- CNY Swaps are now the largest interest rate swap market outside of the “G6” currencies.

- Clearing is split between Shanghai Clearing (onshore) and LCH SwapClear (offshore).

- 90% of the offshore market has been cleared so far in 2025, likely influenced by upcoming Uncleared Margin Rules.

- SEF trading has increased dramatically in the past three years, with Tradeweb ADVs (Average Daily Volumes) approaching $4bn.

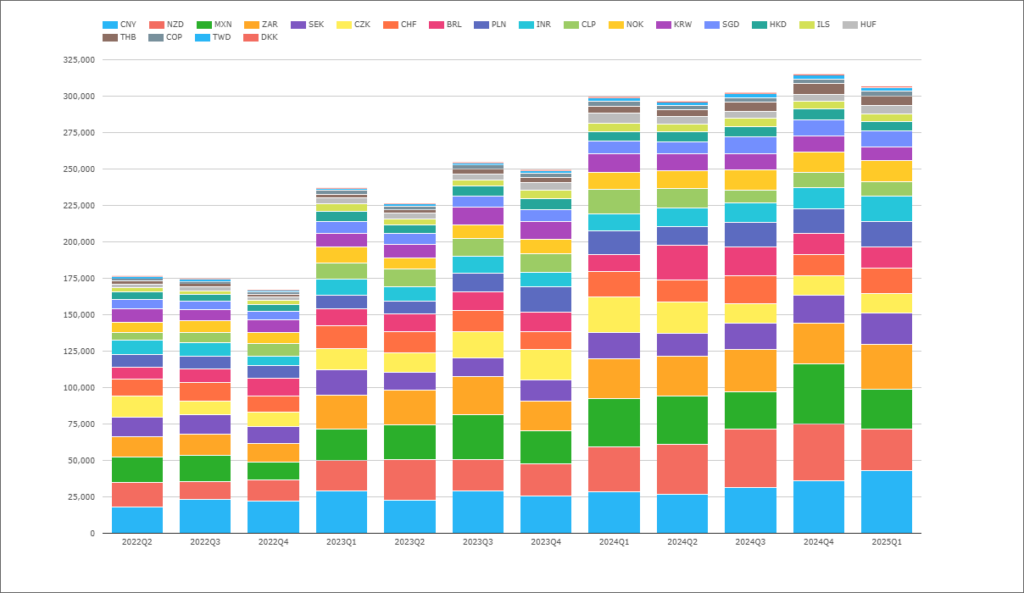

When I last wrote about CNY Swaps back in 2020, I found that CNY swaps were the 9th most traded currency in cleared Interest Rate Derivatives. They have since increased in size significantly, and are now the 7th largest swaps market.

Updating the data from CCPView;

Showing;

- Average Daily Volumes (ADVs in $m) in Cleared Interest Rate Derivatives from CCPView.

- The chart excludes the top six currencies by volumes (USD, EUR, GBP, JPY, AUD and CAD). These six currencies represented over ~95% of total cleared volumes (see Four Trends in Swaps Data).

- For the volumes displayed on the chart (not total cleared volumes), CNY represents 12% of ADVs, capturing the title as the 7th most traded swaps market.

- NZD and MXN now account for 10% of the volumes shown (again, outside of the top six).

- Comparing to our analysis back in 2020, SEK and CHF have now slipped to just 6% of volumes.

- A lot changes in five years in swaps trading!

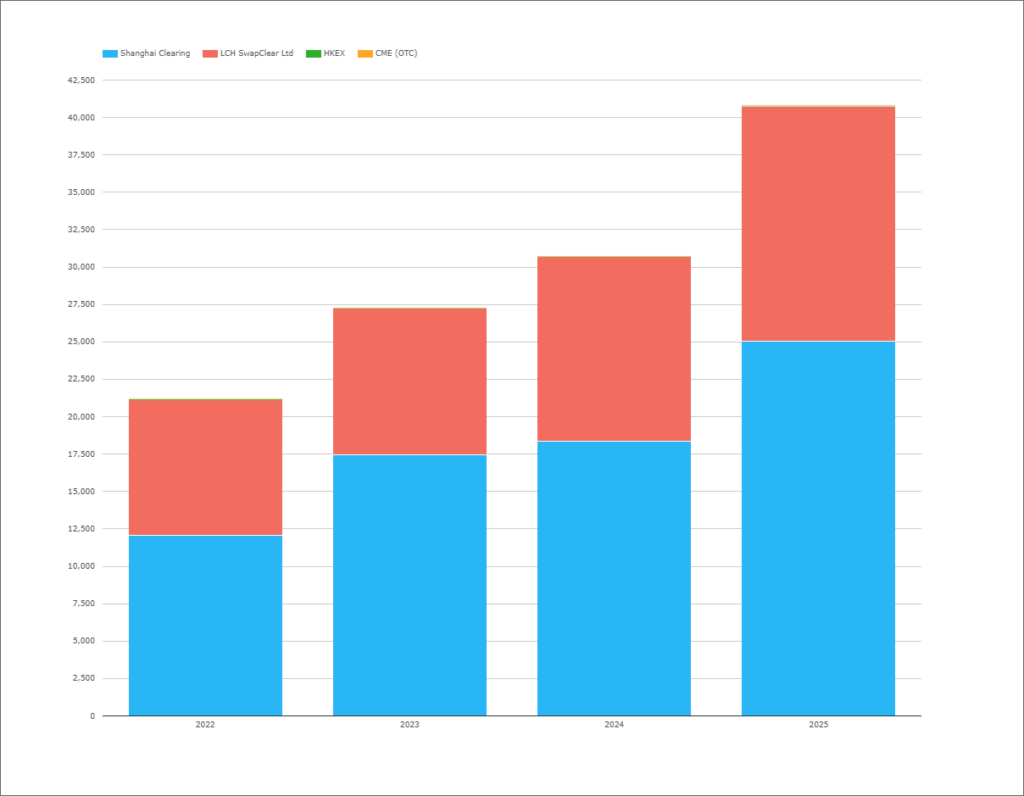

CCP Market Share

CNY is one of the seven currencies that I monitor in terms of shifting market shares at different CCPs. These seven currencies (AUD, BRL, CNY, EUR, INR, JPY and MXN) see at least 5% of volumes trade away from the “major” CCP and therefore present particular market dynamics.

Refreshing the market share of CNY swaps between Shanghai Clearing (onshore) and LCH SwapClear (offshore) shows a remarkably resilient 60/40 share:

Showing;

- Shangahi Clearing enjoy a 60% market share in CNY Swap Clearing.

- That has varied between 57-64% in the past three years, which is pretty stable when you consider that ADVs have nearly doubled in that time!

- Recall that LCH offer Non Deliverable CNY Swaps, with Shanghai Clearing representing the onshore, deliverable market.

- ADVs have really grown in 2025, surpassing $40bn per day. February 2025 saw all time volume records across the market (what is it with all time records and the timing of my blog writing?!).

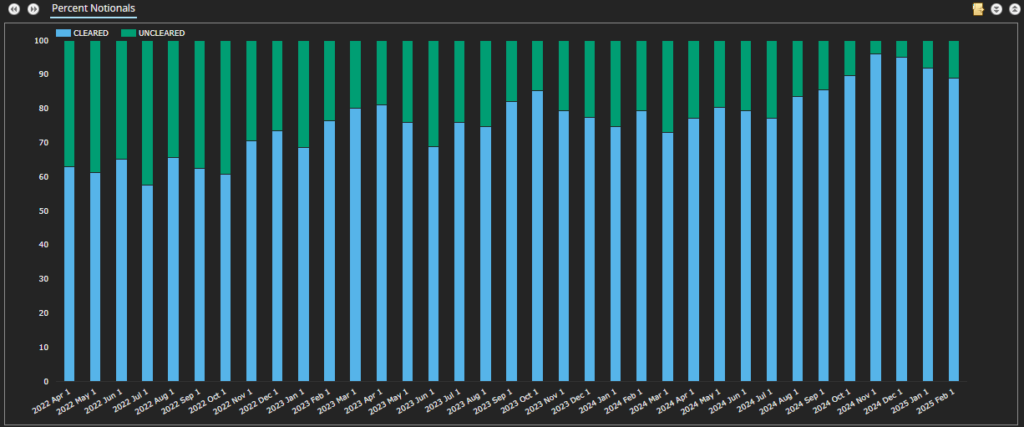

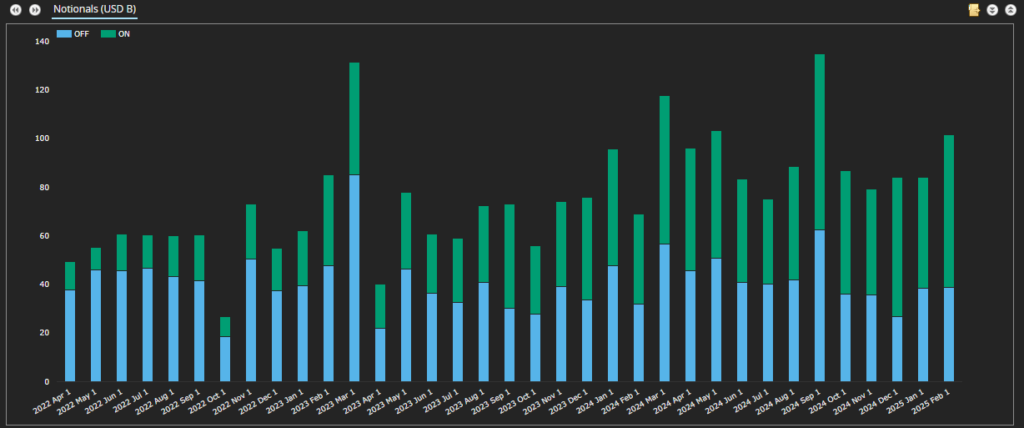

Most Offshore CNY Swaps are Cleared

In a big change from our previous blog, the take-up of CNY clearing has increased from ~60% to 90% in 2025:

Showing;

- 2022: 65% of the market was cleared..

- 2023: 77%….

- 2024: 82%….

- and now 90% of the market has been cleared so far in 2025!

Given the large increase in ADVs we have seen at both SwapClear and Shanghai Clearing, it is likely that this behaviour is repeated for both Onshore and Offshore markets.

New Bilateral Margin Rules Coming in 2026

I admit that it wasn’t 100% of a surprise to see record volumes in clearing. At the beginning of this year, I learned that Uncleared Margin Rules would be rolled out for Chinese market participants:

Summarising;

- September 2026: Variation margin must be posted against uncleared derivatives.

- September 2027: Initial margin must be posted for uncleared derivatives by the largest market participants.

- September 2028-September 2029: Phasing-in of Initial Margin rules depending on size of portfolio.

The Risk article makes some really interesting points, including whether ISDA SIMM will gain regulatory approval.

As readers well know, I always like it when regulatory change shows up in the data. It is great to witness such a large increase in the percentage of the market being cleared ahead of a planned implementation of uncleared margin rules for the local market.

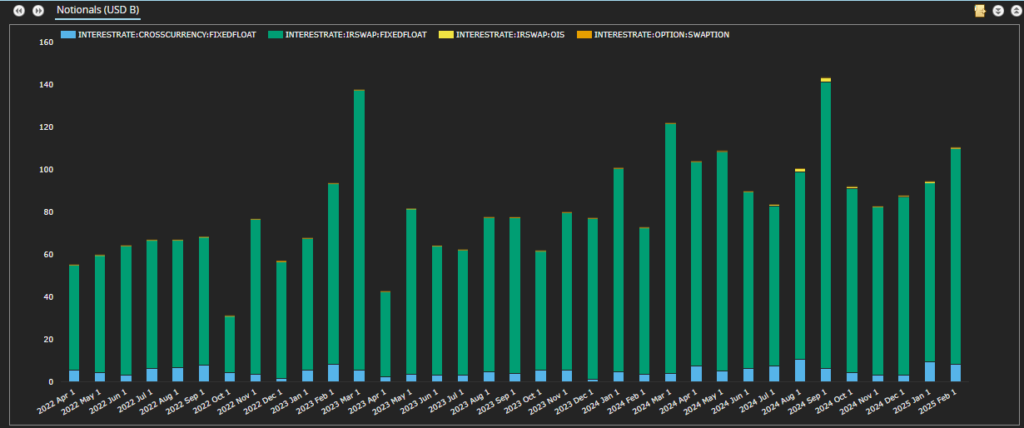

Product Types

I have tended to overlook an analysis of the types of product that trade in this “What’s New” series (8 blogs in 2024). My previous blog uncovered the fact that there used to be a CNY OIS market, but it virtually died out. That is still largely true, with OIS being only as large as Swaptions – which basically means very small:

The only product that can hold a candle to the volumes traded in Fixed-Float IRS in CNY markets are Fixed-Float Cross Currency Swaps. 93% of derivatives volumes in the past three years have been in Fixed-Float IRS, with most of the remaining 7% in Fixed-Float Cross Currency swaps.

Given that CNY trades against a term index – the market standard is a 7-day repo fixing that compounds and pays quarterly – I thought we might see a FRA market, but no such luck. I guess a 7D fixing is too short to warrant an active market?

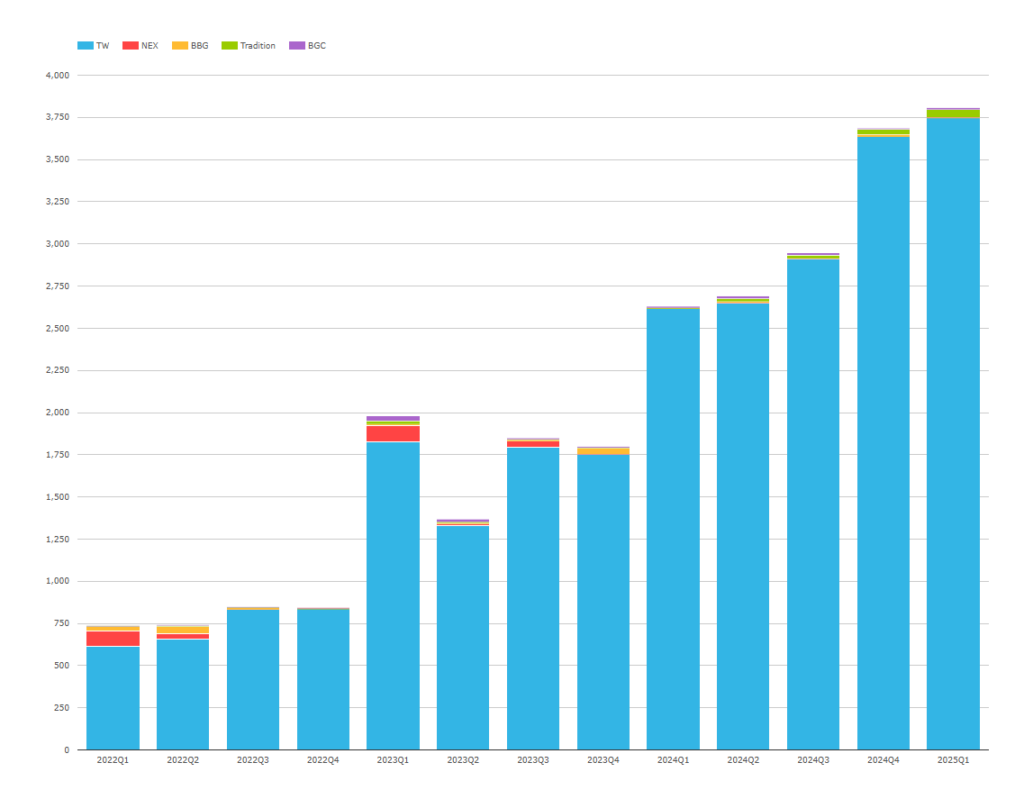

There is finally a SEF Market in CNY!

The popularity of SEF-execution, largely for the workflow benefits, has been a real feature in this series of blogs. I am pleased to report this is no different for CNY. SEF trading now makes up a significant portion of volumes:

Showing;

- SEF trading has really taken-off in the past three years for CNY swaps.

- From 27% of volumes in 2022 (and far lower in 2020), we now see 58% of notional transacted on-SEF in CNY swaps.

From SEFView;

Should I be surprised? Repeating the pattern that we have seen in at least INR, MXN, GBP and CAD markets, volumes on Tradeweb in “other” currencies (i.e. outside of USD) continue to grow.

In Summary

- CNY Swaps Growth: CNY swaps have risen to the 7th largest swaps market, with their share of cleared volumes growing significantly. CNY now represents 12% of swaps trading outside the “G6” currencies, overtaking SEK and CHF.

- Clearing Market Share: Shanghai Clearing maintains a stable 60% market share of CNY swaps, with LCH SwapClear handling the offshore portion. Daily trading volumes have nearly doubled, surpassing $40bn per day in early 2025.

- Increased Clearing & Regulation: The proportion of (offshore) cleared CNY swaps has surged from 60% in 2022 to 90% in 2025. This trend is likely influenced by upcoming Uncleared Margin Rules (UMR) in China, set to phase in from 2026 to 2029.

- SEF Market Growth: SEF trading in CNY swaps has increased from 27% in 2022 to 58% in 2025, with Tradeweb the major beneficiary.