- The Financial Stability Board, in conjunction with the BCBS, CPMI and IOSCO have launched a broad survey about Cleared derivative markets.

- The survey looks at regulatory impacts to both cleared and uncleared derivative markets.

- The survey is split by market participant type – Dealer, FCM, CCP or Client.

- There are plenty of questions about the Leverage Ratio.

- And specific questions posed to FCMs about obstacles to their business and dealing with “small” clients.

- It is an important survey and deserves widespread industry response.

The Financial Stability Board

The Derivatives Assessment Team (“DAT” – cool name, makes it sound like a SWAT team….) is following up their 2014 work to assess the current incentives for central clearing. This is a joint operation from four international regulatory bodies – FSB, BCBS, CPMI and IOSCO. So pretty heavy-weight! It is also something very close to our heart at Clarus, with some of our most popular blogs looking at this subject:

- The Unintended Consequences of Uncleared Margin Rules

- NDF Clearing – What is Multilateral Netting?

- Margin Rules are Pushing Swaps to Clearing

We’ve also tried to assess the potential impact that Brexit and a European location policy could have on the economic incentives to clear:

The Questionnaire

We’d like to bring as many people’s attention as possible to the questionnaire, as more data is good data – we are looking forward to seeing the results in 2018. There are three different questionnaires, split by:

- Clearing Members (both House accounts and Client Clearing providers)

- CCPs

- Clients/End Users

Sadly no survey of Fintech Data Providers is included, so I don’t think Clarus will be responding to this particular survey.

The Previous Survey

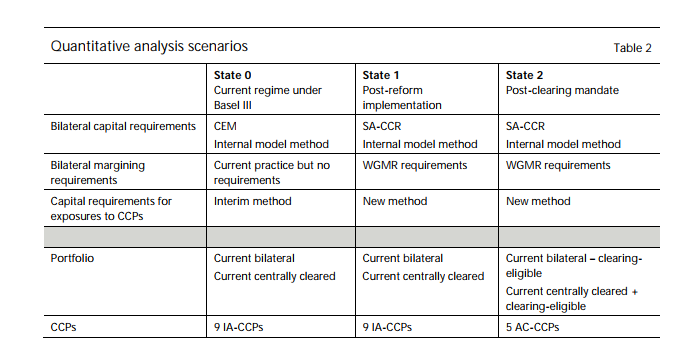

An assumption in the original survey from 2014, is interesting to note:

From that table, you can see that we are now in State 2 -post the clearing mandates, post Uncleared Margin Rules. Note the following:

- The idea was to track the economic drivers (IM plus capital) that would come into play as new capital regimes and new margining regimes entered into force.

- Some assumptions had to be made – for example, once uncleared margin rules are in force, clearing eligible trades are cleared. Everything else remains uncleared.

- Take a look at the number of CCPs! In State 2 (where we are now) the model used only 5, “Asset Class” specific CCPs. This was because it was impossible to forecast the split of business per asset class that would transact across two (or more) competing CCPs. The analysis did not want to lose the potential portfolio effects from clearing by needlessly bifurcating the forecasts.

Whilst I doubt anyone had this level of foresight, that assumption now looks particularly apt with the advent of CCP Basis. As a result of these pricing differentials, we are increasingly ending up in a situation where we DO have Asset Class-specific CCPs (allowing for differences between OTC and ETD market sectors).

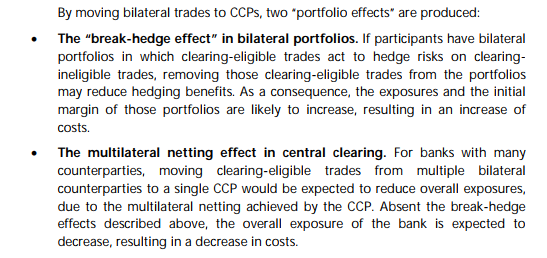

As the FSB quite rightly pointed out in 2014:

The market response to UMRs has tried to maximise the benefits of these “portfolio effects” across most products that are eligible for clearing. For example, NDF trading has seen clearing take-off, OIS has transformed to a 100% cleared market and Inflation swaps now see clearing as the market standard.

The Interesting Dealer Questions

As we said, the survey is split by participant type, so let’s look at the questions posed to the dealers first. Which are the most interesting?

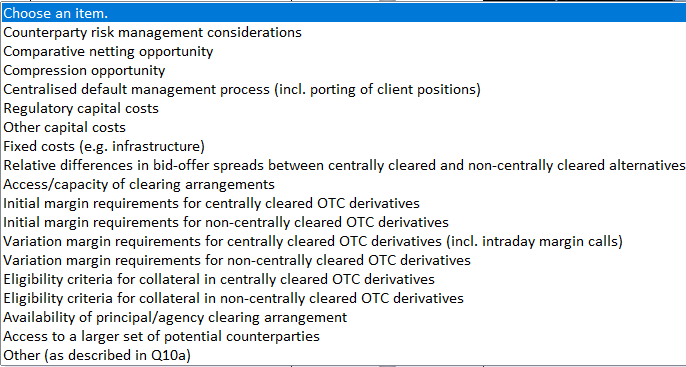

1. Incentives to Clear

![]()

This is really the crux of the survey. The choice of options is quite long – note that this is for “non-mandated” transactions, so don’t go looking for “Clearing Mandate”….

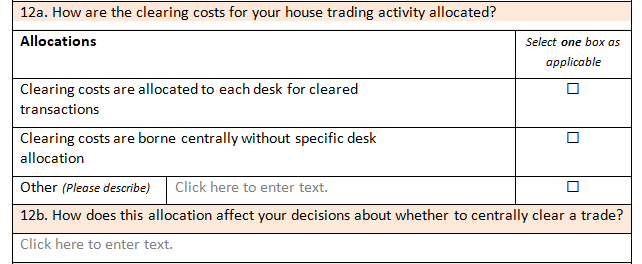

2. Allocation of Costs

2. Allocation of Costs

This is particularly interesting for us as we know of several different approaches across the industry. Some banks would even allocate these costs down to trader level…..We of course have some great solutions in CHARM for this conundrum (overall IM is sub-additive at CCPs).

This is particularly interesting for us as we know of several different approaches across the industry. Some banks would even allocate these costs down to trader level…..We of course have some great solutions in CHARM for this conundrum (overall IM is sub-additive at CCPs).

3. Cost of Clearing

![]() This is an interesting one. One of the great problems of introducing a Clearing Mandate is that CCPs could increase fees over and over again…..but also a tricky one to break-down because more counterparties are involved in more CCP services (e.g. Compression) than ever before. So your total bill may have increased from your CCP over the past 5 years, but you are getting a lot more for your money…..

This is an interesting one. One of the great problems of introducing a Clearing Mandate is that CCPs could increase fees over and over again…..but also a tricky one to break-down because more counterparties are involved in more CCP services (e.g. Compression) than ever before. So your total bill may have increased from your CCP over the past 5 years, but you are getting a lot more for your money…..

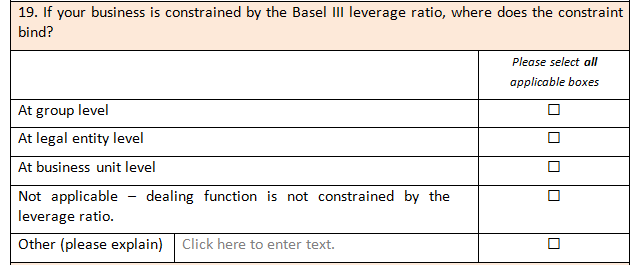

4. Leverage Ratio

I didn’t expect this one! Is anyone captured by the leverage ratio NOT constrained by it?

I didn’t expect this one! Is anyone captured by the leverage ratio NOT constrained by it?

5. Liquidity

There have been some very reasonable cracks at answering this question from a quantitative perspective – not least by the Bank of England, and latterly by ourselves. We’ve not talked about it much recently, so will be interesting to see the answers that come in.

There have been some very reasonable cracks at answering this question from a quantitative perspective – not least by the Bank of England, and latterly by ourselves. We’ve not talked about it much recently, so will be interesting to see the answers that come in.

The Interesting CCSP Questions

There is a different (and even more in-depth) questionnaire for the providers of Client Clearing Services (FCMs). Much of it is about the business mix (and some of the quantitative answers can be inferred from Tod’s blogs on FCM quarterly rankings).

1. Business Split

I have no idea what the industry average will be to that one….intrigued to find out!

2. Small Clients

Always intrigued what is classified as “small”….

Always intrigued what is classified as “small”….

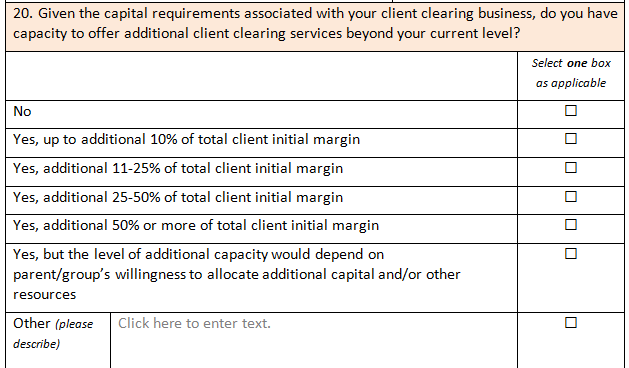

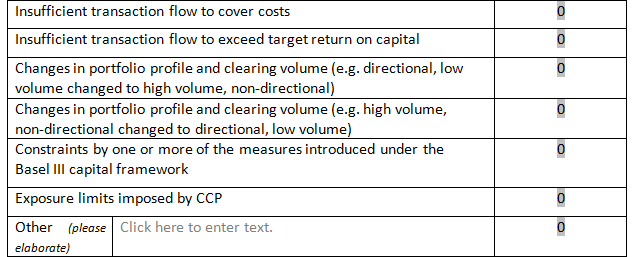

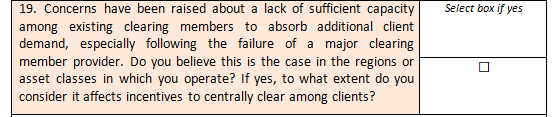

3. Capacity

This appears to be the crux of much of the survey – is your business capital constrained and therefore will not service more clients or smaller clients….

This appears to be the crux of much of the survey – is your business capital constrained and therefore will not service more clients or smaller clients….

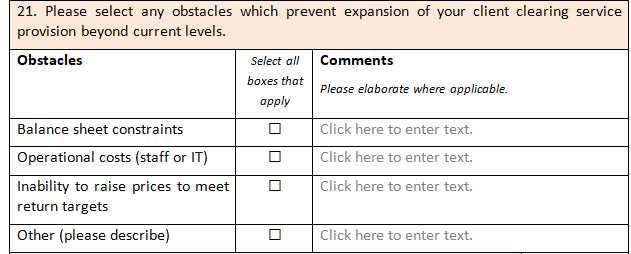

4. Obstacles

Will be interesting to see the “Other” reasons on this one….

Will be interesting to see the “Other” reasons on this one….

5. Reasons to Offboard (!)

I didn’t even realise off-boarding was frequent enough to warrant inclusion on a survey!

The CCP Questions

CCPs have been a beneficiary of G20 reforms. So I think we can expect positive responses from them. Much of the quantitative part of the survey can already be seen in CCPView – both via Volumes being cleared (split by House and Client) and via the CPMI-IOSCO Disclosures, which tell us how many clearing participants are registered at each CCP.

There are only two questions I would highlight:

1. Capacity

This could be a key question to answer for the industry as a whole….

This could be a key question to answer for the industry as a whole….

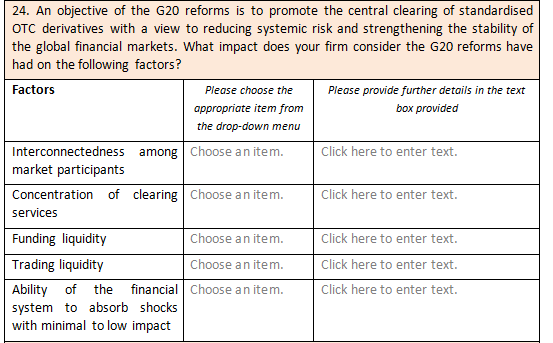

2. Reform Effects

I would add to “concentration of clearing services” or “trading liquidity” the effect that CCP basis has had on markets….

I would add to “concentration of clearing services” or “trading liquidity” the effect that CCP basis has had on markets….

The Client Questions

Finally, we get to the end users themselves. Clients are posed the highest number of questions (63 in total). We are just as interested in the Client’s responses to the above questions too, and there are three further interesting ones:

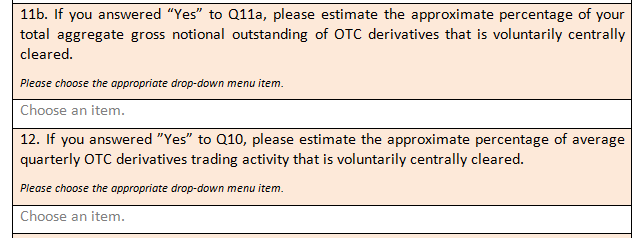

1. Volumes versus Notional Outstanding

This is a particularly opaque corner of the market and pertinent to our work at Clarus. Just what is the split on the client side of cleared vs uncleared activity?

This is a particularly opaque corner of the market and pertinent to our work at Clarus. Just what is the split on the client side of cleared vs uncleared activity?

2. Location Policy

Is this a hint at the European location policy? It’s a bit subtle if so. I think they should have included an outright Brexit question!

Is this a hint at the European location policy? It’s a bit subtle if so. I think they should have included an outright Brexit question!

3. Repo

This must be a key question nowadays with so many “cash only” CSAs floating around.

This must be a key question nowadays with so many “cash only” CSAs floating around.

In Summary

- The FSB survey is very thorough and will supply plenty of interesting data.

- Dealers will likely focus on the negatives – increased costs of doing business via Initial Margin, and increased capital requirements.

- Client Clearing Service providers (FCMs) may also focus on negatives – the obstacles to doing more business, the capital requirements.

- It will be interesting to see which side of the fence the Client surveys fall on.