Guest Blog Series

Wow, the ECB meeting this week is an important one. It’s not immediately apparent, but when you look into the details of recent monetary policy announcements, this looks like the last chance the ECB has to cut rates until early 2015.

Why? It all has to do with the structure of the new liquidity-providing operations – TLTROs.

These are to be offered as fixed rate cash at the prevailing September MRO rate, currently 15bp (plus a 10bp spread).

Banks will be able to hold onto these funds, no strings attached, until at least 2016 – and will have the option to renew the funds into 2018 if they have met certain new lending criteria in the interim period. The first operation is scheduled for allotment on September 18th. Given the current european economic malaise, the ECB must be looking for front-loaded allotments to get the extra liquidity to work ASAP.

At 25bp, these funds are undoubtedly cheap – but they are still at a fixed rate.

Therefore, the ECB cannot credibly cut rates between the first and second operation on December 11th without (unfairly) penalising those banks taking the initial batch of funds in September. I would go as far as to say that the ECB risks making the first TLTRO auction redundant if they were to signal an upcoming rate move. Quite simply, if they want to change the level of rates at all (let’s say within the next four-to-five months), they have to do it on Thursday.

This past week has seen Eonia fix negative for the first time in history – yes, banks will literally pay each other to take cash off their hands, with no strings attached (uncollateralised).

And just as September has started, we have seen the ECB meeting dates for the remainder of the year trade in negative territory. This is best seen in SDRView Pro, where we can clearly see that October ECB first traded last week at +0.5bp and has since moved lower to last trade at -1.3bp yesterday (1st Sep). To be fair, we have already seen the Eonia Maintenance Periods softening, with August currently looking like settling at flat to minus a quarter of a bp.

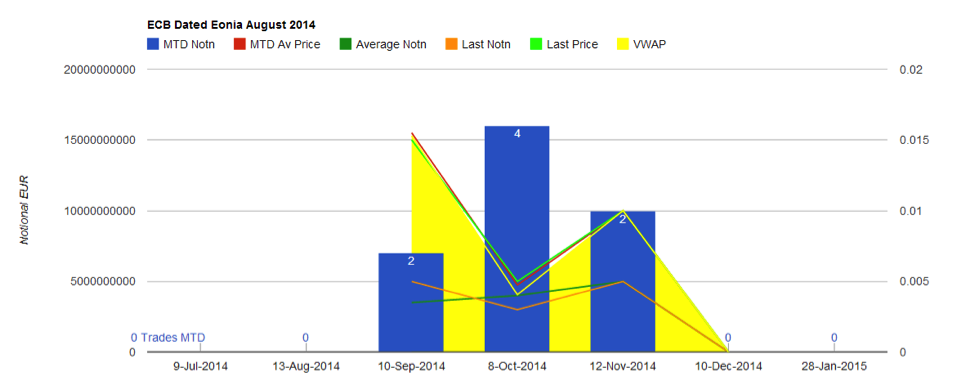

Leveraging the SDRView API, we can see ahead of Thursday’s meeting exactly what the markets are doing. For example, in the last week of August, we saw little trading in ECB dates:

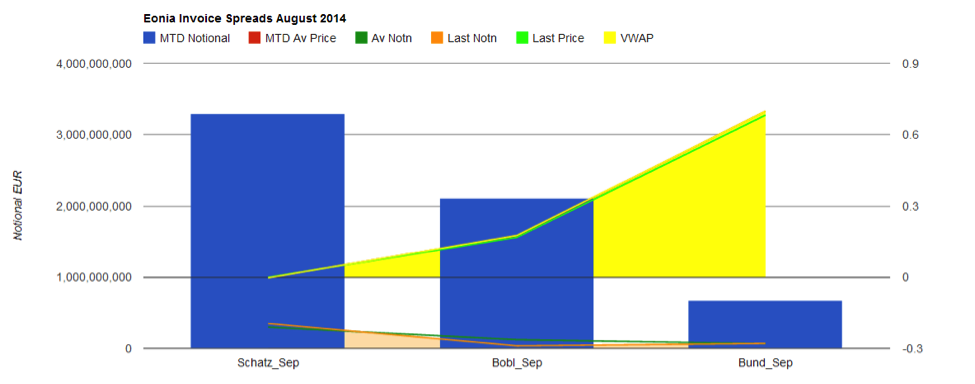

I think we can all agree that 8 trades in the week that saw Eonia print at a negative number for the first time is a pretty paltry return! We saw much more activity in Eonia invoice spreads, but rates were on the way back up:

Therefore, judging from the paltry activity in Eonia markets, it looks like the market as a whole is not expecting Draghi to move on Thursday.

How’s about FRA markets – does the Empire Strike Back?

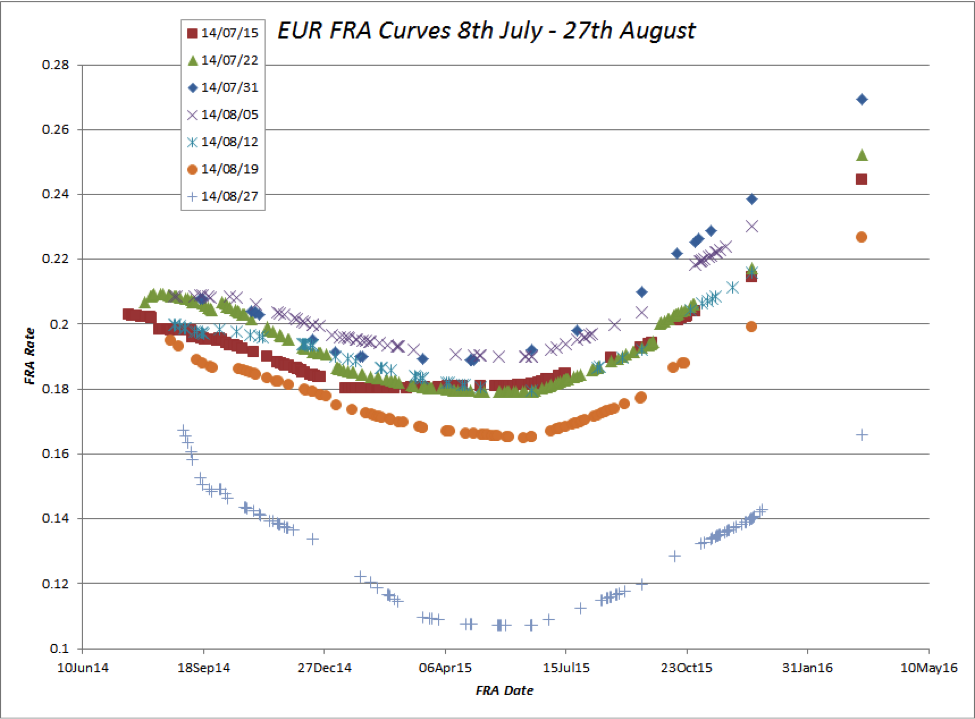

Using SEFView, we’ve certainly seen a huge move lower in price since our last piece in July:

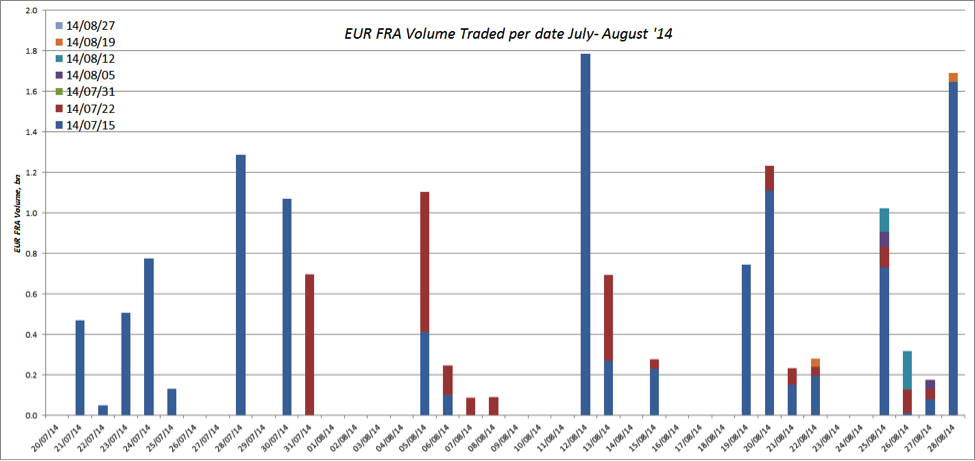

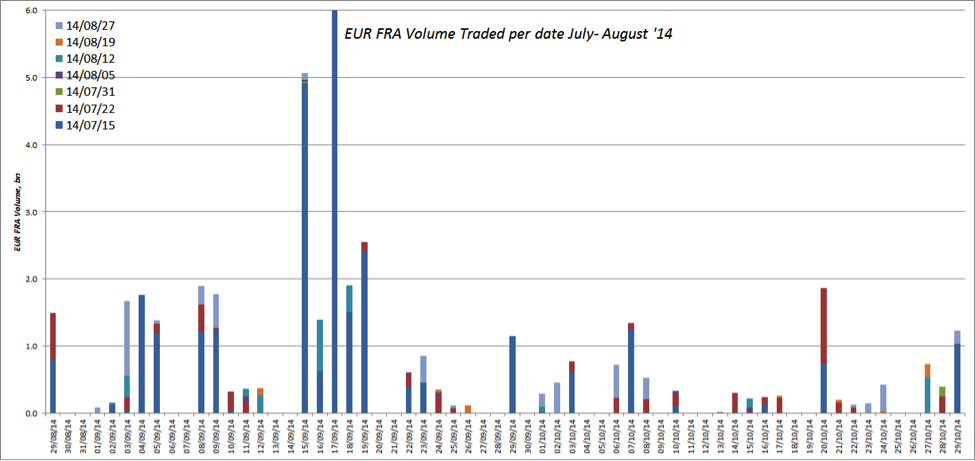

Markets currently see the base in Euribors at roughly 10.5bp – but as we acknowledged previously the force is weak with the European FRA market. Yet again, the VWAP for FRAs has been consistently above the realised fixings during July and August. Volumes were generally dispersed, with the day after the August ECB the largest volume at €1.8bn:

But if we look from this point forwards, the FRA volumes being traded are centred around one week in September. As expected, the IMM date still dominates, but the volumes are also centred around the timing of different announcements regarding the first TLTRO:

The graph shows that there has been a total of €13.7bn traded for the SEP IMM during our observation period. The other significant dates by volume all relate to TLTRO announcements:

- 15th Sep (fixing 11th): €5bn. Central banks inform banks about their borrowing limits.

- 18th and 19th Sep (fixing 16th & 17th): €4.45bn. Announcement and deadline for bids in the TLTRO.

From this market activity, it looks like banks expect 100% allotment at the TLTRO, hence hedging the announcement dates. Given the relatively small sizes, it could also be some short-term hedging tied to Greek banks who fully expect to take up their funds. Either way, the activity paints a picture that is not apparent in the price data. Additionally, there is no discontinuity priced-in for Thursday’s meeting.

The analysis of the market activity therefore suggests it would be a shock to the market if the ECB did actually cut rates on Thursday.

Markets are looking for the TLTRO allotments to be the market-moving event of the month and for Draghi to hold fast on rates. This therefore all points towards ABS purchases and, ultimately, full-blown QE becoming the ECB’s weapons of choice – moving the price action away from the short-end and into lower-for-longer trades.

At which point banks would be well versed to take all the TLTROs funds they can get their hands on and load up on carry trades….