- An Interest Rate Swap (IRS) is a financial derivative that is widely traded.

- This blog defines an interest rate swap and its practical uses.

- Why the parties involved would choose to carry out an IRS.

- What the possible risks of an interest rate swap are.

About the Author

Jake is 17 years old and studying for A levels. At the time of writing, Jake has recently completed a weeklong work experience with Clarus FT. He was tasked with writing a blog on interest rate swaps, in an easy to read and understandable manner for someone with no prior experience in financial markets.

What is an IRS?

An IRS is an agreement between two parties to swap future interest payments on a set amount of money. Only the interest payment is swapped, not the notional amount, and it takes place over a set time horizon. A classic example of when an IRS may be used is to swap floating interest loans for fixed interest loans. The swap agreements tend to be set up using a counterparty called a swap bank, which typically deals with the transfer of interest payments, and seeks out another party to hedge with.

How does an IRS work?

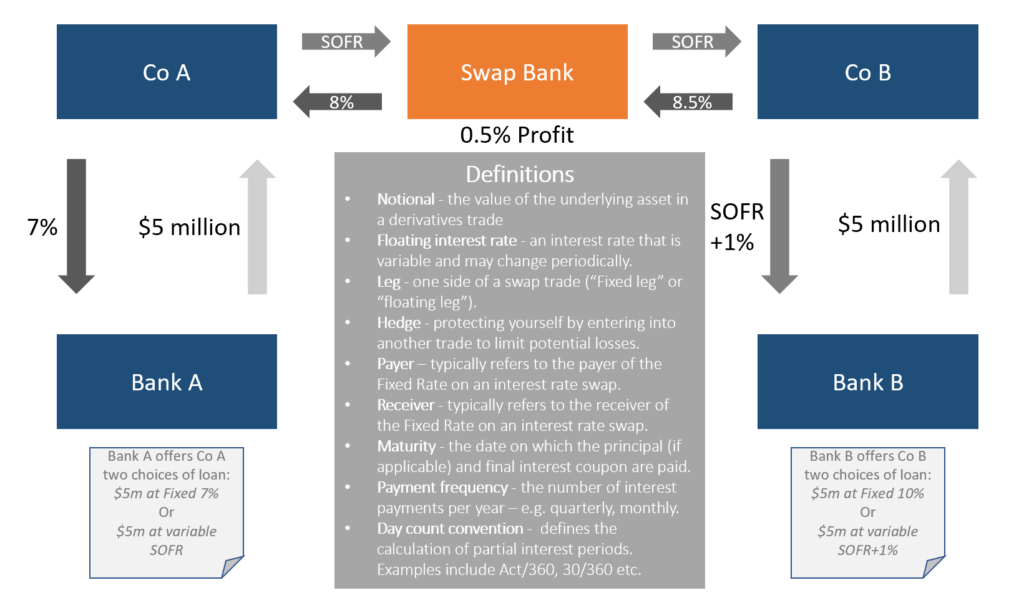

In the example above, Company A (Co A) has the choice of borrowing at either a 7% fixed interest rate, or SOFR[1], on $5 million. Company B (Co B) has the choice of borrowing at a 10% fixed interest rate, or SOFR+1%, on $5 million. Co A chooses the 7% fixed interest rate and Co B chooses the SOFR+1%.

In some cases, Co A and Co B may decide they want to swap into floating or fixed. A swap bank would love to have the pleasure of helping! Co A and Co B approach the bank, and then the bank arranges the terms of the IRS with each counterparty.

Specifically:

- Swap bank pays fixed at 8%, and Co A pays the swap bank SOFR.

- Co A is paying only 7% on the fixed rate loan, therefore is making a gain of 1%.

- This can subsidise the SOFR leg, so that Co A is effectively paying SOFR minus 1% on a floating rate loan. These are better terms than the original terms offered (SOFR flat).

- And what about the other side?

- The swap bank approached Co B and agreed to receive fixed at 8.5% versus SOFR flat.

- The swap bank makes a healthy 0.5% margin, with the floating SOFR legs offset in each swap.

- Co B is now effectively paying a fixed interest rate of 9.5%, a whole 50bp lower than the 10% fixed interest rate originally offered on the loan.

The majority of cases involve swapping fixed for floating, but equally a floating interest loan can be swapped for a different floating rate (known as a basis swap). This is more unusual and we won’t cover it here.

The First Interest Rate Swaps

When researching the project, Clarus provided the following research material, which provided a helpful introduction. Well worth a read:

The paper suggests that the first domestic interest rate swap (i.e. involving a single currency) was conducted in 1982, and involved Sallie Mae.

Other useful references I consulted during the research were:

- Interest Rate Swap Definition

- PIMCO – Understanding Interest Rate Swaps

- And finally, a super helpful video:

Why are swap banks necessary?

You may be wondering why a swap bank is necessary to an IRS, as opposed to the two parties just setting up the agreement between themselves. The reasons tend to be practical.

It is unlikely that Co A would know that Co B also requires an IRS on the same notional amount and over the same time horizon- it’s difficult to have this knowledge about another company! Swap banks have an in-depth knowledge of which parties are looking for which deals, so using this information they can find the best possible match for a party to carry out an IRS. The second main advantage of using a swap bank is that it can allow the parties to remain anonymous.

How do the two parties benefit from the swap?

A counterparty with a floating rate loan suspects that rates are going to increase. They might then want to swap their floating interest rate loan into a fixed interest loan in order to reduce the risk of their interest payments drastically increasing. In this sense IRS is being used to help manage their floating-rate debt liabilities.

However, why would another party with a fixed interest rate loan want to swap to a floating rate loan, if SOFR is suspected to increase? There are two reasons for this:

- This party may believe that SOFR is going to go down in the long term or;

- One company’s comparative advantage can end up being advantageous to both. This is demonstrated in both examples on this blog, whereby a high fixed rate loan can be swapped to yield net floating rates below the reference rate (SOFR in this case). And similarly, a high floating rate loan can be swapped to yield net fixed rates below the reference rate.

| Company A | Company B | ||

| Pays fixed interest rate on loan | 7.0% | Pays Floating Interest Rate loan | SOFR plus 1% |

| IRS | IRS | ||

| Pays | SOFR | Pays | 8.5% |

| Receives | 8.0% | Receives | SOFR |

| Net Costs | SOFR minus 1% | Net Costs | 9.5% |

| Without Swap | SOFR | Without Swap | 10.0% |

| Saved | 1% (100 bp) | Saved | 0.50% (50 bp) |

How do the banks benefit from the swap?

The banks that are providing the loans for the two parties benefit from IRS as it allows them to convert some of their long-term fixed rate loans into a floating rate loan. This significantly reduces interest rate risk, since banks often fund long term loans with short term deposits. Therefore, if interest rates rise, banks will be paying depositors more, yet they will be locked into fixed rate loans. So by carrying out an IRS they mitigate interest rate risk.

The swap bank benefits from IRS, as it earns a small premium for organising and carrying out the entire interest rate swap process. Swap banks tend to make a small profit on each trade, meaning they need a high volume (or notional amount) of IRS contracts.

What are the risks of an interest rate swap?

There are several different risks when carrying out an interest rate swap. The primary risk factor is the underlying interest rate for the counterparty choosing a variable/floating rate of interest.

If moves in interest rates are significant enough, or the underlying loan changes, a counterparty may decide to terminate an IRS. They would typically decide to terminate it if interest rates varied differently to how predicted, making the IRS too expensive/costly. To terminate a swap, both counterparties must agree the termination payment. This compensates the appropriate counterparty for any opportunity cost of losing out on their fixed interest rate payment that is no longer available in the market.

Another option instead of terminating is to enter into an offsetting swap with another market participant to net against the original swap.

IRSs also carry counterparty credit risk, meaning the likelihood of the counterparty defaulting on its payments. However this risk has been reduced, by both Clearing and the posting of Initial and Variation Margin in Uncleared markets.

In Summary

- An IRS is commonly used to swap floating rate loans into fixed interest loans and vice versa

- It’s normally beneficial due to the comparative advantage of one party

- If interest rates change greatly in an unexpected manner, it can lead to losses for one of the parties.

[1] SOFR- secured overnight financing rate is the overnight interest rate for US dollar-denominated loans and derivatives. Or more simply, it represents the amount of interest a bank will have to pay on cash borrowed overnight. For a more in-depth SOFR blog from Chris, please see here.

Wonderful write-up. Good luck to Jake.

Jake, this is a superb write up, and its great to pose a question as you have done to bring it to life. With swaps as a foundation, you can branch into many other areas of finance and different types of contracts, referencing different risks. The exchange of risk is at the heart of most financial transactions.