- EUR Rates markets are hitting volume records.

- This is elevating EUR to be the largest swaps market in the world during 2024.

- SEF volumes are also benefitting from this increase in activity.

- We explore signs of balance sheet dressing in EUR swaps that suggest Open Interest in swaps may drop into year-end again.

Time for another installment of my “What’s New” series, looking at dynamics (mainly volumes!) in different currencies. I follow EUR markets pretty closely, particularly through the lens of €STR futures market share and what is happening with EUR swaps. Today, I’ll take a look at most aspects of EUR trading.

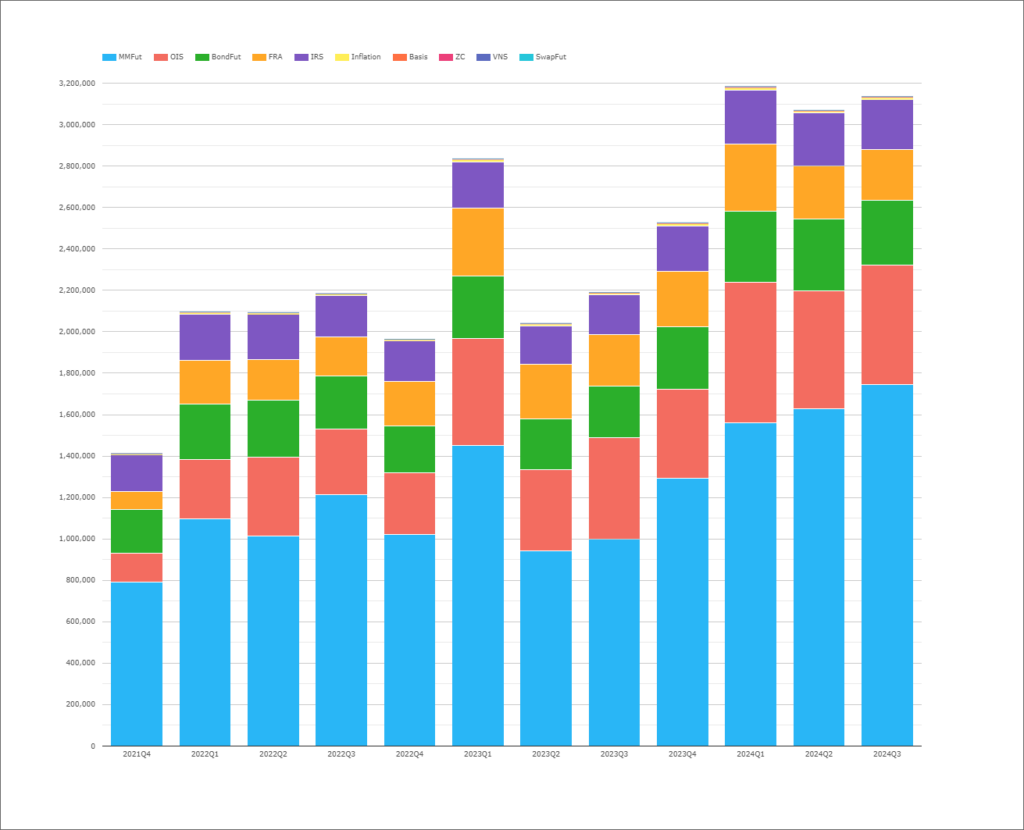

EUR Outright Volumes

I like to start a blog with a catchy chart. Below is therefore one of the most important take-aways – EUR volumes are at all time highs.

Showing;

- Average Daily Volumes per quarter in notional equivalents across all EUR rates products – covering swaps, bond futures, STIRs etc.

- One day I will write a blog that isn’t about all time record volumes. That day is not today though!

- The chart shows that 2024 has been a record year, with the top three all time record volumes coming in the past three quarters.

- As I said in my USD commentary, despite choosing to write this blog, I really was not expecting record volumes. I thought that the German economy was struggling and that the ECB rate moves had been well communicated. The extreme August volatility seemed a USD-centric move at the time.

- However, there has been a huge amount of trading in Rates this year, irrespective of currency. This bodes well for most CCPs.

- I’ve checked back to 2017 and this chart looks even more impressive on a long time horizon. Volumes in EUR products really are flying.

- We should remember this if volumes decrease into Q4. Traded volumes have been really healthy this year.

Let’s check in on DV01 as well. We can see above that volumes in STIRs have grown – is all this trading short-end? Has the actual amount of risk traded also broken records?

Yes, DV01 has been hitting records as well! The chart shows;

- Monthly volumes of DV01 traded across all EUR Rates products.

- (Honestly, the quarterly chart looked too similar to the first chart of volumes to warrant posting it again. The switch to monthly volumes is solely to switch things up a bit here!)

- September 2024 saw a huge amount of risk trade in EUR, with both OTC and ETD products close to their records.

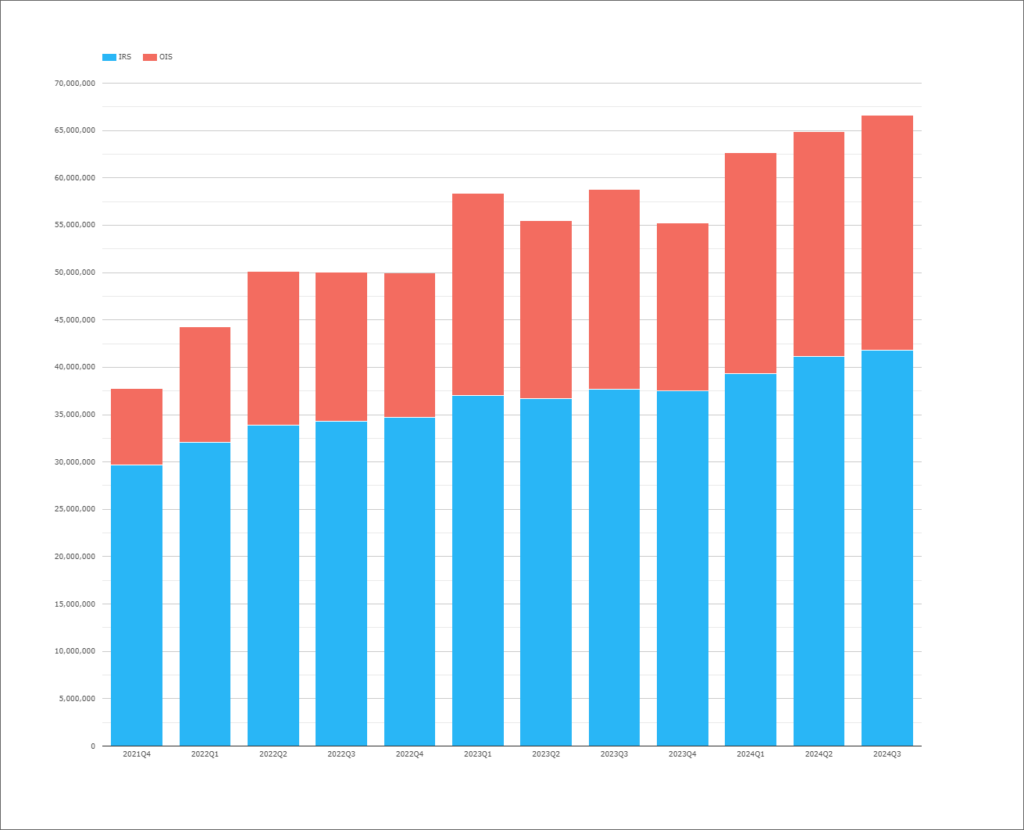

And the prize for the biggest market goes to…?

Painting EUR in the best possible light, it has been the largest Swaps market in the World for the past year!

Showing;

- DV01 traded each quarter in OTC products (swaps & FRAs mainly) calculated in $m equivalents.

- EUR and USD are much larger swaps markets than the next three largest – GBP, JPY and AUD.

- How much larger? Each of the EUR and USD markets are about 4 times bigger than GBP, 5 times larger than JPY and 10 times as large as AUD!

In case anyone needs reminding (again!), USD futures markets are still the largest in the world. This means that USD is easily the largest “Rates” market when you look across everything – especially so when also adding government bonds into the mix.

It would be a really interesting exercise to consider what the true liquidity in EUR markets is at the moment. We have a multiple rates environment across €STR and EURIBOR. Is basis trading truly additive liquidity when I have a unit of risk to hedge? We also have €STR futures, which are potentially traded on a spread to underlying EURIBOR contracts.

Open Interest

These “spread” considerations motivated me to look into Open Interest for both Swaps and Futures. Can we directly see the portion of EUR markets that trade as spreads between EURIBOR and €STR contracts?

First up – swaps. Basis Swaps in EUR are traded as two swaps, therefore they directly impact the Open Interest in both IRS and OIS. Is there any evidence that there is a lot of basis trading happening?

- Open Interest (along with Initial Margin) is a pretty decent measure of the risk that has built up at a CCP.

- 37% of Open Interest (risk) is now in €STR products, compared to 22% back in 2021. That is roughly consistent with the traded volumes we see in the RFR Adoption Indicator.

- €STR Open Interest tends to see large jumps in Q1 of each year compared to the prior quarter.

- Is this related to compression and associated balance sheet window dressing for GSIB purposes? Is it a sign that risk/gross notional is pretty stable in EURIBOR products and that it is being actively managed back into €STR? It is really hard to say.

- Thinking aloud, it could also signal that basis trades are taken off into year-end, to be reinitiated at the start of the year.

It isn’t any easier to interpret Open Interest for Futures markets. Looking at the overall EUR STIR picture:

We see that Open Interest at ICE has grown more than at Eurex:

- Since Q1, ICE OI has increased by 550,000 contracts.

- OI at Eurex has increased by 300,000.

This seems healthy, but doesn’t help us work out what is traded “on spread”.

I think the best summary of liquidity is the analysis published by BMLL. Their data shows that liquidity is improving in €STR contracts, indicated by a tightening in the bid/offer, particularly at ICE:

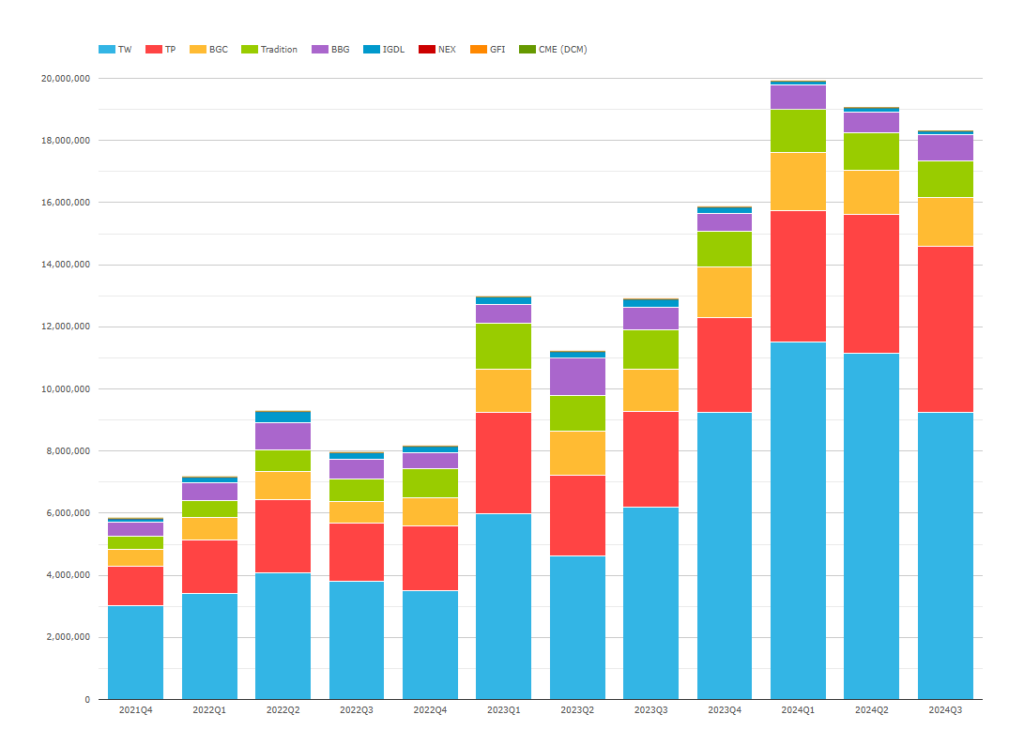

SEF Trading

SEF volumes, if we exclude FRAs, have also hit records in 2024:

It is interesting to see that Tradeweb volumes have fallen each quarter (after a really stellar Q1), but remain in line with Q4 volumes from last year. Tulletts (TP) have had a really good year in EUR!

In Summary

- 2024 has seen three record quarters of trading activity in EUR Rates markets.

- This is replicated across both risk traded in DV01 terms and notional activity.

- EUR is now the the largest swaps market in the world.

- Open Interest in EUR swaps might drop again into year-end, as we have seen in the past couple of years.