- Is “enshittification” of social media akin to worsening liquidity conditions in financial markets as a result of increased rent-seeking behaviour of centralised platforms?

- We see ever increasing volumes traded in Rates markets, and yet constant concerns from market participants over liquidity conditions.

- Post-trade transparency shines a light on market functioning, but does not define liquidity metrics or the cost of liquidity provision.

- Does this all make Citadel the Taylor Swift of modern markets?

*Disclaimer – this is a tongue-in-cheek consideration of third-order risks in our markets. Hope you enjoy.

For those who missed it, the FT introduced us to “enshittification” last week, and the article has no doubt made the rounds of trading floors ever since:

https://www.ft.com/content/6fb1602d-a08b-4a8c-bac0-047b7d64aba5

Why are we choosing to talk about it on the Clarus blog? Because the Wikipedia entry defines it as:

Enshittification is the pattern of decreasing quality of online platforms that act as two-sided markets. Examples of enshittification include services and products provided by Big Tech companies like Amazon, Bandcamp, Facebook, Google, Reddit, Twitter, and Unity.

https://en.wikipedia.org/wiki/Enshittification

It is the “two-sided” markets aspect that jumped out at me – sounds a lot like trading to me! With more and more focus on market structure and the platforms that are integral to derivatives markets, could enshittification (or something similar) ever happen in financial markets?

Regulation

The FT article cites four forces that act to reduce enshittification (Competition, Regulation, Self-Help and Workers). Our financial industry is awash with regulations. Does regulation in derivatives markets prevent or enshrine enshittification? Regulations have generally moved execution and post-trade onto centralised platforms, such as SEFs and CCPs. Trade reporting and transparency are also largely dependent on standardised platforms.

Is something akin to enshittification the true cost of more transparency/electronification/centralisation in our markets? I hope not, but we should assess the risk…..

What is enshittification?

I understand enshittification to broadly describe a process whereby;

- Something is centralised, creating positive network effects and bringing together users.

- This leads users to have a “great experience” on the platform, and motivates further network growth.

- The quality of the product continues to improve (more users, more user interaction).

- This great quality product then allows the platform to start offering further services to third parties – such as selling advertising space, promoting content, selling data.

- This continues until the platform shifts focus from improving the user experience to maximising the money earned from third parties.

- At which point the user experience declines, as users are bombarded with promoted material at the expense of the original reason they signed up to the platform.

- It seems like enshittification could also be replaced by “rent-seeking behaviours” in a lot of cases.

Our readers will be more than able to point at centralised services in derivatives markets (price discovery, data terminals, clearing, execution platforms etc) that could fit into a number of those stages.

What could this look like in derivatives markets?

We are all, ultimately, in the game of risk management. So what are the risks in our markets of enshittification and could it happen?

- I believe that market participants are ultimately concerned with one thing – liquidity i.e. how easy is it to hedge my risks?

- The regulatory changes over the last decade introduced a lot of centralisation – from SEFs/MTFs to trade reporting and clearing.

- These changes were expected to lead to new market participants entering the swaps market to provide new sources of liquidity – a good thing.

- This did indeed happen – but it has only really been Citadel who have entered the market-making realm.

- We have also seen hundreds (thousands?) of new users of clearing as a result of clearing mandates.

- So we have seen more use of centralised platforms than ever before.

- We also saw an initial improvement in liquidity provision from new market participants. Great!

- But the roll-out of Clearing Mandates is now complete. Does this introduce a risk that platform operators start to turn to rent-seeking behaviours in order to achieve revenue growth?

- Potential signals of this behaviour would include platform operators increasing their focus on new services – selling data for example.

Is The Only Answer More Regulation?

A simple answer to stop rent-seeking behaviour is to “regulate it out of markets”, particularly because the cost of switching any of these centralised services is extremely high for end-users. This is a potential avenue in financial markets, but the platforms still have to be commercially attractive to encourage continued investment.

A more likely outcome (and a true capitalists view), is that pure market forces come into play. Just as a music streaming platform cannot exist without access to Taylor Swift’s music, you can’t run a USD swaps platform without access to Citadel’s liquidity. Should Swiftie and Citadel really be paying the most in fees to these platforms?

Disenshittification

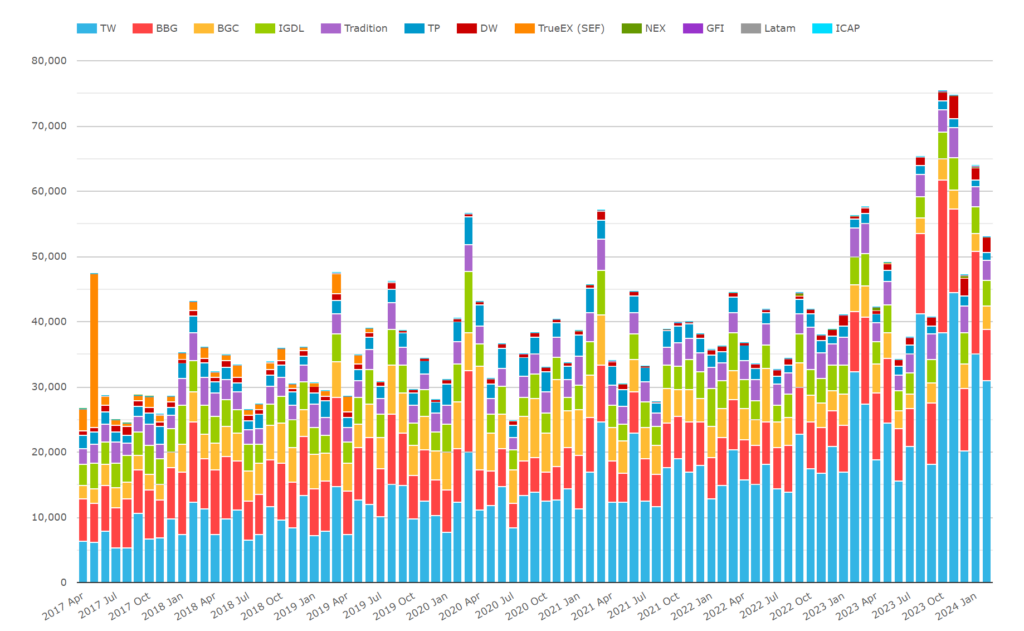

An example of enshittification in OTC markets can be seen in some recent data. SEFs reported an ADV of $50bn in January 2024 for USD Swaps with tenors of 10Y and longer. This is 225% larger than the same period in 2017, and doubtless carries more revenue for SEFs with it. And yet does anyone in the swaps market believe that liquidity provision has improved by 200% in the past 5 years? Market participants normally state the exact opposite!

If more market participants are trading more swaps than ever before, but available liquidity at any point in time has been stationary for years, is this evidence that enshittification may well be happening in our markets?

Market infrastructure has become more entrenched (largely as a result of regulation) and the platform operators are motivated by one thing – increasing trade volumes.

Is it time to move their goal-posts? Increasing liquidity provision could be the move toward “disenshittification” that our industry needs.

In Summary

- I take a sideways look at our current market infrastructure.

- Enshittification of social media could well be akin to worsening liquidity conditions in financial markets.

- Increased rent-seeking behaviour from platform operators is a risk in capital markets.

- It should be filed by all regulators as a “known-unknown” in the vast universe of risks they have to monitor.

- It remains inconclusive whether Citadel really are the Taylor Swift of swaps markets….