Last week we looked at the US Markets and Spreadovers, that trade as a spread to underlying US Treasury bonds. These are not the only structures that trade in the market. Other currencies and other strategies yield a variety of alternate structures.

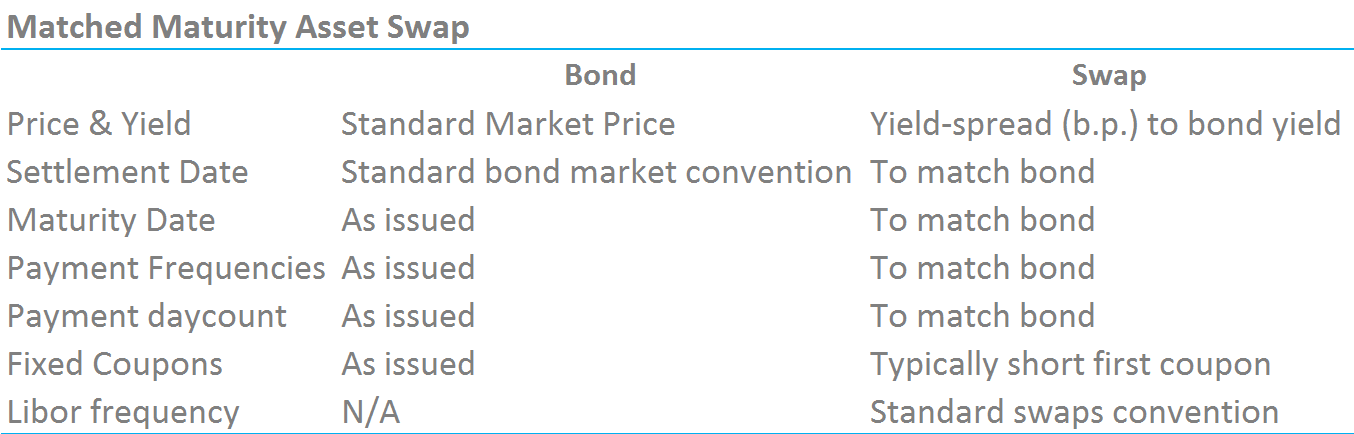

Matched Maturity Asset Swap

In some markets, government bond issuance is nowhere near as frequent as in the US. Instead, governments hold re-openings of existing issues when they need to issue more debt. This has benefits in smaller government bond markets. It concentrates liquidity in individual bonds, and hence reduces the need to roll bond positions between on-the-run issues. However, it reduces the ability of both governments and investors to tailor their maturity exposures and can make it difficult to launch a new issue. The new issues may suffer from illiquidity during the first few auctions, until their outstanding amounts reach sufficient benchmark size.

In these markets, it is more difficult to transfer government bond liquidity directly into the swaps market. If the government bond representing the “5y” point actually has only 4.5 years left until maturity, this may split swaps liquidity equally between the 4y and 5y points. If the yield curve is particularly steep between these two maturities, investors and traders will be wary of exposing themselves to unwanted “curve” risk through a mismatch of bond and swap maturities.

Therefore, it is possible to trade a government bond versus a swap with exactly matching maturity dates – a so-called Matched Maturity Asset Swap. This may be considered a more conservative way of trading as it minimises the differences between the bond contract and the swap contract by way of exactly matching cashflow dates where possible. This can have added operational and cash-management benefits in the case where a trade may be held to maturity. It also becomes an easier exercise to use bond auctions to move into and out of swap-spread positions as they do not need to be rolled.

These matched maturity asset swaps have a number of utilities:

- Delta neutral way to maintain duration whilst reducing (or increasing) credit exposure.

- Both legs are transacted at-market.

- Simple quotation mechanism (yield-spread).

- Allow swap traders to transfer liquidity between swaps markets and government bond markets without any curve risk.

- Concentrates liquidity in two complementary Rates markets in the same maturities.

- A swaps trader may prefer to increase (decrease) the amount of physical collateral they hold at any time without affecting their overall duration exposure.

- An end investor may prefer to receive a higher fixed rate of interest from the Swaps market than they receive on their underlying bonds. This is particularly the case if they view a daily-collateralised, centrally cleared swap as a higher-rated credit than the underlying government bond.

This liquidity-transfer approach also has added benefits for investors who may only want to trade the swap-leg of the matched-maturity package. For example, with liquidity in swaps existing at the exact maturity date of the underlying cash bonds, investors trading only the swap leg can:

- Maintain government credit exposure as an on-balance sheet cash position, but modify their Rates exposure off-balance sheet.

- Modify their duration exposure between physical government bond holdings without liquidating their cash positions.

- Release physical cash bonds into repo markets or to collateralise other swaps. This rehypothecation of collateral does not have to impact any portfolio duration decisions as they can be synthetically managed using these matched-maturity swaps.

- Synthetically realise profits on a government bond holding without realising the capital gain (depending on accounting treatments!).

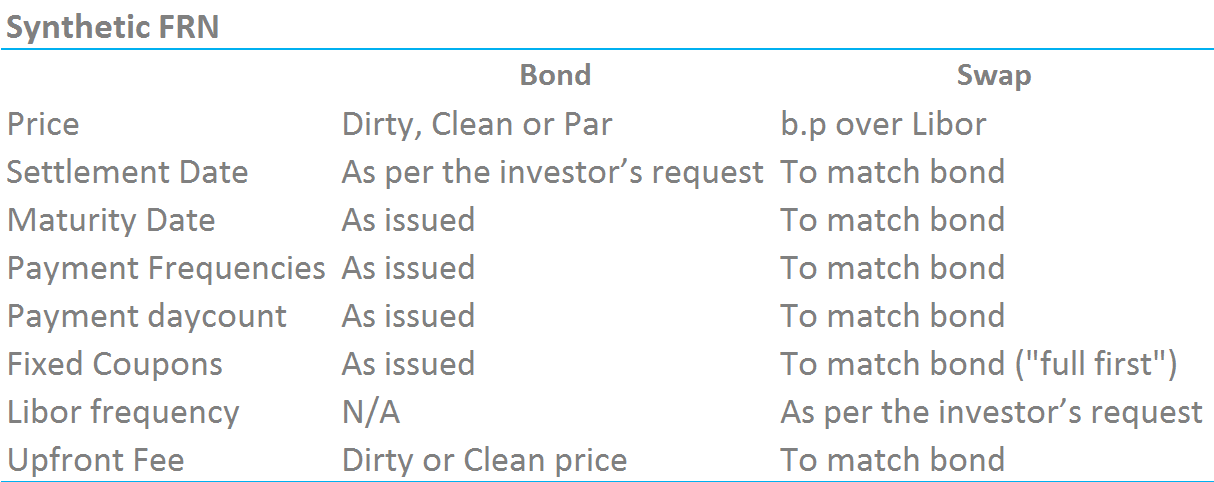

Synthetic FRNs

Taking the concept of a matched-maturity asset swap one step further, we can offset all of the cash-flows of a bond exactly – i.e. including the fixed rate. When we do so, we transfer the yield spread (or more aptly, the credit spread) onto the floating Libor leg of the swap. The spread, thus quoted, hence describes the credit-worthiness of the issuer relative to Libor markets as opposed to government bond markets.

This is liquidity transformation of a different sort. Instead of leveraging separate liquidity pools by maturity and transferring them into different asset classes, this swap allows bond investors to create a synthetic Floating Rate Note (FRN) for any issuer – even if they have never issued floating rate debt.

This can be attractive for a portfolio manager wishing to maintain a duration target through other means (e.g. highly liquid futures or benchmark government bonds), or to maintain credit exposures whilst reducing (increasing) the duration of their portfolio. They retain the full credit exposure to the issuer by way of holding the physical bond, but have hedged their exposure to long-term interest rates by translating the bond into a floating rate exposure.

In the current environment of ZIRP and QE-fuelled all-time lows in yield, it can be very attractive to shift rates exposures into floating rates if investors think markets are showing a distorted expectation of future monetary policy.

These types of trade are most frequently employed against a non-government credit.

As we highlighted above, because issuers prefer the certainty of issuing fixed rate debt, the pool of available FRNs is much smaller. However, entering into a swap with highly customised features to match the underlying bond allows investors to synthetically create FRN exposures from any fixed rate bond. If you are a long-only fund, this can be particularly attractive in a rising rates scenario.

Optical Spreads

Last week, we touched upon how US government bond spreads trade. I term these “Optical Spreads” as they look like you are trading a 5y bond versus a 5y swap. In reality, the exact maturity date of the current 5y bond is unlikely to exactly match that of a 5y swap, and hence it only looks like a 5y vs 5y due to the terminology employed.

In markets where the on-the-run versus off-the-run liquidity premium can be significant, liquidity rules-all and hence we see these (slightly) mis-matched packages trading. For most traders and investors, the benefit of being able to get in and out of these trading strategies at the tightest possible bid-offer spreads is the most important aspect. This means that these positions may have much shorter holding periods than the other strategies outlined above.

What about convexity?

As a final, geeky nod to market inefficiencies, it is worth noting that only a Synthetic FRN counters the sticky question of convexity. Because we are dealing with two asset classes that have different yield curves, the way that one leg of the spread reacts to a change in rates is inherently different to the other leg. Therefore, over time (or as a consequence of particularly large moves in rates), we may need to rebalance our hedges to maintain a true duration neutral exposure.

This of course says nothing about the outright bias to most spread trading strategies – such as US government swap spreads tending to widen as a result of a flight to quality bid for bonds, or corporate credit spreads widening as rates go higher (and hence monetary policy tightening).

And the data?

By their very nature, we are dealing with complex and customisable swaps here. US Persons are still required to report their transactions (and in some case transact on-SEF), therefore we can look for these precise trades in the data. One idea to identify synthetic FRNs would be to compare TRACE data for Corporate Bond trades with the maturity dates of swaps possessing a spread on the floating leg. Another is to look for Gilt maturity dates in the GBP swap data (this is a particularly fruitful endeavour).

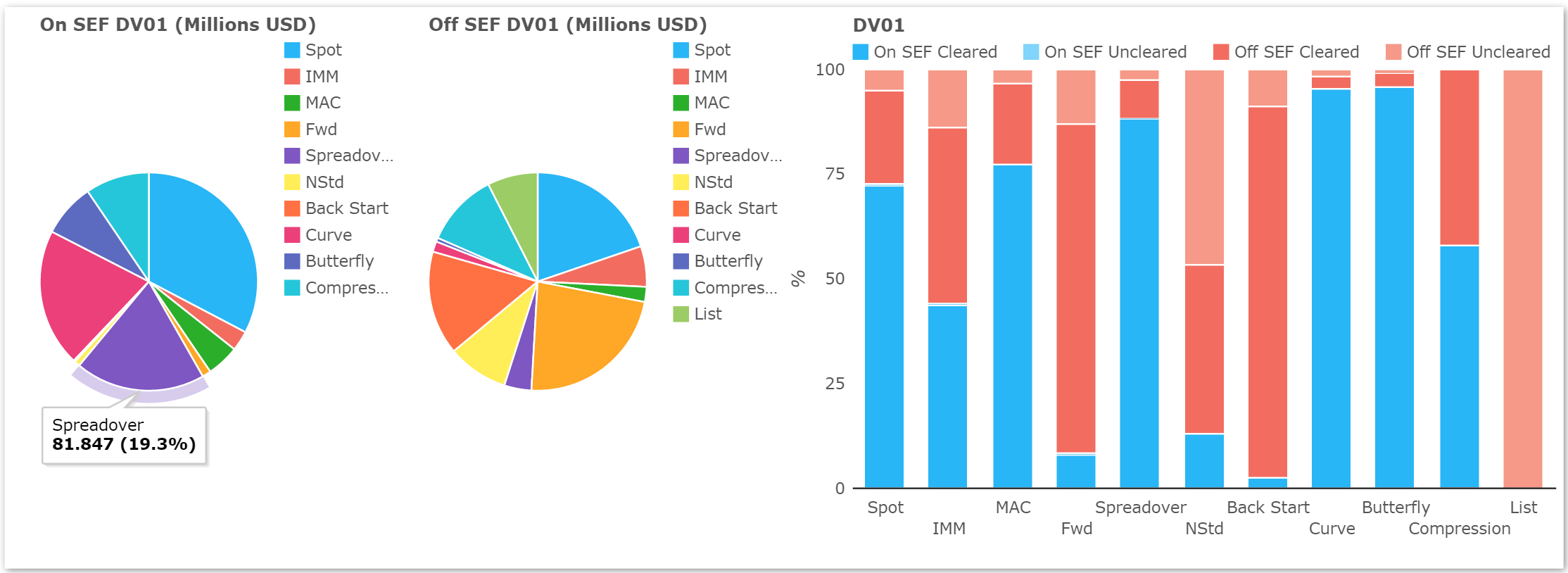

But of course, we make it easiest for the most liquid market, and Clarus reports all of the USD Spreadover trades that we identify in the markets. These are a significant portion of volumes, accounting for nearly 20% by DV01 so far this month: