- EUR/USD Cross-Currency Basis Futures have just been launched by CME, introducing a cash-settled contract that derives its price from FX forwards and short-term interest rate futures (€STR and SOFR).

- Key Mechanics & Pricing Considerations include margining, convexity, and clearing differences versus the OTC market.

- Tight cross-currency basis spreads right now make it an ideal time for market adoption.

- The new futures contract could either complement or compete with OTC swaps. Hedge funds may find it attractive due to multilateral netting and greater transparency, whilst the index provides a valuable funding indicator to the broader market.

CME are taking a bold step into the (relatively) unknown and launching EUR/USD Cross-Currency Basis futures. Let’s take a look…

Definition

The Cross-Currency Basis Future can be defined as;

A contract for difference that cash-settles the implied 3 month cross-currency basis from observable EUR/USD FX-forward, USD and EUR short-term interest rate futures.

Recall that a Cross-Currency Swap is defined as;

An OTC Interest Rate Derivative with physical exchange of notional and interest amounts between two currencies. The physical exchange of the currency amounts occurs on the start and end dates of the swap contract. The interest amounts are calculated according to the outstanding notional amount of each currency and are physically exchanged on every interest payment date for the life of the trade.

Mechanics

How will the Cross-Currency Basis future work?

- CME will calculate a new “index” – the implied 3-month cross currency basis, using EURUSD FX, USD SOFR and EUR ESTR futures contracts as the price inputs observed at 4pm London each day.

- The index calculates the difference between the implied EUR interest rate from the FX Forward and the current EUR €STR rate from CME-listed €STR futures.

- The basis price is expressed in basis points.

How to Calculate The Basis

The CME have some excellent materials on Cross Currency Basis, Understanding Basis Futures and Covered Interest Parity. I discovered that Basis dates all the way back to John Maynard Keynes (1923!), which is quite embarrassing as I had no idea of the origins of the theory during the 12 years that I traded the product!

There are plenty of worked examples in the CME materials, but I will take the opportunity to explain the calculations through a different lens. Here is my spreadsheet:

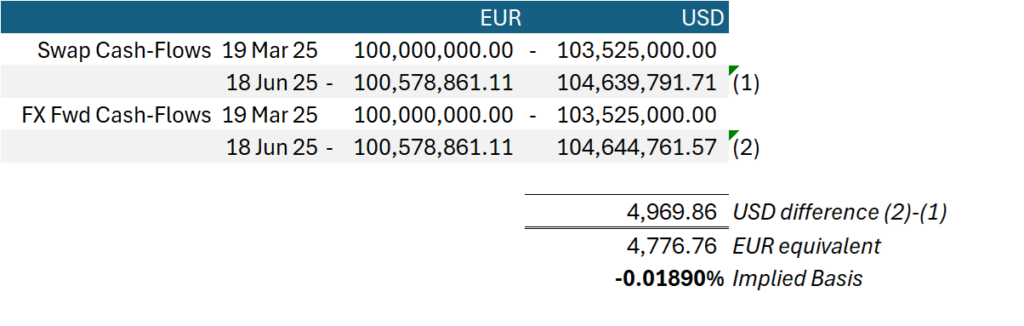

My inputs use current market rates;

- Front ESTR (Mar25) at 97.71, implying a 2.29% yield (100-Rate).

- Front SOFR (Mar25) at 95.74, implying a 4.26% yield.

- Front EURUSD future (Mar25) at 1.03525 and second EURUSD future (Jun25) at 1.040425.

The first two rows of the spreadsheet above model a single period currency swap traded at SOFR flat and €STR flat. If I borrow €100m EUR between 19th March 2025 and 18th June 2025, I will pay 2.29% in interest for 91 days. In return, I receive 4.26% interest in USD for lending the equivalent amount of USD ($103.525m using the Mar25 FX rate).

What happens if I try to replicate exactly the same cash-flows using FX Forwards instead of a swap? The EUR legs offset perfectly. But I am left with a difference in the USD amounts. $104,644,761.57 is returned to me in the FX Forward, but on the swap I would expect to only pay $104,639,791.71.

This is the physical manifestation of the cross currency basis. I am “paid” $4,969.86 more for lending USD into the FX market than I expect to earn in a cross-currency (or loan/depo).

If we convert the $4,969.86 into a fair amount of EUR on the forward date and express as an annualised percentage of the original €100m amount (i.e. remember to multiply by 360/91), you find that the current Cross Currency Basis is tighter than it has been for many a year – at just -0.0189%, or -1.89 basis points.

Please Note!

I am surely not the only one performing these calculations this week as the new contract rolls out? I thought it would be helpful to note a few pricing considerations here:

- €STR and SOFR futures accrue between two IMM dates – 19th March until 18th June 2025 in this case. This is slightly different to when I had my old “IBOR” spreadsheet, which would be looking at a complete 3 month period out of the IMM dates.

- To replicate the Cross Currency Basis future calculation, you could trade:

- 1 SOFR future, with daily margin payable in USD.

- 1 €STR future, with daily margin payable in EUR.

- 2 EURUSD futures (Mar and Jun 2025 contracts), with daily margin payable in USD.

- BUT, this is slightly different because the Cross Currency Basis contract itself attracts daily margin in USD. There will always be a variable USD vs EUR funding balance to fund.

- This is kind of cool because Cross Currency Swaps traders love this complexity (ask me how I know?).

- You cannot exactly replicate the Cross Currency Basis in OTC space, because:

- The single period swaps in SOFR and €STR will be convex (the value of a basis point is not exactly equal to the $ or € 25 tick value of a SOFR futures contract).

- The accompanying FX Forwards (to Mar and Jun IMM dates) will probably be bilateral (i.e. uncleared) and collateralised as part of a bilateral CSA. They most likely attract daily margin in cash USD or EUR, but it will vary from counterparty to counterparty.

With the XCCY Basis so tight, market conditions present a great opportunity to build liquidity in this product because there will be almost no observable pricing difference between ETD and OTC markets. Just be careful it is accurately priced!

Transparency and Evolution

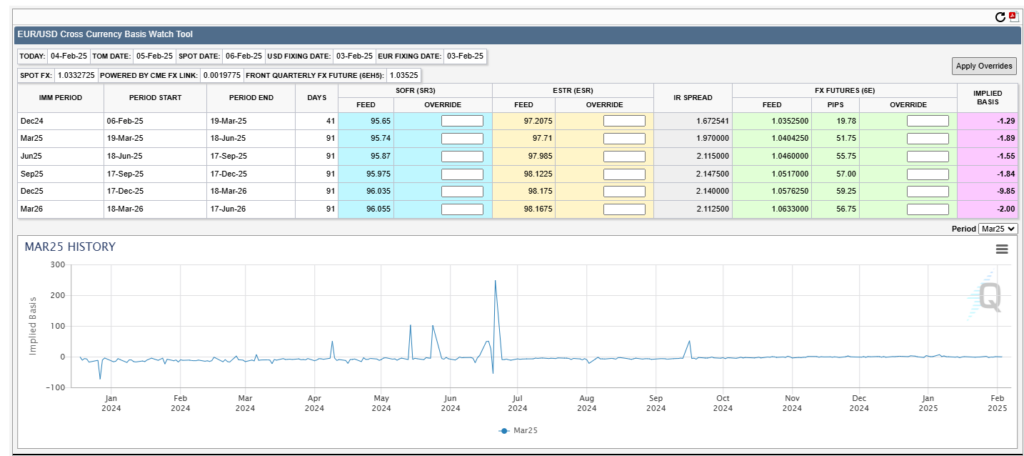

I really like the CME Basis Watch Tool – finally I don’t have to fire up a Bloomberg terminal or a spreadsheet to monitor my old market:

Use Cases: A New Competitor or a Complementary Tool?

Does this product compete directly with OTC Cross-Currency Swaps, or does it carve out a new niche? It’s a complex question, and my key considerations include:

- Physical vs. Financial Settlement

Cross-currency swaps are traditionally physically settled, with the premium reflecting the cost of transferring funding positions. This raises a fundamental question: Can a cash-settled (financially settled) product truly compete with, or at least complement, the OTC physical market? - Hedge Fund Activity & Market Preferences

The sustained presence of hedge funds in the OTC market—particularly those trading forward-starting cross-currency swaps with mandatory break clauses—suggests that physical settlement isn’t always essential. If market participants are already comfortable with synthetic exposure, could this new futures contract gain traction? - Basis as a Funding Indicator

Beyond direct competition with swaps, the cross-currency basis itself is an invaluable funding indicator. The transition to risk-free rates (RFRs) has removed the role of LIBOR-OIS spreads as a gauge of financial stress. In this landscape, basis could step up as a critical benchmark for funding conditions. - Cleared Trading & Multilateral Netting

Hedge funds may find appeal in this product as it enables them to benefit from multilateral netting, which is not possible in the bilateral market. - Extending Along the Curve

A final consideration: Can a financially settled futures contract gain traction across longer maturities? The shape of the basis curve does not suggest that there is a premium for long-term USD funding these days (yes, 50Y EURUSD, I am talking about you!).

And Finally….

Mechanics of Cross Currency Swaps sits proudly in our top three blogs of all time. As an ex-cross currency swaps trader and author of 500+ blogs on clearing, market infrastructure and changes in our industry of course I was going to blog on Basis futures! I hope that I will also be able to provide updates on their traded volumes in the future.