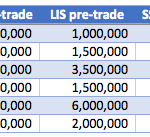

MiFID II Bond Transparency Calculations

As Jan 3, 2018 is now just three months away, I wanted to update my February 2016 article MiFID II and Transparency for Bonds, in particular as ESMA have now published Transparency Calculations and compare these to transparency in the US Corporate Bond market with FINRA TRACE. Background Post-trade transparency and pre-trade transparency for Bonds is meant […]

Introducing Our Daily Briefing, Direct to your inbox

Introducing the new Clarus Daily Briefing. Curated market information direct to your inbox. Swap rates, volumes and Central Bank rate expectations every day. Make sense of daily trading activity in less than 2 minutes. We offer a free two-week trial before your paid subscription starts. Daily Market Commentary We always aim to improve the general […]

MiFID II: Why Research is in the News

There have been many recent articles on Banks having to charge for Research as required under MiFiD II, see here, here and here, so I thought I would look into the detail. Inducements The relevant text in the EU Commission Delegated Directive is in Chapter IV: Inducements, the title providing a clue to the intent. This Chapter […]

MIFID II Transparency will leave us in the dark

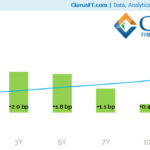

We run the SSTI and LIS thresholds over US SDR data. We anticipate that over 80% of EUR swaps will not be subject to pre-trade transparency. Post-trade transparency will not be much better. 75% of the risk traded will remain dark for up to four weeks. We are intrigued to see what the APAs will […]

Our Response to the ESMA Trading Obligation Consultation

ESMA published their latest Consultation on Trading Obligation for Derivatives under MIFIR on 19th June 2017. As we stated back in June, we have concerns about the quality of the data used to determine the Trading Obligation. We have therefore offered to make all of our SDR data available to ESMA as part of our response to the […]

MIFID II: What Should Transparency Look Like?

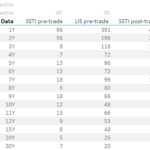

We replicate the transparency calculations published by ESMA, using SDR data on EUR Swaps. EUR swaps are the second largest IRS market, and yet do not benefit from real-time trade level reporting. Our data shows that most of the EUR IRS curve is “liquid”, with ADV >€50m. SDR data calibrates realistic pre-trade transparency thresholds at €50k […]

MIFID II Transitional Transparency

ESMA have published Transitional Transparency Calculations for a number of asset classes. These calculations define which asset classes and instruments are deemed liquid for the purposes of making trade data public as of 3rd January 2018. Anything deemed “illiquid” will likely have a two-day lag applied to the trade record being made publicly available. The transitional […]

MIFID II: ESMA Trading Obligation

ESMA published their latest Consultation on Trading Obligation for Derivatives under MIFIR on 19th June 2017. EUR, USD and GBP swaps are deemed liquid and will be covered by the Trading Obligation under the current proposal. JPY, NOK, SEK and PLN swaps will continue to be covered by the Clearing Obligation but will not be […]

MIFID II: Transparency Data

Following on from my article on the MiFID II: Instrument Reference Data, I wanted to look at the “Transparency Data” mentioned in the briefing note released by ESMA on 12 Jan 2017, titled “MiFID II technical data reporting requirements“. This starts with the following table: Showing that from September 2017 ESMA will start collecting Transparency data. Transparency Data […]

MIFID II: Instrument Reference Data

Following on from my article on the Trading Obligation For Derivatives under MiFIR, I wanted to look at more recent documents released by ESMA for MiFID II and MiFIR and found a briefing note released on 12 Jan 2017, titled “MiFID II technical data reporting requirements“. It starts with the following table: Interesting. Lets look […]