I last looked at Latam swaps back in February this year, with the focus on Interest Rate swaps. We learned that both BRL and MXN swaps had migrated to a primarily cleared market at CME. We also then looked at CME margin requirements for these swaps and noted they were more expensive than similar USD swaps.

Today I wanted to both update the data, and expand it to look at both the IRS and NDF markets. Lets have a look.

Interest Rate Swaps

First, updating the Fixed/Float swaps volume for the 6 Latam currencies:

This tells us that really only BRL, CLP and MXN have much data.

I want to focus just on the clearable currences BRL and MXN. If we look at the average daily volume of each of these, in US$ terms:

Showing us:

- ADV of MXN swaps has hovered about US$7 billion

- ADV of BRL swaps to be fairly consistently above US$3 billion, this is up from the roughly US$2bn we noted back in my 2015 article

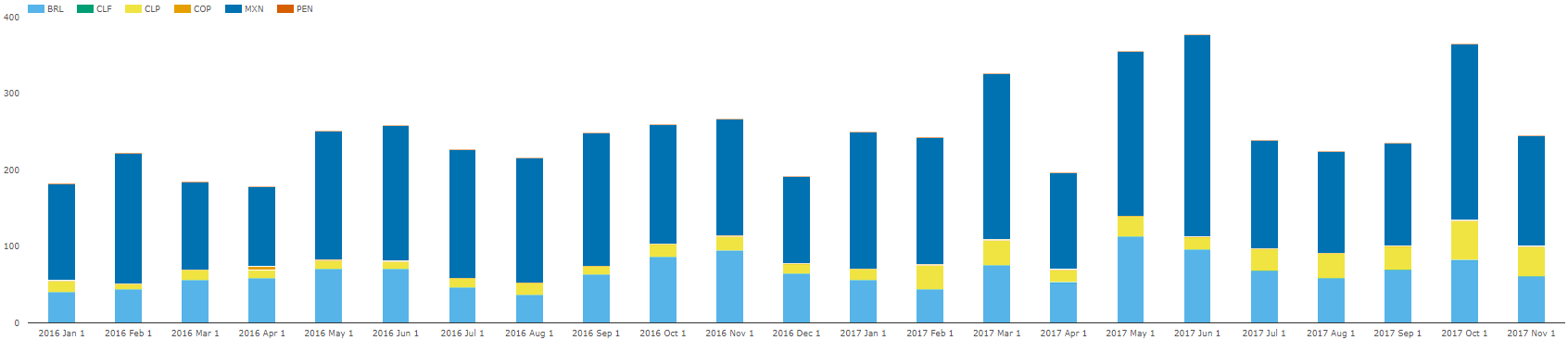

The real notable trend in this data is the amount which is cleared, which we pointed out earlier this year. And it still holds true:

![]()

This shows that nearly the BRL and MXN rate swaps market are now entirely cleared with few exceptions.

FX NDF

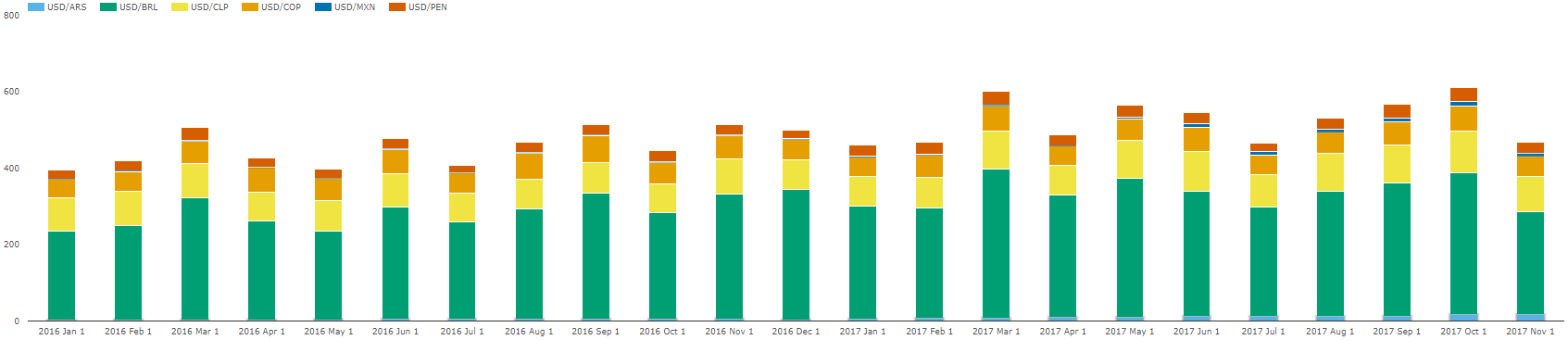

Let’s look at Latam NDF data on the US SDRs:

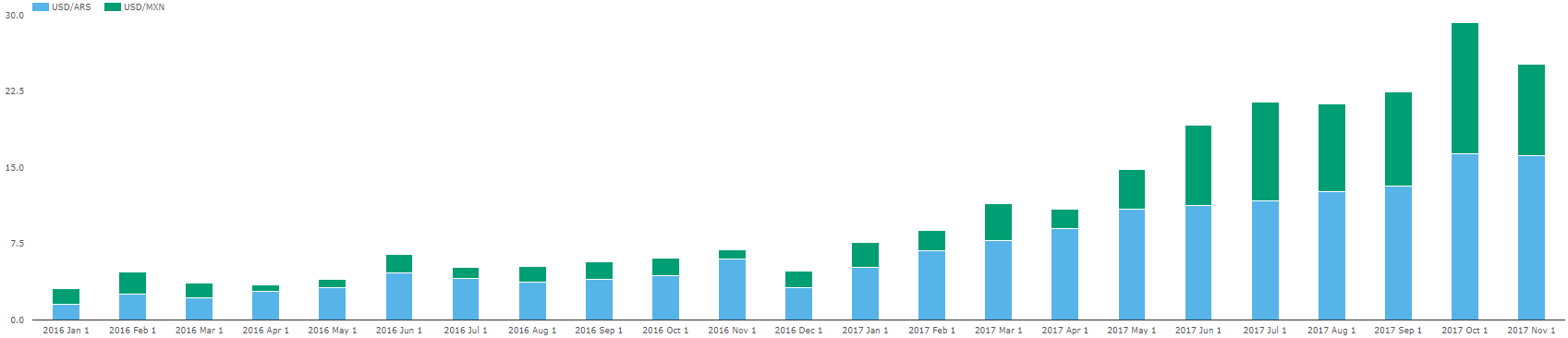

Showing more than half of the volume being in USDBRL, with the balance being in CLP and COP. A keen eye will however see that there are a couple slivers of data that have begun growing in size; in ARS and MXN. Honing in just these two over the past 2 years:

Monthly volumes in these pairs have grown significantly:

- ARS has grown from US$2bn to about US$15bn

- MXN has grown from US$1bn to up to US$12bn

Probably the most notable here is the Mexican peso, as it is not traditionally a non-deliverable currency! I wonder if there are fears about physically settling USD/MXN in the current political climate?

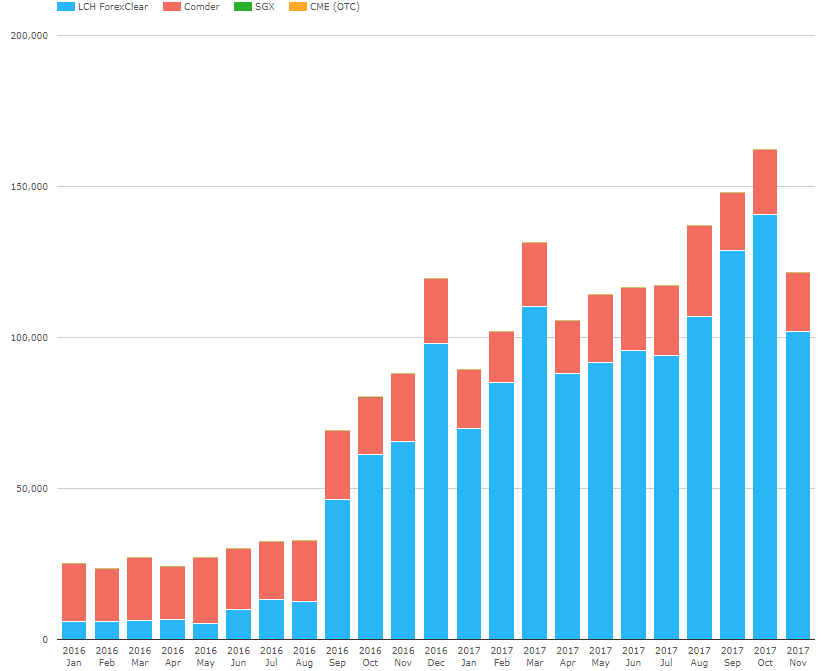

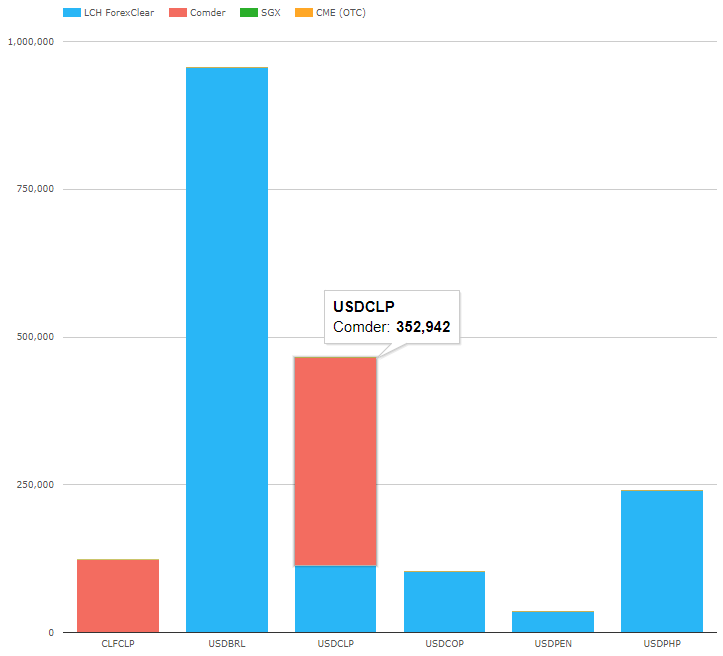

Finally, I wanted to wrap up with clearing data for Latam NDFs. First, monthly volumes by clearing house in millions of USD equivalent:

And next by currency pair:

These show a few things:

- LCH dominate even Latam FX clearing

- Comder handling Chilean pairs

- No USD/MXN is cleared yet

- You’ll see there is a color assigned to CME. Yes indeed, it seems that in the past 2 years, CME cleared some USD/COP – in fact it was about US$1 million worth, on November 22, 2017! Perhaps they are gearing up their FX clearing.

Unfortunately, we do not have a reliable way to see how much of the NDF market is cleared in the market; we believe trades are not being reported to SDRs as “intending to clear” in any consistent manner for trades that end up being cleared. I chalk this up to an operational glitch at the moment.

Summary

We find Latam IRS continue a slight uptrend in ADV, and the shift to cleared IRS is complete in the available currencies (BRL and MXN). It would seem logical that this will extend to further Latam currencies.

Within FX, we find:

- USD/MXN has begun trading as a non-deliverable pair

- USD/MXN however is not cleared

- LCH handling the bulk of NDF clearing

- Comder clearing the bulk of CLP pairs

- CME cleared an FX USD/COP NDF!