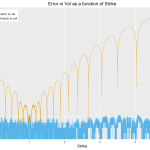

Bachelier Model: Fast Accurate Implied Volatility

“An industrial solution” – provides computation to near machine precision for option prices over an extremely large range! Fast and analytic in nature, employs rational polynomials to determine implied BpVol. Follows the Bachelier model; that is, dF = σdW. A new method for computing implied BP Vol (basis point volatility) analytically has come to light. It is described by […]

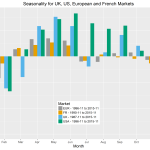

Exploring Seasonality in a Time Series with R’s ggplot2

Inflation index values are decomposed into trend, seasonality and noise. Certain types of graph help identify seasonality. Graphs can be created simply and quickly in R. Simple graphs can be refined for stronger visual impact. Recently, I have been looking at inflation indices and studying their seasonality. The best way to see the overall trend and seasonality in this […]

Starting an Internship Programme at a Startup

In the UK, the notion of an internship is fairly new (to me at least). It was not straight forward to set up a program, so I share a few of the key steps I have found to be useful. The documents “Common Best Practice Code for Quality Internships” and “Internships that Work: A Guide […]