Following on from my article FRTB – The Default Risk Charge, I wanted to look at another specific component of the Standard Approach, namely the Residual Risk Add-On for instruments with non-linear payoffs.

Background

In January 2016, the Basel Committee on Banking Supervision (BCBS) published its Standards for Minimum Capital Requirements for Market Risk; also known as the Fundamental Review of the Trading Book (FRTB). These new standards replace parts of the Basel 2.5 reforms, which were introduced in 2009 to address the material undercapitalisation of trading book exposures during the 2007-08 financial crisis. (Document is here).

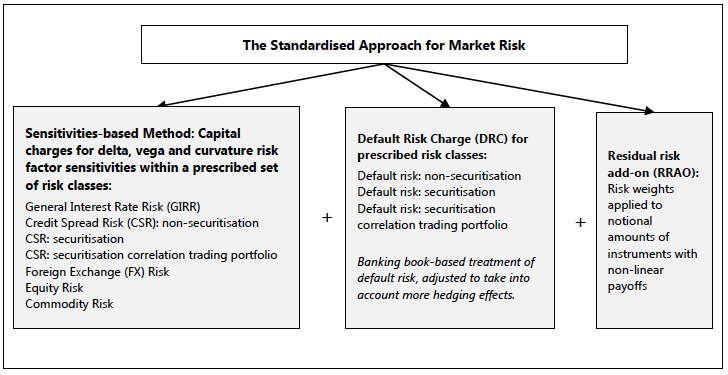

Standardised Approach (SA)

The overview chart from the BCBS document:

In Chris’s article, FRTB – Excel Calculator for the Standardised Approach, he looked at the details of the Sensitivities-based Method as applied to Interest Rate Swaps and in my earlier article I covered the FRTB – The Default Risk Charge, so lets turn to the third category in the diagram above.

Residual Risk Add-On

The first point to note is that the products subject to the Residual Risk Add-on charge are also included in the Sensitivities-based Method (Delta, Vega, Curvature) and where appropriate the Default Risk Charge, so this is an additional charge to those.

Secondly it is a simple sum of gross notionals of instruments bearing residual risks, so a crude measure.

One that is somewhat mitigated by the fact that risk weights are 1% for instruments with an exotic underlying and 0.1% for other instruments bearing residual risks.

And from the BCBS doc:

![]()

So there you have it, longevity risk as traded in insurance-type derivatives and weather derivatives, I don’t know much about those markets beyond the fact that they are highly specialised and likely to be small and of interest to few firms.

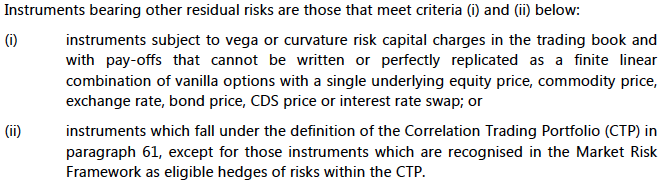

However it is the other instruments bearing residual risks that are more relevant and much more significant.

Let’s see what the BCBS document says about these.

In addition back-to-back transactions, listed and eligible for clearing instruments are excluded.

BCBS then provides the following:

This is where it gets interesting as FX Barrier Options are commonly traded, CMS Spreads and Range Accruals are well known in Rates, Basket Options in Equities, Spread Options in Commodities, Tranche Index in Credit, to name just a few, I could go on …

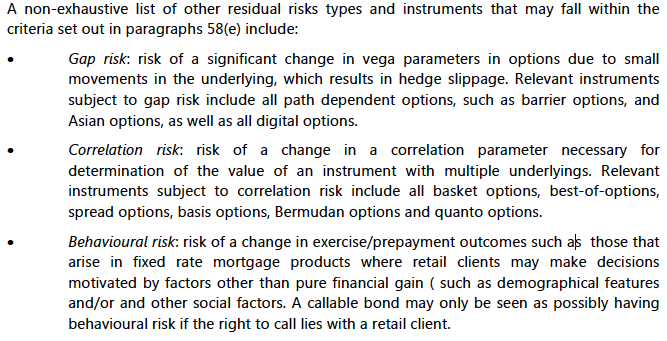

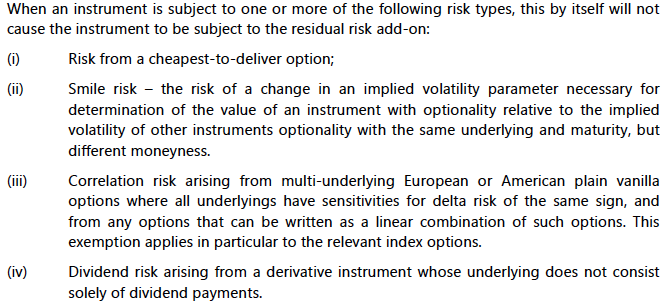

Before we delve further into some of these, BCBS also adds:

Which is helpful as Bond Options and Bond Futures would be excluded by the first, any Non-ATM Options by the second, Index Options by the third and Equity Options by the fourth.

Lets look at a few of the products that fall into the “instruments bearing residual risk” category.

FX Barrier Options

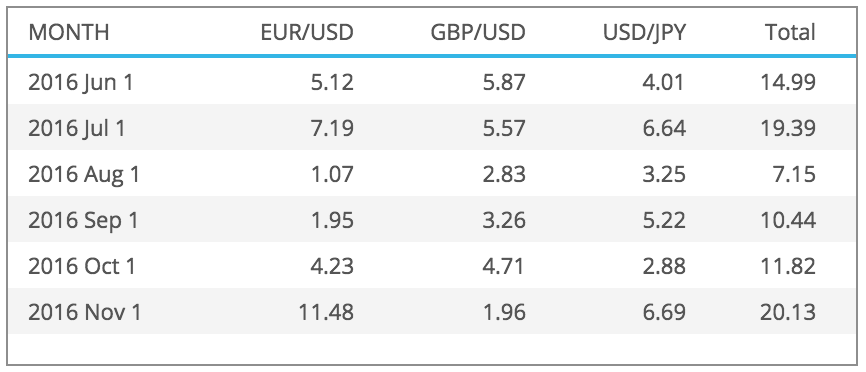

Using SDRView we can look at the volume of reported trades by US persons.

Barrier Option volumes in USD Billions by month for three major currency pairs.

Showing:

- EUR/USD average monthly volume is $5.2 billion

- GBP/USD average monthly volume is $4.0 billion

- USD/JPY average monthly volume is $4.8 billion

- A total average monthly volume of $14 billion

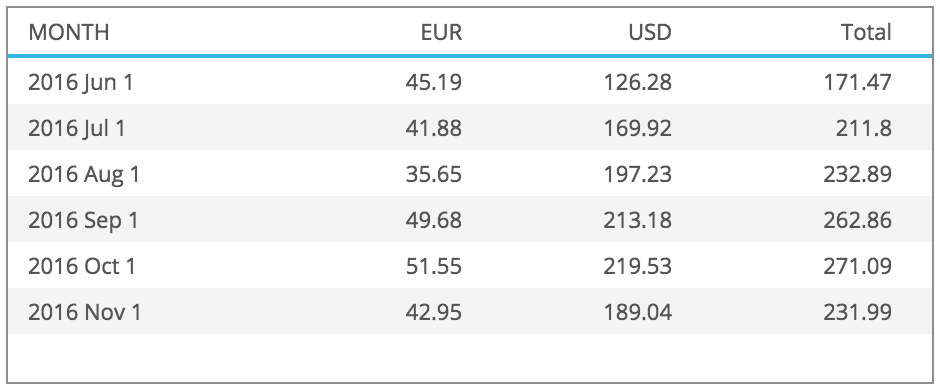

Compared to Vanilla Options, this is a small percentage, as the below shows.

However Vanilla Options are subject to just the Sensitivities based charge, while Barrier Options are subject to both the Sensitivities based charge and the Residual Add-On Charge. Importantly this charge is a direct function of the gross notional.

Lets try a simple example to quantify this.

First assume we turn over outstanding notional every 6 months, so outstanding gross notional is 6 times the monthly volume. Second assume we are a major dealer with 10% market share in the above currency pairs.

In which case our gross notional is $14 billion * 6 * 10%, equals $8.4 billion.

Making the Residual Risk AddOn at 0.1% equal to $8.4 million.

It is not easy to know how significant this is compared to the Sensitivity based charges without constructing hypothetical barrier option portfolios and working through the calculations, but that is a much bigger task for a different day.

Suffice to say the Residual Risk AddOn will be material for a dealer with a large FX Options book.

IR Exotics

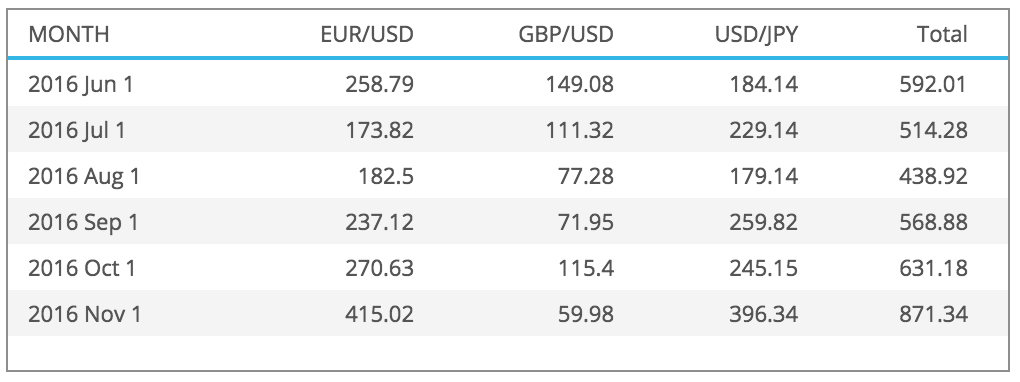

Next lets look at Interest Rates with product type “Exotic” in the public dissemination record and while it is hard to know whether these are all truly exotic in the sense of requiring a residual risk addon, lets assume for today that they are.

Monthly volumes in USD billions for the last six months for USD and EUR trades.

Showing:

- EUR monthly average volume of $45 billion

- USD monthly average volume of $185 billion

- Total monthly average volume of $230 billion

So much larger gross notionals than FX Barrier, as we would expect for an Interest Rate product.

Lets do the same example as before, outstanding notional is 6 times monthly volume and 10% market share.

Meaning our gross notional is $230 billion * 6 * 10%, equals $138 billion.

Making the Residual Risk AddOn at 0.1% equal to $138 million.

Which definitely is a much more significant number.

We can only hope that many of these Exotics would not meet the criteria of “instruments bearing residual risk”.

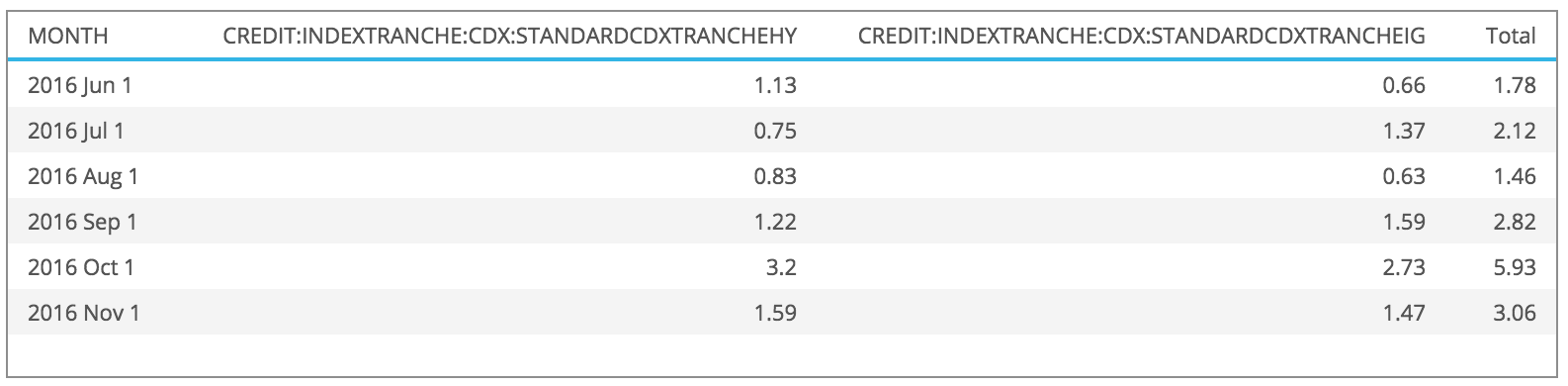

Credit Tranche Index

Finally lets look at a Credit correlation product.

Monthly volumes in USD billions for the last six months for USD Tranche on CDX IG and HY.

Showing a monthly average of $2.8 billion.

And using the same 6 months and 10% and 0.1% above, we get a Residual Risk AddOn of $1.7 million.

The smallest of our three examples.

Final Thoughts

Now you may think that that such instruments are only held by sophisticated dealers.

And these dealers will all get Internal Model Approval (IMA).

So the above discussion is moot.

However there are a number of reasons why it is not.

First there is an open point on whether the Standard Approach (SA) should serve as a floor.

With IMA being floored at something like 60% to 80% of the SA.

If that proposal makes it (and the jury is out) the Residual Risk AddOn is certainly important.

Secondly the use of IMA is approved at a Trading Desk level and SA needs to be run daily.

As a regulator may require a firm to revert to the SA (e.g. on breach of PL attribution).

Thirdly a firm may not seek IMA for a small separate Exotics desk.

Summary

Any measure based on gross notional of derivatives is likely to be a big number.

The Residual Risk Add-On has the potential to be very significant.

As such the impact on Trading Books needs to be carefully evaluated.