Guest Blog Series

Guest Blogger Profile: Interest Rate Swaps trader. 12+ years’ experience, European and cross markets focused

Gather round and let me tell you a (hypothetical) story……

After the ECB cut rates, a friendly Debt Capital Markets executive pitched an idea to the European Investment Bank about selling some USD bonds. The EIB were very interested, because from a check of basis swap prices, it looked cheaper to issue bonds in USD and swap them back via the Cross Currency markets than issuing directly in EUR (I fear I may have lost some of my younger readers already with that punchy sentence….).

The EIB are an experienced, transparent issuer and so were kind enough to let the whole market know they were about to issue USD bonds, and in what maturity:

*EIB TO SELL $3B 3Y NOTES; MAY PRICE TOMORROW, Jun 10 2014 14:56:44

You may expect a rush of activity as a result of such an announcement.

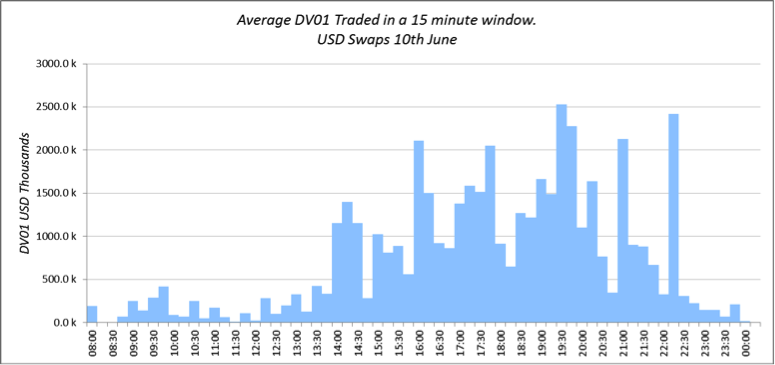

Using SDRView we can export the intra-day trade activity in USD Swaps for 10 June and we see this is certainly not the case:

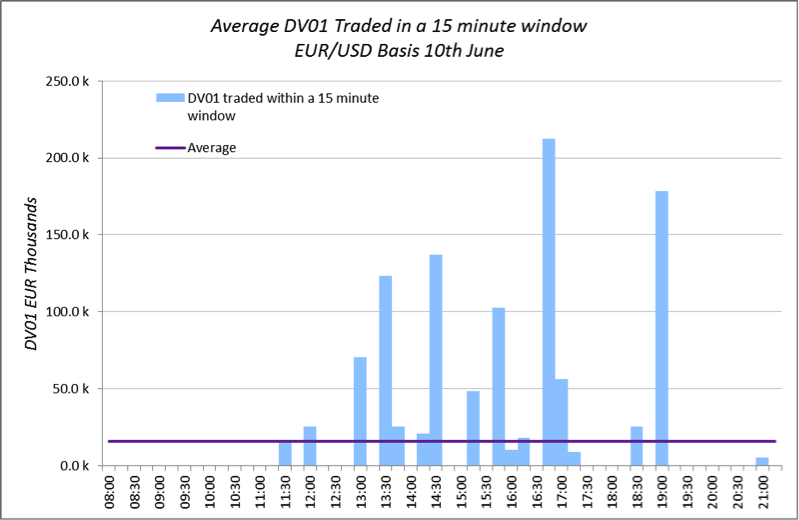

And similarly in EUR/USD basis, there is no discernible spike in volumes:

So, assuming swaps traders are already well fed (if not well watered) and therefore didn’t miss the announcement due to an extended lunch break – why is there no discernible uptick in activity on June 10, given that valuable information about upcoming flows has been provided to the market?

Well, this is a story of a well-managed capital markets transaction. (Disclaimer: I have no connection with this transaction nor the banks involved. The only information I have has been gleaned from analysis of the Clarus SDRView data, plus other widely available news feeds).

Traders hear of these flows and communicate with their marketers. Does anyone have any clients looking to receive EUR/USD basis in the 3 year area? I have an axe. (Sorry, this isn’t about to turn into Game of Thrones. No incest, no nudity, no bloody battles. This is the capital markets, not the Seven Kingdoms…, just how speak on the trading floor). Are there any accounts looking to pay 3y USD rates? This is like manna from heaven to these transaction-starved marketers who spend most of their days signing –away (sorry!) up their clients onto electronic trading systems. They finally get to pick-up their phones and practice their narrative. Zoopla and how well the property market is doing even gets mentioned (briefly).

The ensuing conversation isn’t a quick one. Credit lines have to be checked, settlement limits verified for cross currency swaps. Customers have to dust-off their playbook of what to do in cross currency markets when the central bank cuts rates into negative territory, and how to play the Fed in a rising rates environment. Traders will frantically bang-out a “daily” commentary, which for some reason hasn’t been written since May. Artfully pointing out what a good idea it is to pay USD rates with the Fed eyeing exit policies.

The salespeople will come good – given time. The two risks being hedged are very different. For example, EUR/USD Basis swaps markets are not particularly active. Using SDRView, we see only around EUR16k DV01 trades every 15 minutes on average, making for a total of EUR800k per day. The EIB have announced $3bn of 3 years – equivalent to nearly EUR700k DV01. The salespeople have time to canvas their best accounts as the trader’s axe will last throughout the session. Equally, in USD Swaps they know the trader will want to transact the bulk of the risk as close to the EIB transaction as possible – which is expected in another 24 hours’ time.

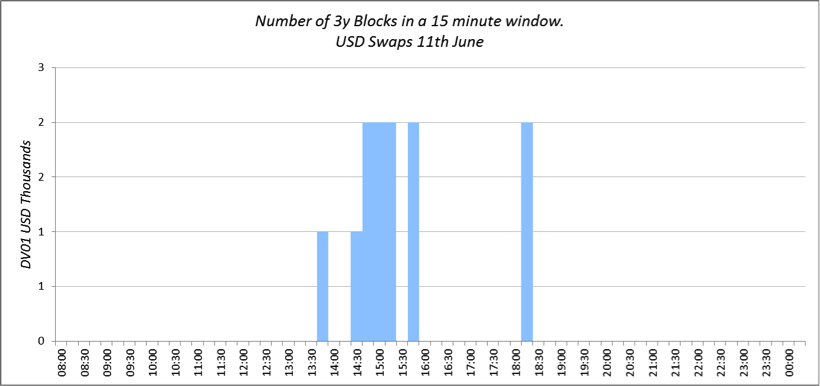

When we look at the data, this activity is not readily apparent at first. This is because when a trader has an axe, he or she really wants to get rid of the position. He doesn’t want to mess around with poxy market-sized transactions. Sales people – the trader wants you to bring in those elephant trades. Those trades that blow through the block thresholds on reporting and allow him(her) to smoothly shift risk through the markets. He understands that these are the tickets that it takes time to print and he will be patient. And indeed, that is exactly what we see happening in the data. In USD Rates, 3y block activity is concentrated around the bond pricing on 11 June. The bond pricing announcement below hit newswires at 15:41 CET:

*EIB SELLS $3B 3Y NOTES AT MS FLAT, UST+17.25BPS, Jun 11 2014 15:41:29

And if we look at block trading activity in 3Y USD Rates, we see block trading activity for 3Y Rates concentrated around the time of the bond pricing:

Plus in SDRView Professional for EUR/USD basis, on 10th June we see two block tickets, late in the session, 3 year maturity:

It is a fair bet that all of these trades, whilst only being reported up to the EUR70k DV01 threshold, are substantially larger than that. And having found these offsetting positions, the trader is happy, the salesperson is happy and all of the customers are over the moon with transactions well-hedged.

And so ends our hypothetical and voyeuristic story.

For those wishing to take the analysis further, SDRView can be further utilised to look at a number of other aspects of the transaction.

For me that is a story for another time and place.