Mechanics and Definitions of Cross Currency Basis Futures

CME are taking a bold step into the (relatively) unknown and launching EUR/USD Cross-Currency Basis futures. Let’s take a look… Definition The Cross-Currency Basis Future can be defined as; A contract for difference that cash-settles the implied 3 month cross-currency basis from observable EUR/USD FX-forward, USD and EUR short-term interest rate futures. Recall that a […]

USD Rates 2024 Review

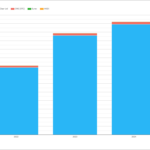

Cleared USD Rates We start with looking at notional volume cleared in OIS referencing either Fed Funds or SOFR indices. 2024 volume of $264 trillion is a new all time high (across both OIS and Swaps), exceeding the previous high set last year. All of that volatility over the Summer and the election drove volumes […]

USD Rates – What’s New?

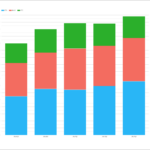

USD Outright Volumes The chart below shows monthly volumes since Sep 2021: Showing; And we shouldn’t avoid the chance to present another impressive chart. Average Daily Volumes in USD Rates keep on increasing each quarter: Will September 2024 be busy enough for us to close the quarter with another record? Stay tuned to the Clarus […]

Just how bad are trading conditions right now?

This is very likely a premature blog. But it’s August, it’s quiet, and I haven’t written a “live” blog since Credit Suisse went up the swanny. So whilst Bloomberg is declaring a “$6.4 Trillion Stock Wipeout” and Reuters a “Global Market Rout” I note at the very outset that more sanguine minds rule over at […]

GBP Swaps – What’s New?

It’s time to take a look at UK swap markets. I tend to do this about once a year, and the last time was June 2023: Again, I will reference FT Alphaville for their great coverage of the UK and in particular highlighting the potential for stability in one of their recent posts: A good […]

Allocation Workflow in Futures and Options

At Industry Events focusing on Futures and Options, you often hear about trade allocation workflow and efforts to improve this important post-trade process. Not knowing much about this topic, I recently read a very interesting article, “The evolution of F&O clearing workflows: Let’s talk allocation!” on the ION Markets Blog. Well worth a read.

Could “enshittification” happen in derivatives markets?

*Disclaimer – this is a tongue-in-cheek consideration of third-order risks in our markets. Hope you enjoy. For those who missed it, the FT introduced us to “enshittification” last week, and the article has no doubt made the rounds of trading floors ever since: https://www.ft.com/content/6fb1602d-a08b-4a8c-bac0-047b7d64aba5 Why are we choosing to talk about it on the Clarus […]

USD Rates Overview in 2024

We have previously noted that EUR Rates are now larger than USD Rates in terms of notional traded across OTC swaps (see here and here). This change has arisen because EUR has continued in a multi-rate environment – both €STR and EURIBOR swaps still trade, whilst USD has largely moved to SOFR, with Fed Funds […]

Swaps Compression: What is it and why is it important?

Another interesting article on the ION Markets Blog provides an introduction to Swaps Compression, for those not familiar with this or just needing a referesher on the what and why, please read at Swaps Compression: What is it and why is it important?

HJM-FMM Model – Fast Calibration via a Neural Network

Authored by, Davide Gianatti, Serena Manti and Gianluca Molteni of the Financial Engineering and A.I. team at List. The aim of this post is to introduce a novel systematic approach that could be used to calibrate quickly any model describing interest rates. The core of the algorithm is a Neural Network (NN) that outputs the parameters […]