in the DTCC USD SDR shows using SDRView.

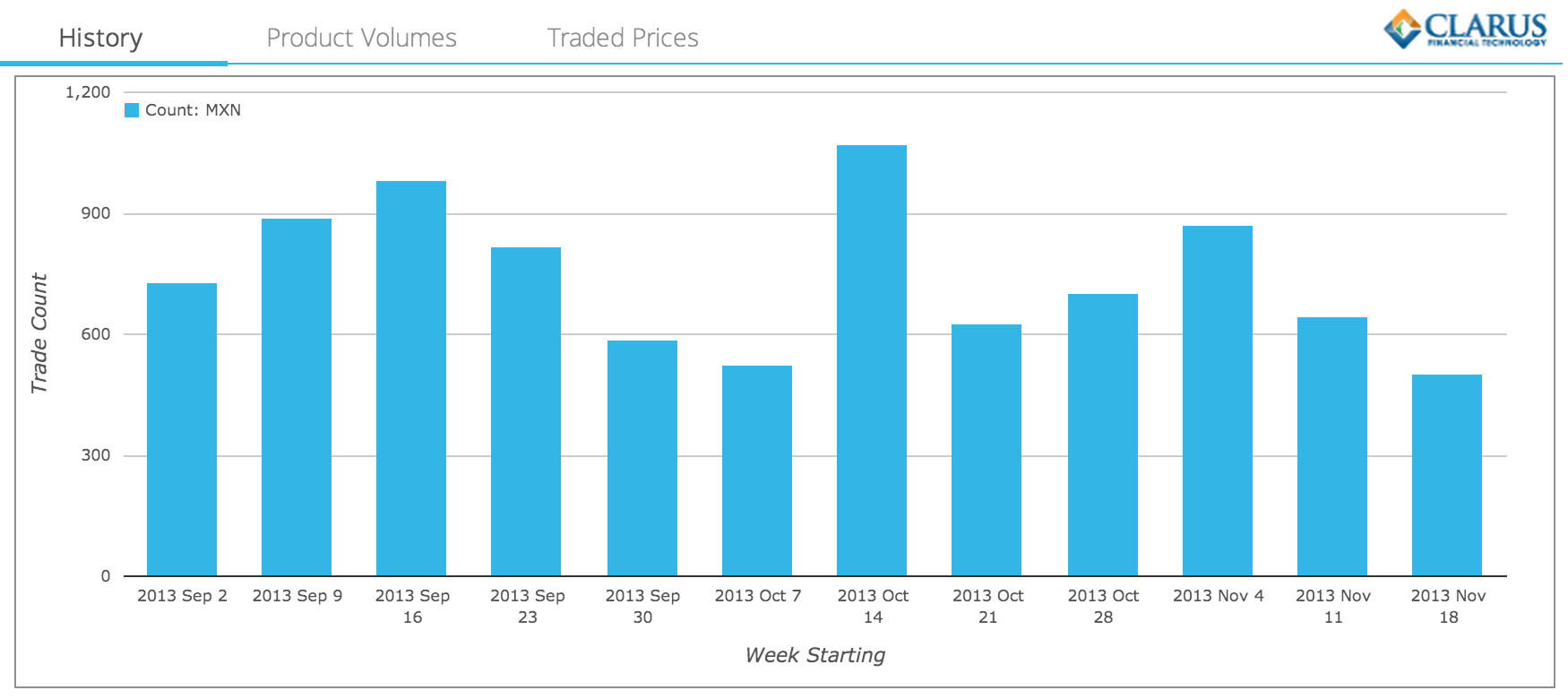

Weekly Volumes

Lets start with weekly volumes using SDRView Researcher, for the prior 3 months.

From this we can see that for the period 2 Sep to 18 Nov 2013:

- The average number of trades in a week is around 750.

- Or the average per day is 150.

- In our period the highest week had 1,072 trades and the lowest 503.

- In-fact the highest single day was 17 Oct with 688 trades.

- All these trades are bi-lateral or un-cleared.

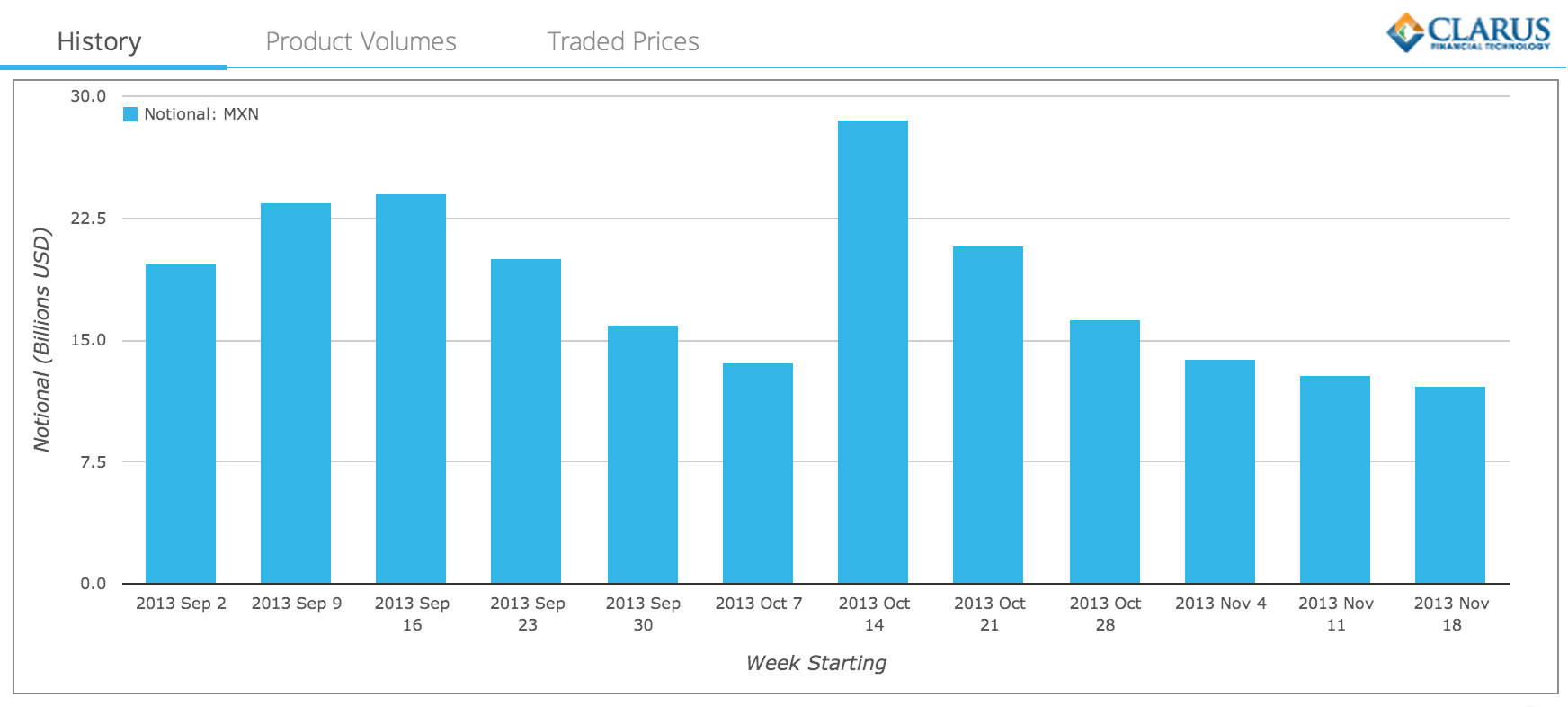

So the trade count is good, but what about gross notional?

Swap Execution Facility

Very interestingly we can see that since Oct 2, a significant portion (60%) of trading is On SEF.

And from the data that SEFs publish (see Week8) the On SEF volume is largely at ICAP.

What Tenors trade?

Using SDRView Professional we can see that on 2 Dec for the Index MXN-TIIE-Banxico 28D, there are 96 trades:

From which we can observe:

- The major tenors are 5Y and 10Y with MXN 5 billion and MXN 2 billion respectively

- The average deal size for 5Y is MXN 200 million

- There are also a reasonable number of trades in 2Y, 3Y, 4Y & 7Y

- The Hi & Low for each tenor are in a tight range

- Allowing a good Swap curve to be built between 1Y and 10Y

- As MXN uses a 28 day coupon frequency, there are 13 periods in a 1Y deal, which is 364 days.

- This means for a 10Y trade, effective date is 3 Dec 2013 but the maturity is 21 Nov 2023.

Summary

There is good volume in MXN Interest Rate Swaps on the TIIE index.

On average $2 billion a day.

Since Oct 2, the majority of trading is On SEF.

So Clearing is overdue.

Follow the data in SDRView to see when this starts.