Aka “Everything you wanted to know about Block and Cap sizes but were afraid didn’t know who to ask.”

Since the inception of SDR trade reporting took hold, there has been a concept of capped trade sizes. The general idea being that transparency is good, but too much transparency can be damaging. The CFTC understood that, so they instituted a threshold for swaps after which the trade size that gets disseminated to the public is capped. Trades beyond this threshold (the “Cap Size”) get reported as the capped amount. This prevents competing market participants from seeing that massive size has gone through a particular instrument, such that the original price makers have a chance to hedge the position accordingly, and somewhat shields the parties from being identified. It’s part of the Block trade rule, which further delays such trade reporting by 15 minutes.

We’ve known about this for some time. Amir first blogged about the topic back in June of 2013 here.

And if you’re really interested in this topic, you can either read all 200+ pages of the multiple official CFTC documents that reference block and cap sizes:

- “Real Time Reporting Rule” – January 2012 (85 pages)

- “Further Block Proposal” / Proposed Rules – March 2012 (69 pages)

- “Block Trade Final Rule” – May 2013 – (80 pages)

Or you can just read the rest of my blog (1 page).

DEFINITIONS

While we have known about this topic for some time, we do get asked occasionally what these sizes are, and when they will change. Further, people often confuse block sizes with cap sizes. I’ve been quick to tell people that the two are not necessarily the same; the Cap size can be larger than Block sizes.

So first, my quick definition:

- Block Size: The notional threshold for which a trade can be a “Block” and hence must be executed away from a SEF. (Disputing “must be executed away” and “can be executed away” is the subject of another article).

- Cap Size. The notional threshold to which the public reporting of the swap is capped.

IN THE MIDDLE OF THE PHASE BEFORE YOU START

The CFTC used some terribly confusing phases. Starting with “Interim”, leading to “Initial”, and ending with “Post Initial”. So, the Interim period occurred before Initial. For the quants in the audience:

Interim < Initial < Post-Initial

To top it off, we are now (November 2014) in the Initial phase for Block Trade Reporting rules, but in the Post-Initial Phase for Cap Sizes. I think. But the Post-Initial phase for Cap sizes is based on the phase of the Block sizes. Confused? Me too. It’s times like these that we have to look for empirical evidence which we have in abundance in SDRView. This shows that indeed trades are currently being capped at the block trade schedule (there is not currently a separate Cap schedule).

However, the law is very clear that Cap sizes are designed to be larger than block sizes.

WHERE ARE WE GOING WITH THIS

So while it might be confusing to understand where we are with Block and Cap sizes, the law is very clear on where we will end up. Once we get to the “Post-Initial” period for blocks, there will be two schedules for every product, currency, and tenor:

- Block Schedule based on 67% notional

- Cap Scheduled based on 75% notional

So when will we get there? Well, the “Post-Initial” phase was due to begin “at least” May 2014 (many months ago). The term “At least” has been interpreted by the CFTC to mean that is the earliest possible time they would come up with a new schedule.

Note to self. I should try this next time my wife hassles me for not doing a chore:

- Wife (on Sunday): “Can you at least take the trash out by Tuesday”.

- Wife (on Wednesday): “You didn’t &*%! take out the trash!”

- Me: “Sorry honey, but I thought you meant any time AFTER Tuesday”

But what this means is that the CFTC can at any time surprise us with a new Cap and Block size schedule based upon the prescribed 67% and 75% logic.

67% OF WHAT?

For details on how to determine the 67% (and 75%) threshold, you can read pages 70-72 of the Block Rule. I have summarized it here in 11 easily digested bulletpoints:

- Take all swaps reported (eg all 10YR fixed float USD swaps) for previous 1 year period

- Remove non-publicly reportable transactions (eg inter-affiliate)

- Convert to a common calculation currency, eg USD

- Remove trades beyond 4 standard deviations from the average

- Sum the notionals (You’ll get a big number, let’s assume 10 bazillion)

- Take 67% of that amount (6.7 bazillion)

- Order all swaps in your sample set by notional size

- Start adding them up from the smallest trade

- When you get to 6.7 bazillion total (let’s hope you don’t get distracted and have to start over), stop.

- Observe the notional of the trade that put you over the 6.7 bazillion mark. That is the 67% threshold. (Let’s assume this is 303 million)

- Round the notional of that trade to the nearest 10 million (300 million)

Humor aside, it seems a reasonable approach. However I might point out:

- Should CLOB’s become active and reduce the average trade size, the block and cap sizes should drop along with it.

- It is susceptible to manipulation by participants putting through a bunch of small trades. However, the cost of 100’s of 1mm lots instead of a single 100mm lot would vastly outweigh any benefit gained by decreasing the block and cap size.

- Without highly reliable data, this becomes a herculean and error-prone task for the CFTC. Just imagine if they were looking at allocation-level trades instead of the blocks traded.

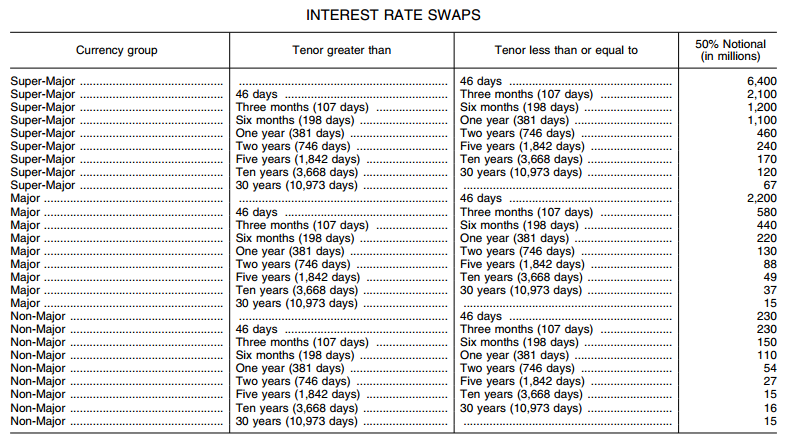

WHAT DOES THIS LOOK LIKE

The actual schedules for swaps start on page 78 of the Rule. I’ve taken a snippet of it here for your reference.

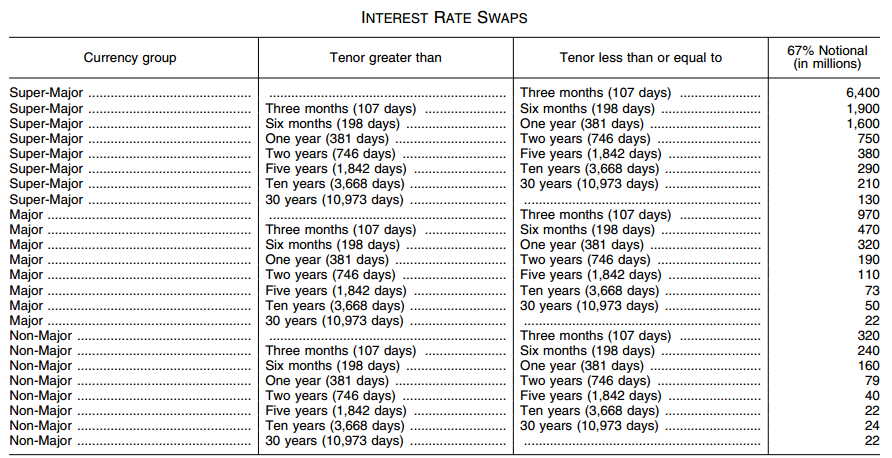

If you are interested in what this might look like when we get the 67% designation, look no further than the original, 2012 “Further Block Trade” proposed rule, which had assumed 67%:

Hopefully that might give you some insight into what the upcoming 67% Block and 75% Cap schedules will look like.

FINAL WORD

Transparency in the OTC swaps market is directly impacted by the block trade rule. Like many of you, we at Clarus want to see as much and as clean data as possible. Let’s hope for a swift transition to the Post-Initial period in swaps reporting.

Todd-

Thanks very much for the thoughtful post. I have been struggling to interpret/apply this rule as well. Perhaps with your expertise we could start a dialogue on a few items I have been wondering about… Please feel free to answer all, none, or some of these!

1. You added the original 2012 ‘67%’ guidance for blocks, do you know if a corresponding table exists for 75% cap?

2. When will we be in the interm/post-initial phase for blocks?

a. Since we are in the post-initial for cap, but the initial for blocks, how does the cap get calculated off of the block size?

3. How will complexities of these be handled for cross-currency swaps between let’s say USD/ZAR or SuperMajor/NonMajor? Page 76 speaks to currencies, but it isn’t clear to me how these complexities are addressed.

Hi Jon,

Thanks for the comment, glad you found it useful. Few responses to your questions:

1) No, I do not believe a cap schedule is out there, particularly given that I interpret the Initial phase of blocks to mean that we will use the Block schedule for Caps. Hence no need. But happy to be told I’m wrong here.

2) I’m led to believe the CFTC is ‘working’ on the 67% block schedule. I had expected May 2014 for the new Block schedule, which clearly hasn’t materialized – which is one of the reasons why I went back to do some research on the topic and determined that “at least” means “after” May 2014. I’d be guessing, but would think that the CFTC want to make sure they are working with ‘clean’ data before they make this assessment. Your guess is as good as mine here.

2a) I think, until the 67% block comes out, that caps = block for now. I fully expect a 75% cap schedule to be published at the same time as the 67% block schedule.

3) Good question. I’m hopeful that’s been addressed somewhere (I’d favor a “take the more senior ccy amount” approach). But no idea.

Tod, really enjoyed reading this. A sense of humour combined with demystifying notional amounts, well done.

From reading this post, the comment “remove non publicly reported transactions” – does this imply inter-affiliate trading which does “not” take advantage of clearing exemption, is “not” publicly reported and displayed in SDRs?

Hi Ken, thanks for the comment. The actual example they give is on page 75 of the final rule if you are inclined to read it. I interpret the intent is to just use the reported “alpha” trades. So the beta/gamma trades (such as the tearup of the bilateral and replacement with 2x cleared trades) are not included in this. As well as inter-affiliate trades that are not reported. And, now I’m guessing, but I would think most inter-affiliate trades are not cleared (hence no alpha or beta or gamma trades). And even if an inter-affiliate trade was cleared (did not take advantage of exemption), I would believe the CFTC would endeavor to remove these trades from the calculation. I generally do not believe we see inter-affiliate trades on the SDR tape at all. If you know otherwise, I’d be interested to hear.