Regular readers may recall that we looked at the break of the SNB’s EUR/CHF cap back in January 2015 in this blog. “Francaggedon” was a unique event without any pre-warning, and yet we were still able to see evidence in the data of fortuitous/lucky/profitable trading strategies in fairly decent size.

Now that the “Brexit” referendum has been announced for 23rd June 2016, are we about to see large volumes of EUR/GBP FX Options struck around this date?

The Data

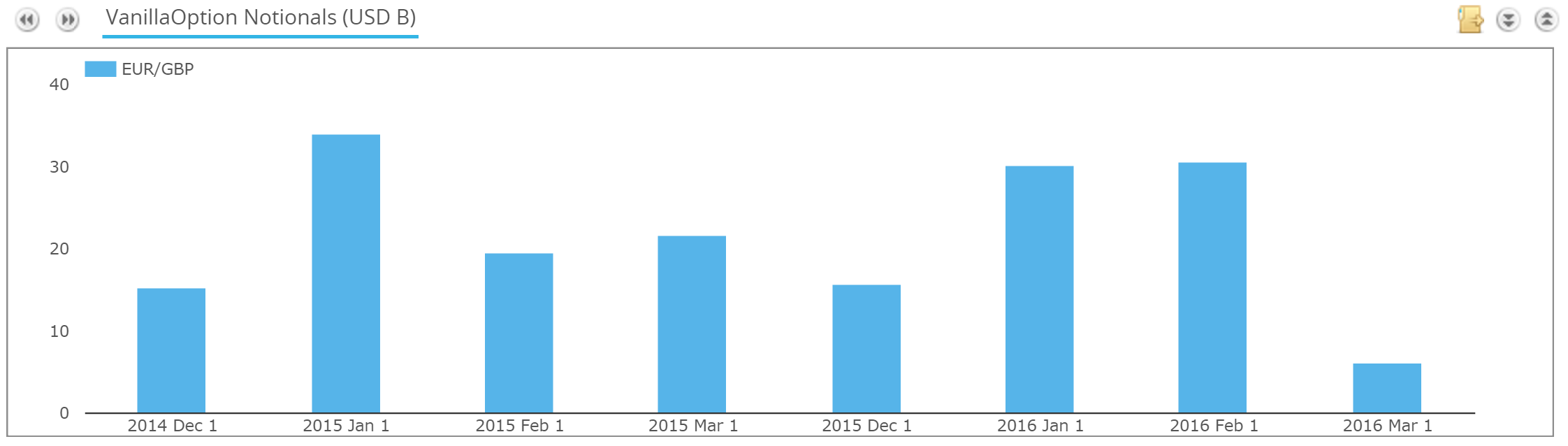

David Cameron announced the exact date of the referendum on 20th February 2016. Therefore it makes sense to compare EUR/GBP FX Option volumes between 2015 and 2016. This is simple in SDRView Researcher using the “Year on Year” flag that we recently added:

Showing;

- An average monthly volume in 2016 of $30.5bn, plus $9bn already traded in March

- Versus an average monthly volume in Q4 ’15 of $25bn

- So we can say that whilst peak volumes in 2015 were higher, activity has picked up slightly in 2016.

However, it’s quite disappointing really. Given the “unknowns” associated with a Brexit, I thought we’d see more of a clamour towards insurance type of structures. Maybe bank desks are simply unwilling to write any options these days?

General Volume History

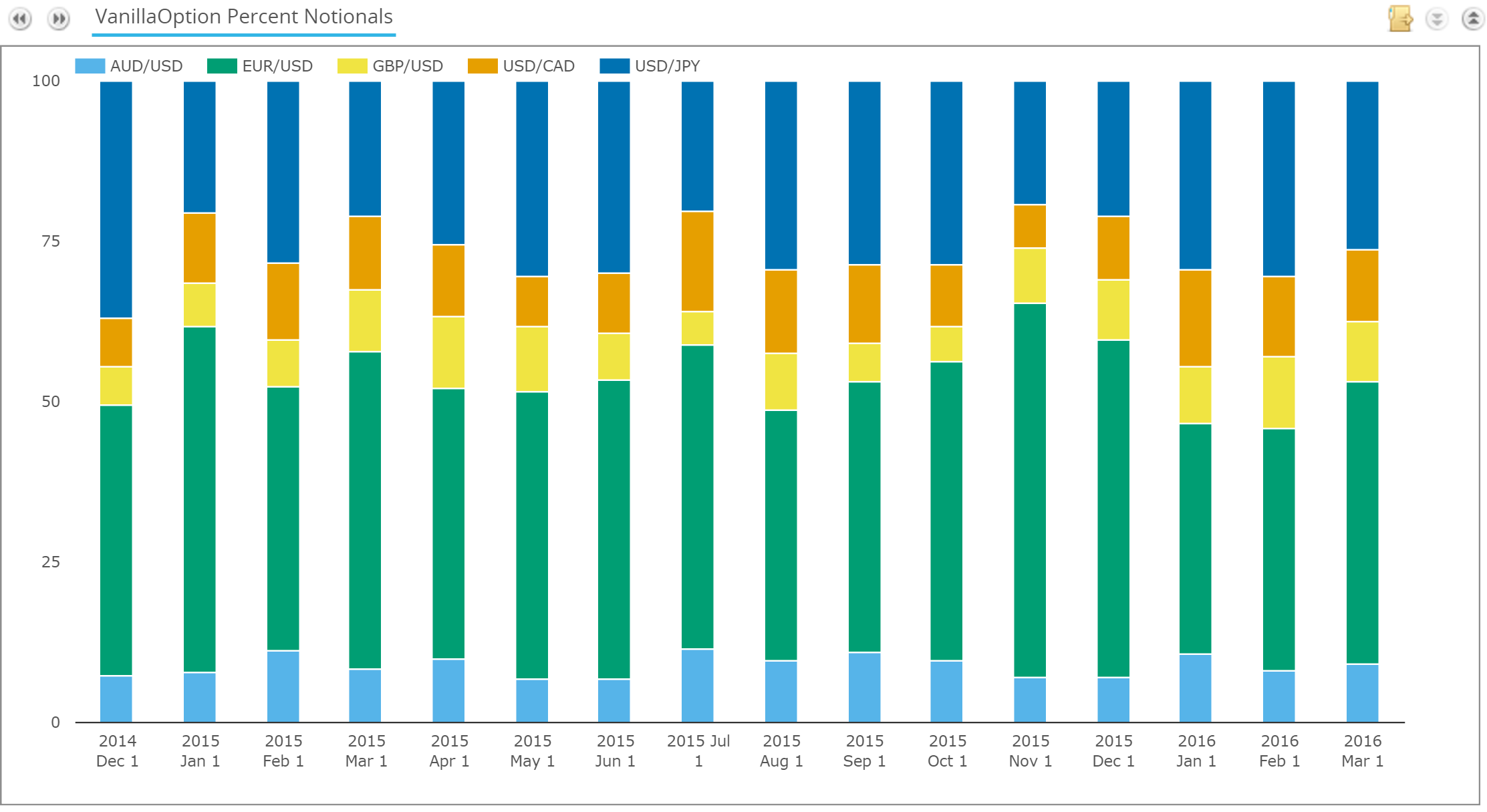

With that thought in mind, I wondered if we are now seeing a larger percentage of activity in GBP/USD options relative to the other major currency pairs. Let’s look at the time series between 2015 and 2016 for activity by currency pair, looking at their percentage share of notional:

Showing;

- GBP/USD options are becoming more widely traded – slowly

- February 2016 represents their best month in terms of “market share”, accounting for over 11% of options traded across the 5 currency pairs above.

- GBP/USD previously saw large volumes in April 2015, presumably related to the closely run General Election.

- Interestingly, volumes were largely unaffected by the 2014 Scottish Independence referendum.

Generally speaking, we do not see a big impact on GBP/USD FX Option volumes related to political events in the UK. This is somewhat surprising as these events undoubtedly impact prices.

Upcoming Maturities

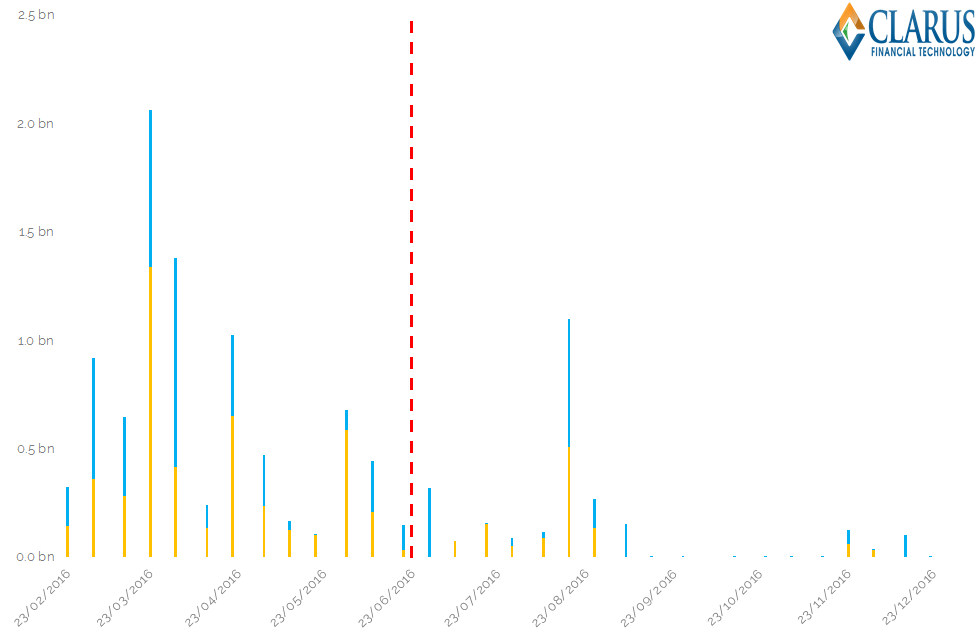

Nonetheless, it’s still worth persevering to see if we can find any evidence of Brexit-related Option strategies. So let’s look at the expiry ladder of EUR/GBP FX Options traded year to date:

- Notional of FX Options traded since the 20th February (the announcement date of the Brexit Referendum)

- Chart shows weekly expiries up to the end of 2016 (Puts in orange, Calls in blue).

- As is typical, notional amounts are greatest for shorter expiries

- We see another peak towards the end of Summer, in August 2016…

- ….but there have been very few options struck around the exact Referendum date.

- Maybe we need to wait for shorter-dated expiries, with their increased liquidity, to fall over the Referendum date to see some meaningful volumes?

Interpreting the Volumes

The volumes seem to be telling us two things:

- The uncertainty is baked into the price of the underlying, not in the activity of options. GBP/USD is historically weak, which is associated with periods of political uncertainty.

- EUR/GBP has already rallied aggressively since last year. This 10% plus rally flies in the face of the interest rate differentials, where the ECB retains its easing bias. But will the EUR really benefit from the UK leaving? Macro Man has a particularly well-balanced piece on this here.

Is It a Time Issue?

Borrowing from the Macro Man piece, maybe the reason option activity remains so subdued is due to the sheer time it will take for the subsequent negotiations. Yes, the Referendum happens in June – and yes, market prices will undoubtedly react at this time. But realistically, any split from the EU will not happen for another two years. As per Article 50;

3. The Treaties shall cease to apply to the State in question from the date of entry into force of the withdrawal agreement or, failing that, two years after the notification referred to in paragraph 2, unless the European Council, in agreement with the Member State concerned, unanimously decides to extend this period.

So maybe we’ll have to widen our net as to what we look at in Options space.

We’ll certainly be keeping our eye on the activity over the coming months, so remember to sign up below to stay informed.