- August 5th 2024 saw the highest volumes ever reported to SDRs in a single day.

- I take a quick glance at the data for Rates markets.

This is very likely a premature blog. But it’s August, it’s quiet, and I haven’t written a “live” blog since Credit Suisse went up the swanny.

So whilst Bloomberg is declaring a “$6.4 Trillion Stock Wipeout” and Reuters a “Global Market Rout” I note at the very outset that more sanguine minds rule over at FTAlphaville (a personal bell-weather). They are still publishing about the Gilt Tilt, alongside some early thoughts on the Carry Fissure (bravo for the Star Wars reference).

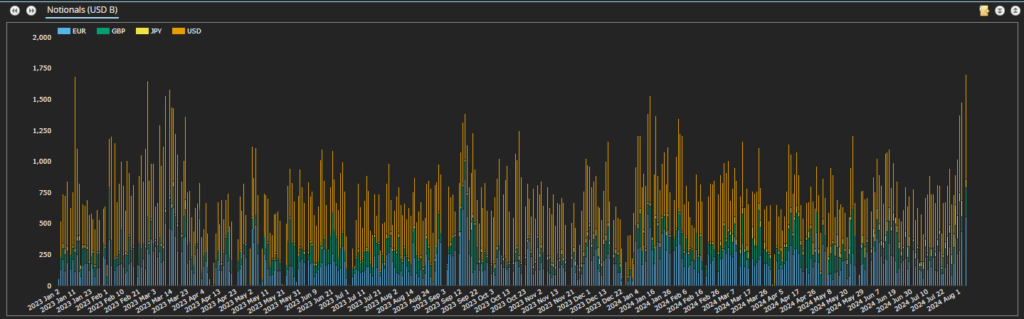

In a typical week, I therefore would stick to publishing my planned blog on EUR Swaptions. But then I checked yesterday’s traded volumes in the SDR:

Showing;

- Notional volumes traded in EUR, GBP, JPY and USD OIS per day since January 2023.

- August 5th 2024 saw the highest volumes traded in a single day.

- Volumes yesterday were at least double the average daily volumes we have seen since 2023, with EUR volumes 2.8 times greater than “normal”.

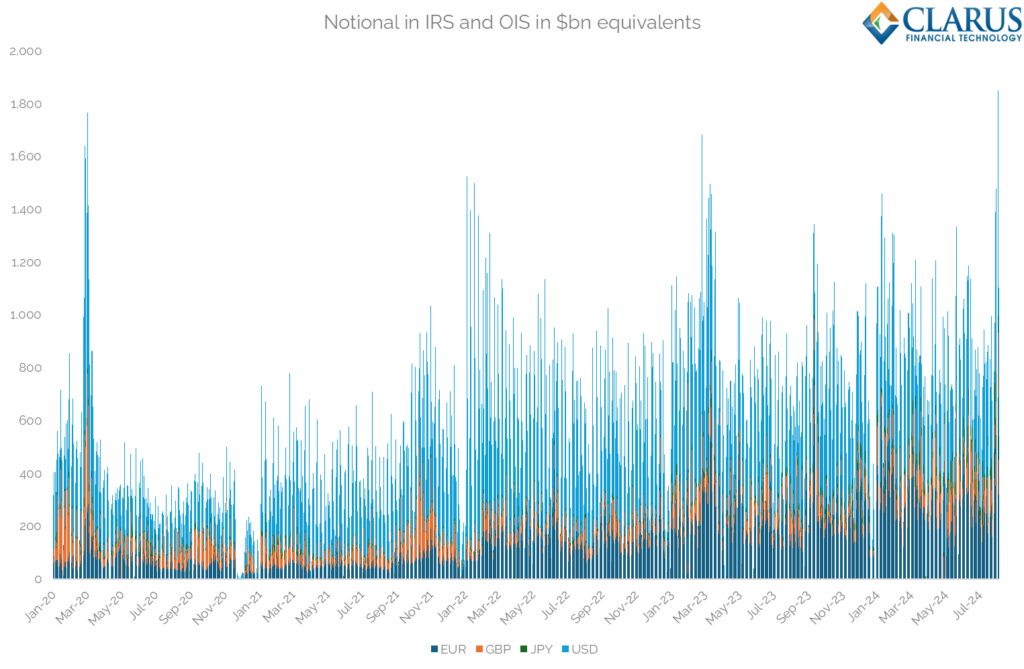

Shockingly, the spike in volumes was higher even than the COVID-induced volatility. Looking at all cleared volumes across both OIS and IRS:

Showing;

- August 5th 2024 saw $1,849bn (i.e. nearly $2Trn) reported to SDRs across cleared IRS and OIS.

- This was in EUR, GBP, JPY and USD.

- This is the highest cleared notional I have seen in the past 4 years, which by extension I think makes it the largest volume day ever reported to SDRs.

- Total volumes will be even higher, given that some trades will be capped at the block/reporting threshold.

- It covers trades executed both on- and off-SEF.

- Actual volumes were certainly well over $2Trn – see below.

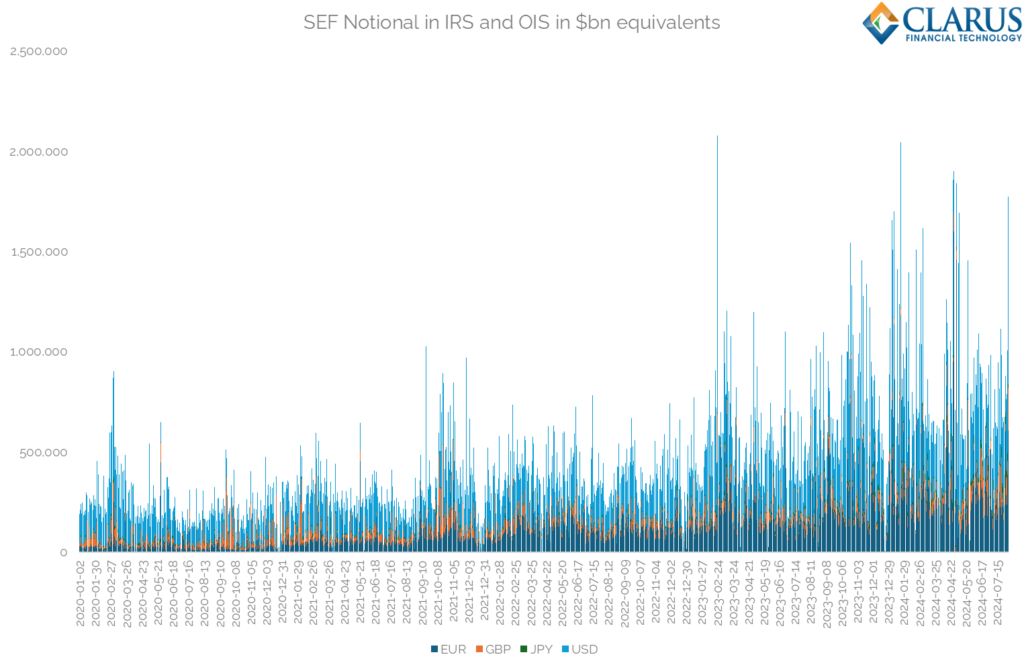

How did SEFs do?

Monday August 5th 2024 was the 6th largest day since January 2020 (and probably all-time) for notional executed on SEF across EUR, GBP, JPY and USD IRS and OIS:

Showing;

- $1,772bn executed on SEFs across EUR, GBP, JPY and USD IRS and OIS.

- These volumes are “uncapped”. They are reported T+1 (not “real time”), and the benefit of the delay is that we see the total volume reported per instrument.

- The ADV in 2024 has been $780bn – so Monday saw ~2.3x larger volumes than on a “typical” day.

- The chart makes it clear that SEF volumes have been increasing since 2020. Some of that will be down to shorter dated trading, some due to increased trading on D2C SEFs etc.

- Of the top ten volumes ever recorded on SEF, 9 have occurred in 2024!

- We have seen over $2Trn trade on SEF twice already this year.

- So maybe Monday wasn’t all that unusual in terms of SEF activity in 2024.

Transparency and Volatility

Since Monday, markets have “recovered“, “rebounded“, “stabilised” (choose your headline accordingly). Desks will be primed for any renewed risk-off moves as the week progresses. But again, OTC markets have been well served by the market infrastructure we now have in place. Clearing scales up in times of stress, transparency proves that markets continue to function, and whilst it is very likely that the price of liquidity increased on Monday through wider bid/offer spreads, there is no evidence that liquidity was in short supply (albeit at an increased cost).

Monday 5th August 2024. Another day when transparency worked as intended.