We’re all aware that in the US, the new Uncleared Margin Rules (UMR) took effect on September 1st. Except they kinda didn’t take effect. There was this chestnut of No-Action relief issued by the CFTC on the day, which, if you just read the headline news reports, meant that the Rules were pushed back 1 month.

Except, if you read the letter, there are 3 key takeaways:

- Category 1 firms are NOT relieved from collecting and paying IM & VM effective Sept 1. (You still have to!)

- You are only relieved from the obligation to hold such margins with a third party custodian (and the legal documents, plumbing, etc supporting that)

- And my favorite tidbit: “This letter… represent the views of DSIO and do not necessarily represent the positions or views of the Commission or of any other office or division of the Commission”. So, what if the Division of Enforcement doesn’t hold this view!?

It seems the 20 or so Category 1 firms complained that they were not quite ready for the Margin Rules, explicitly because they didn’t get the custodian part all lined up. So the CFTC acted by only giving specific relief.

It’s akin to telling your mom you can’t go to school because your toe hurts; only to have her respond by sending you to school in your comfortable teddy bear slippers all day. You got what you asked for, but not what you wanted.

So what this all means, is much of the rules did actually take effect. Hence I wanted to investigate some of the rhetoric:

- Foreign counterparties refused to trade with US names

- Banks would turn to cleared swaps or other (eg listed) derivatives for hedging

- Swap activity and liquidity would be reduced because some banks would execute offshore

- The margin structure for US banks will be non-competitive

- Banks would just choose to not trade (?)

If any of this is true, then it should show up in the data.

Let’s have a look.

DATA

We’re slightly unfortunate that all of this took place over a US bank holiday on Monday Sep 5 (Labor Day). But that just makes it a bit more difficult to discern.

I think it’s relevant to take a simple look at 2 things:

- Uncleared trade counts for Price-Forming Trades

- Indication of how uncleared trades are collateralized

TRADE COUNTS

So to begin, let’s look at the most liquid of vanilla swaps by defining our universe as all price-forming, USD swaps. More specifically:

- Spot, IMM, MAC and Fwd starting swaps (no back-starting, and Non-Standard subtypes)

- Outright, spreadover, curve and butterfly packages (no Compression, List, or Roll trades)

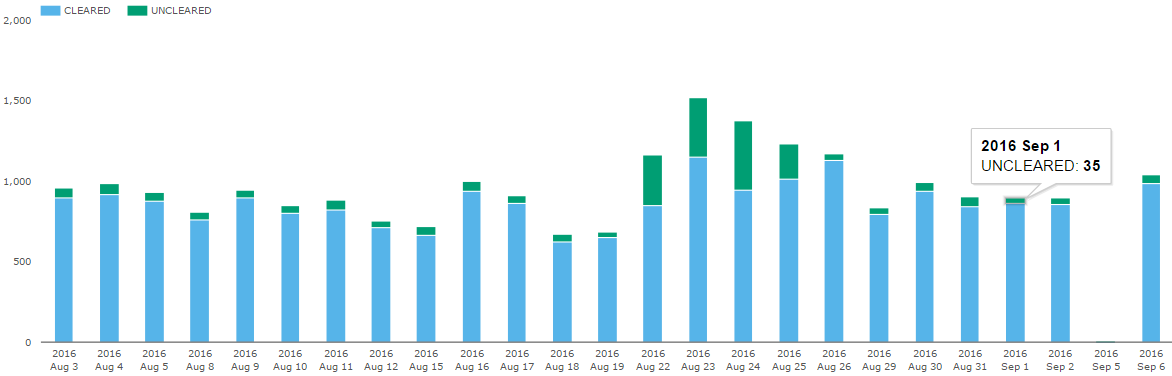

Nothing jumps out here. In fact September 1, 2 and 6 look like fairly normal days in terms of trade counts both cleared and uncleared. And if I go back to Labor day 2015, I see very similar results. I’ll spare you the graph.

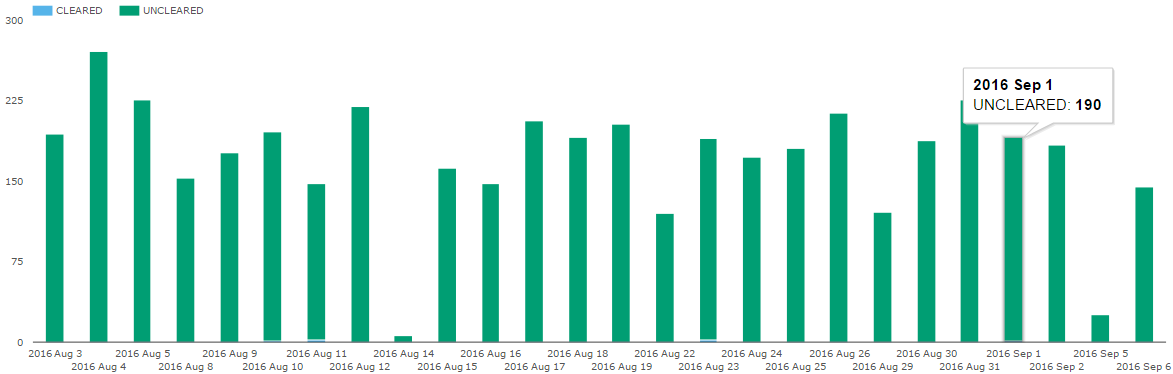

But we should acknowledge that Fixed Float swaps are already the most clearable products out there. The UMR’s impact a much wider universe of products. So let’s look at a few products that are clearing eligible, but with no clearing mandate. Let’s start with swaptions, they are clearable:

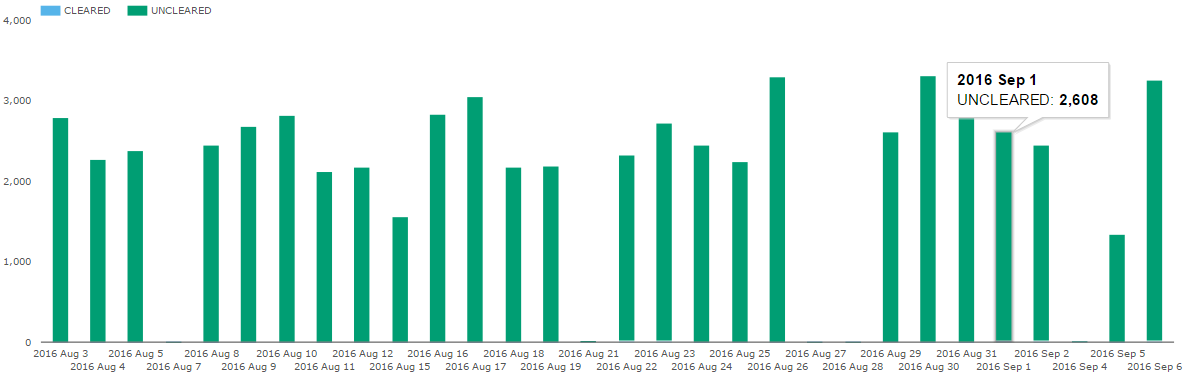

Nothing jumps out there. Trade activity seems stable, and no jump to clearing. How about NDF’s? Sticking to the most active BRL, CNY, KRW:

Also no flock to clearing, and trade counts steady through the mandate period.

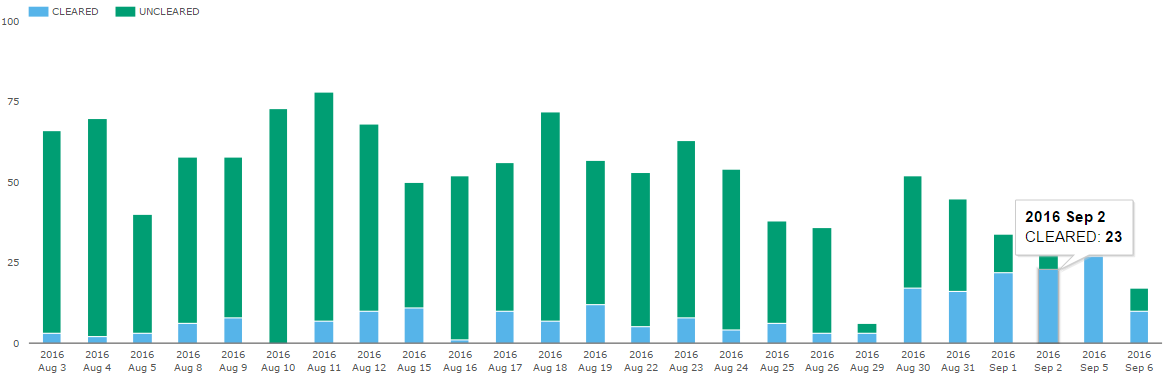

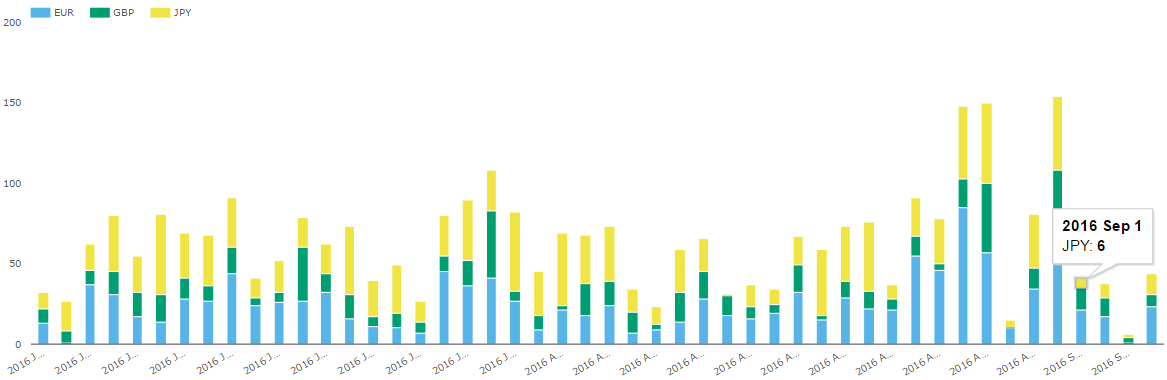

How about inflation swaps (EUR, GBP, JPY, USD):

Slightly interesting, as the cleared trade counts have indeed accounted for about 75% of activity at the end of the month, up from under 15% earlier in the month.

Lastly, what about the truly non-clearable stuff. Take XCCY swaps for example, this time from July 1:

Perhaps some indication here of less US-named business, but we might be stretching it.

In all of this, we might be guilty of simply having too small of a sample size (3 days at the start of a month around a holiday). Though the few comparisons to Labor Day 2015 do not show significant differences.

And once you get past XCCY swaps, the data starts to get very thin.

INDICATION OF COLLATERALIZATION

The other piece of analysis I want to do is to look at the collateralization flag on SDR data. I’ve never done any thorough analysis on this trade attribute – and I do not claim that what I am about to do is thorough – but now is a great time to see if this flag tells us anything.

For starters, some definitions. Every trade has an attribute “Indication of Collateralization” that is set to either:

- FC: Fully collateralized. I take this to be 2-way, akin to what the UMR’s require.

- PC: Partially collateralized.

- UC: Uncollateralized.

- OC: One-way collateralized.

- N/A / blank: I recall SDR’s encourage this to not be blank for uncleared trades.

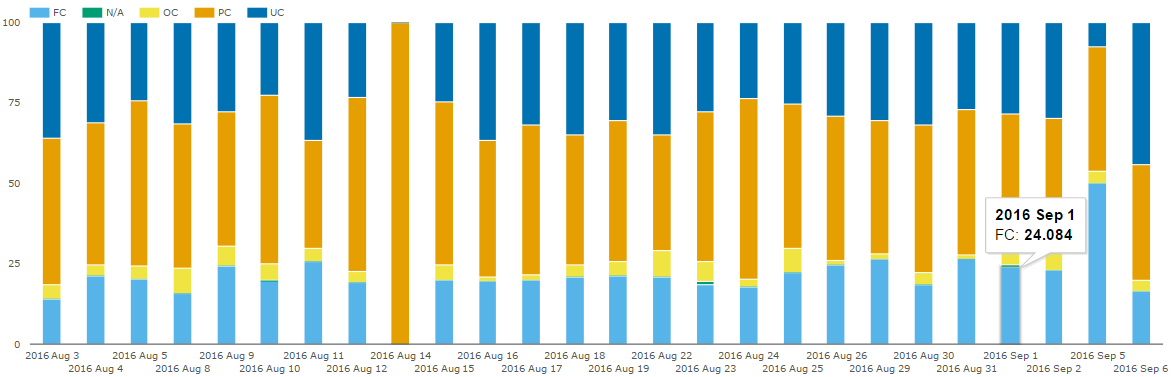

My expectation would be that, upon successful UMR launch, we’d see significantly more fully collateralized (FC) uncleared trades. Here is swaptions:

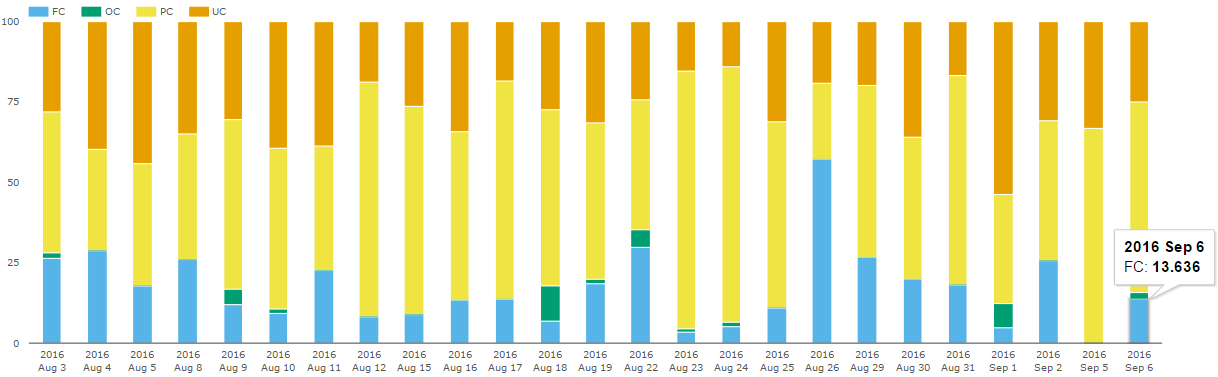

And here is XCCY Basis:

Which does not corroborate the story that suddenly, banks had to fully collateralize their swaptions and xccy swaps. Granted one big caveat here is that this data includes all dealer-to-client as well as dealer-to-dealer transactions. Whereas only a subset of dealer-to-dealer trades would be impacted.

I’ll spare the charts, but I’ve also run this for uncleared NDFs and a few other products, and there are no striking results.

It’s also quite possible that no reporting counterparties have thought to update the SDR trade reporting field for “Collateralization”.

SUMMARY

I set out to confirm the rhetoric that the first day(s) of the Uncleared Margin Rules were difficult on banks and impacted trading activity. What I found:

- Trade counts in clearing eligible swaptions and NDF’s do not seem impacted through the mandate.

- Trade counts in clearing eligible inflation swaps were steady with some growth in cleared counts. A possible, positive, consequence of UMR’s.

- Trade counts in non-clearable products such as xccy swaps might tell a story, but the sample size is very small, and surrounded by a holiday weekend. Comparisons to last years holiday weekend do not turn up anything glaring, particularly given the small sample size.

- The “Collateralization” field on liquid, uncleared trades shows no migration to fully collateralization.

I suppose we’ll need to let this settle down a bit. We’ll be keeping our eye on it.