We spend a lot of time analyzing IRS clearing activity for CME and LCH, primarily because it is close to home and about as much of a fist fight as we are going to see in swaps.

But what about the rest of the world? There are 14 clearing houses that we monitor for OTC derivatives in CCPView. Surely the 12 others have something notable going on.

Particularly relevant to look at this now, as in the past month, we saw KRX in Korea publish their first set of numbers for their IRS clearing service, Comder in Chile launch their Chilean Peso NDF clearing service, and Eurex launch inflation swaps.

So what do we do when those things happen? We of course take note and start plugging their data into CCPView.

So let’s have a look at the data beyond the CME & LCH IRS clearing (which Amir discussed earlier today in his blog).

Let’s get started.

FOREIGN EXCHANGE

I’ll begin with FX. The only OTC foreign exchange trades being cleared is non-deliverable forwards (NDFs). These are simple products with lesser settlement risk (when compared to deliverable FX), as only the mark-to-market gets settled when traded OTC, so it fits nicely into a cleared and daily-variation-margin-settled world.

I should mention however that LCH also announced this week that they seem to have figured out how to clear FX Options. Issues there being with the settlement of the underlying deliverable FX and the ad-hoc nature of expiry. But that is a story for another day that I look forward to analyzing, as that service will not be launched until 2016.

First off, who clears OTC FX NDFs? Well, we have seen clearing services at the following venues:

- LCH ForexClear (12 ccypairs)

- CME (38 ccypairs, although many of them appear to be natively deliverable, eg AUD/USD, so are really “cash settled forwards”)

- SGX (7 ccypairs)

- HKEX (2 ccypairs)

- Comder (as of this past week) – USD/CLP and CLF/CLP

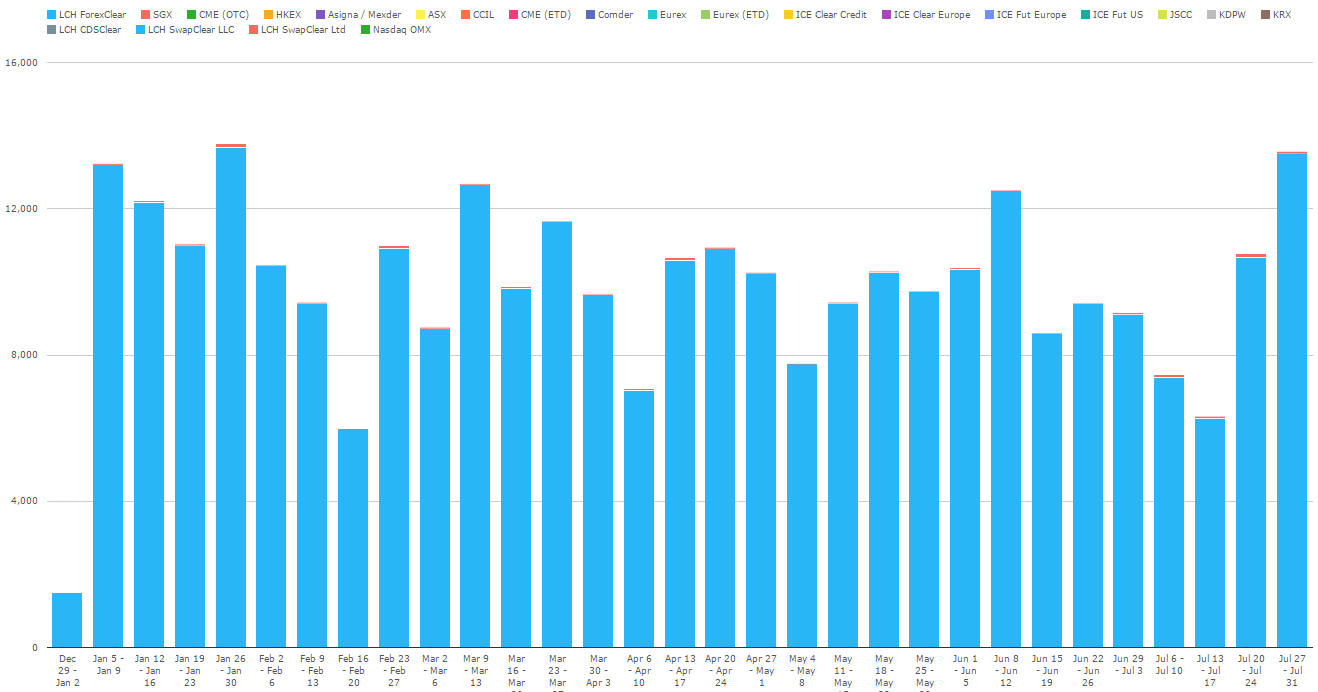

So we have 5 venues clearing FX. But up through the end of July, only one of them shows up on the map. First in terms of Activity (LCH ForexClear is blue):

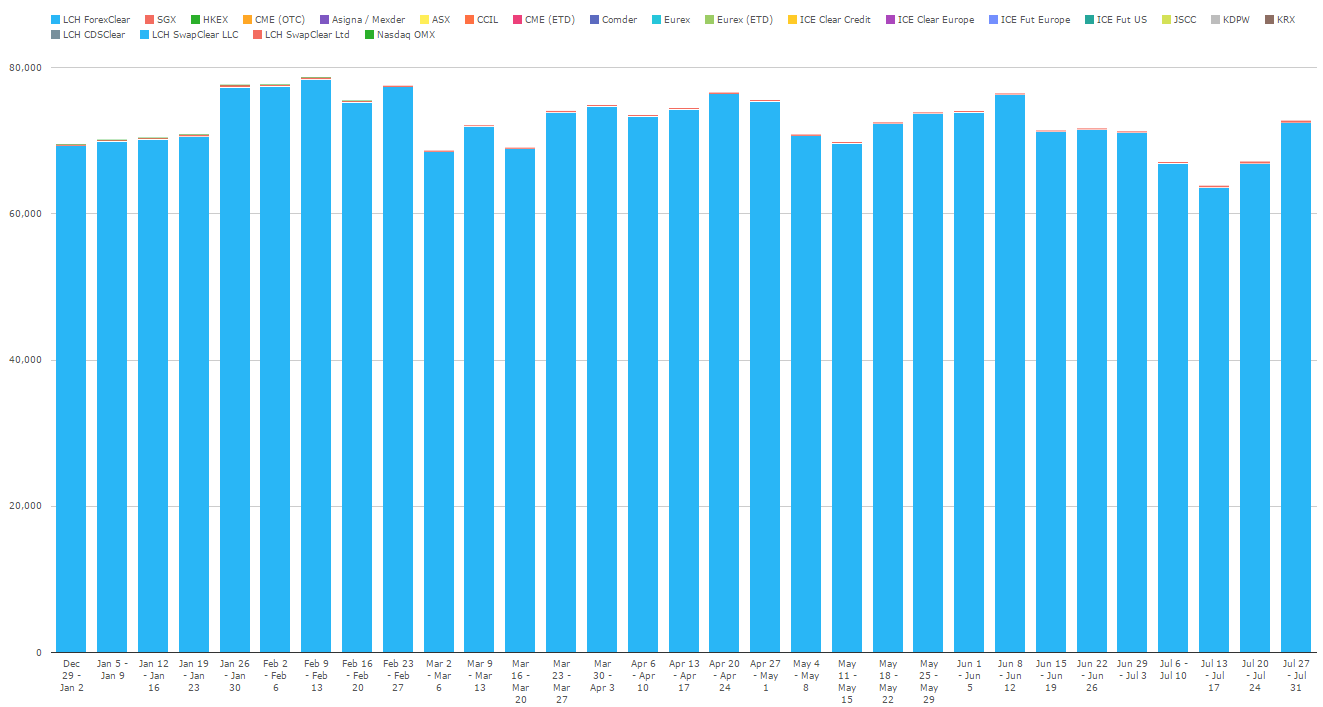

And then in terms of Open Interest:

Pretty easy to see that while 5 venues clear FX, it is really a 1-horse race at the moment, with a small amount of regional activity at SGX and HKEX. I would surmise this is primarily driven by the fact that FX NDF are not mandated to clear.

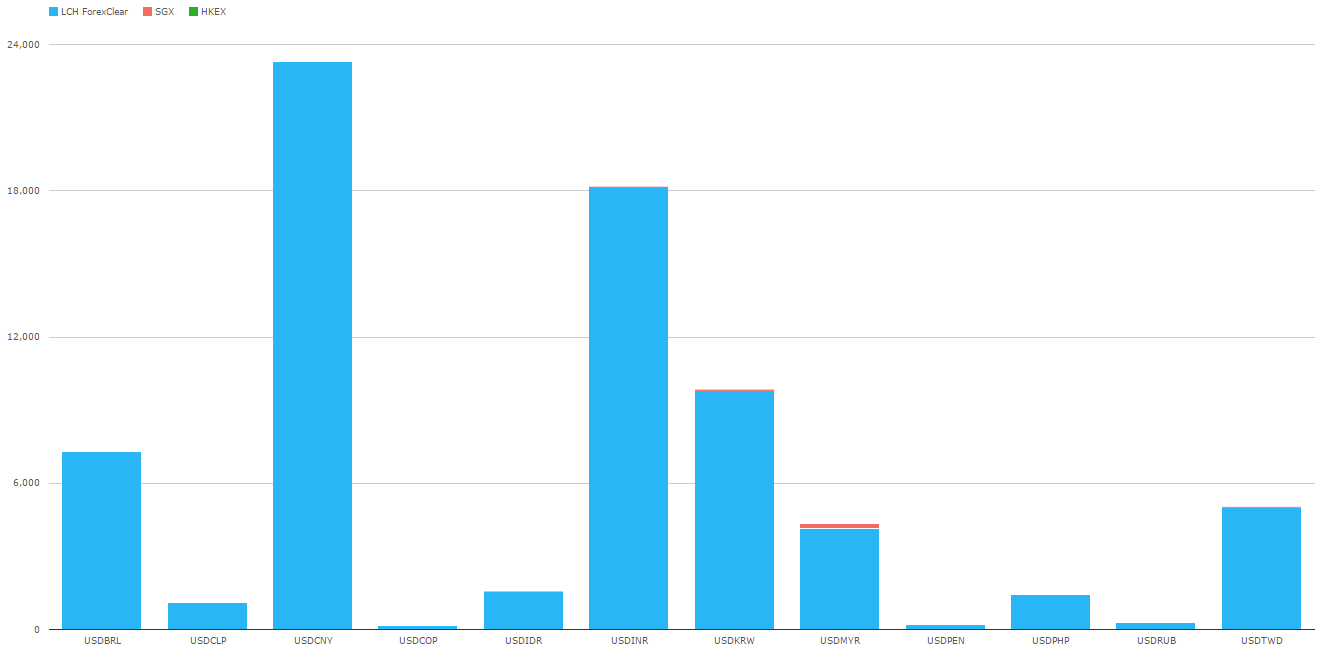

Then in terms of which currency pairs are cleared, let’s look at open interest by currency pair:

This seems to say that USD/CNY and USD/INR are the top 2.

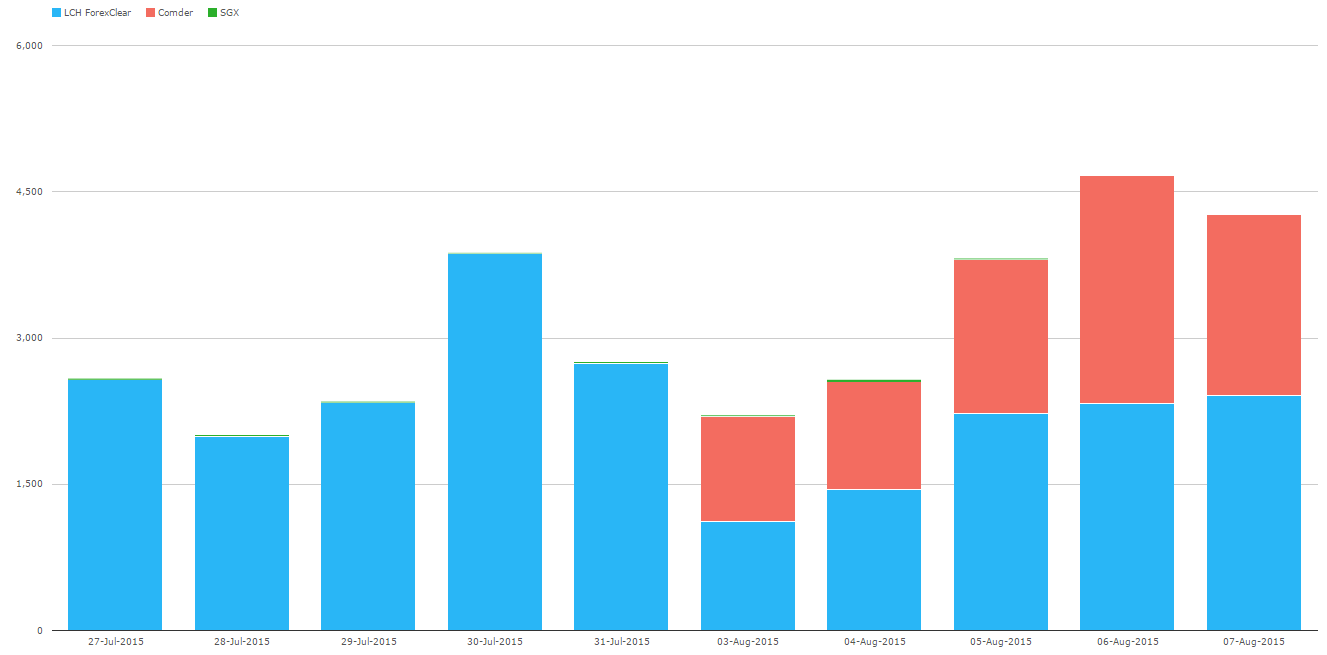

And lets now add in Comder cleared NDFs. They have published data starting August 3rd, shown below in terms of trade volume. Remember we are quoting millions of USD equivalents.

Comder are clearing CLP NDFs, and already their service appears to be a success. So successful in fact, that we are in the process of double-checking our numbers. But if this is correct, that is quite an impressive launch.

CREDIT DEFAULT SWAPS

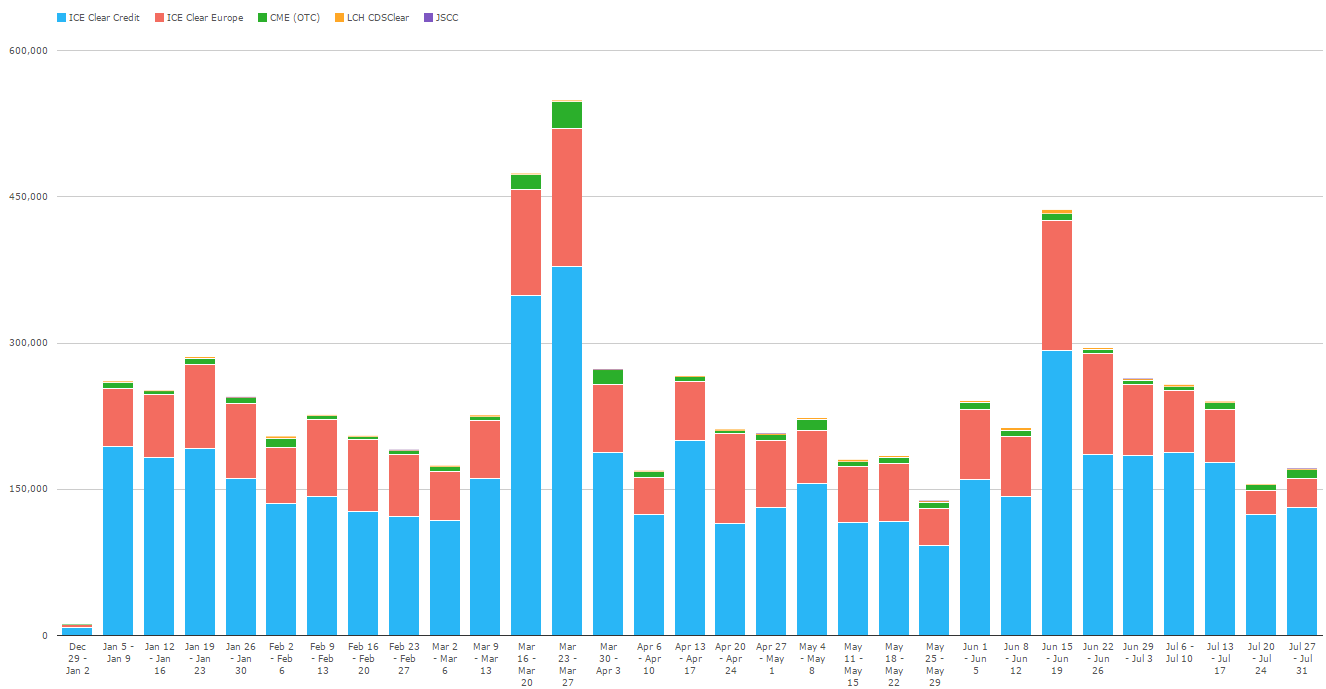

Much like FX is a one-horse race, the anecdotes for credit derivatives is that it is likewise a dominated by one name, this time by ICE. Let’s look at the numbers in terms of volume:

Which seems to corroborate the notion that ICE (blue is ICE US and red is ICE Europe) has the lions share.

Worth noting however that CME (green) appears to have some activity, and we can make out little blips for LCH and JSCC.

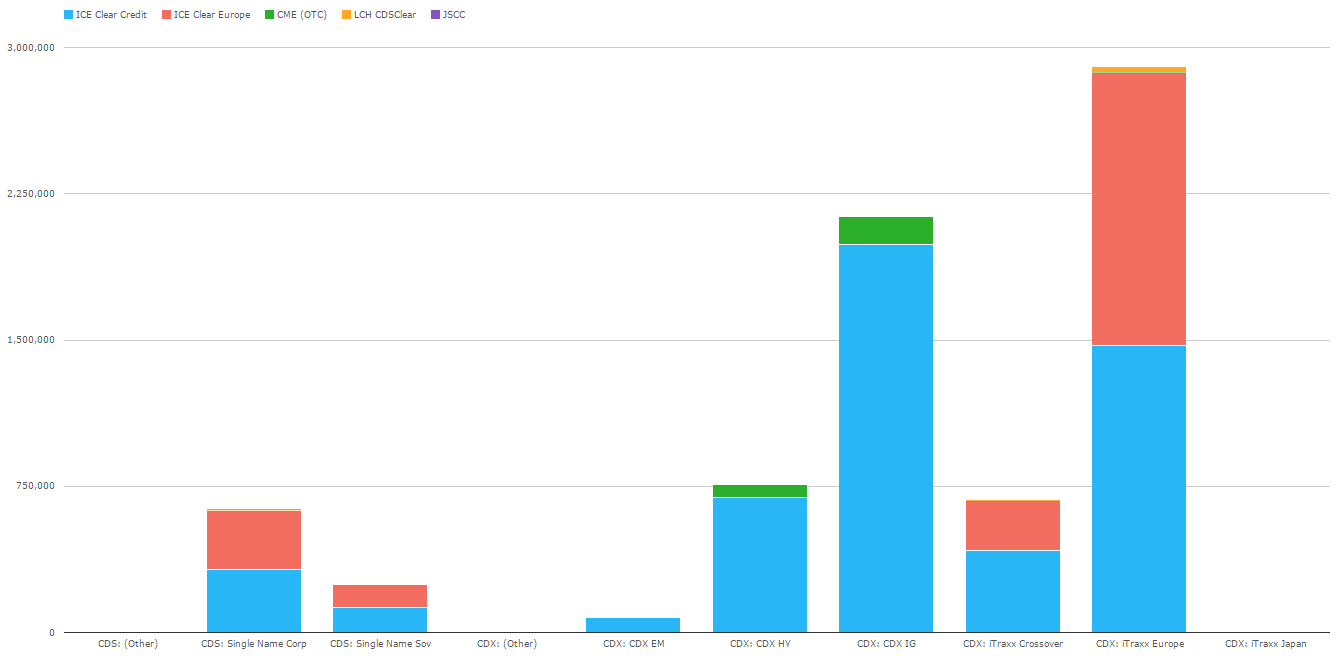

As far as who clears what – it’s what you’d expect – the HY, IG, and primary iTraxx products are the active issues. I do however find it interesting that Single Name CDS is not as insignificant as you might think:

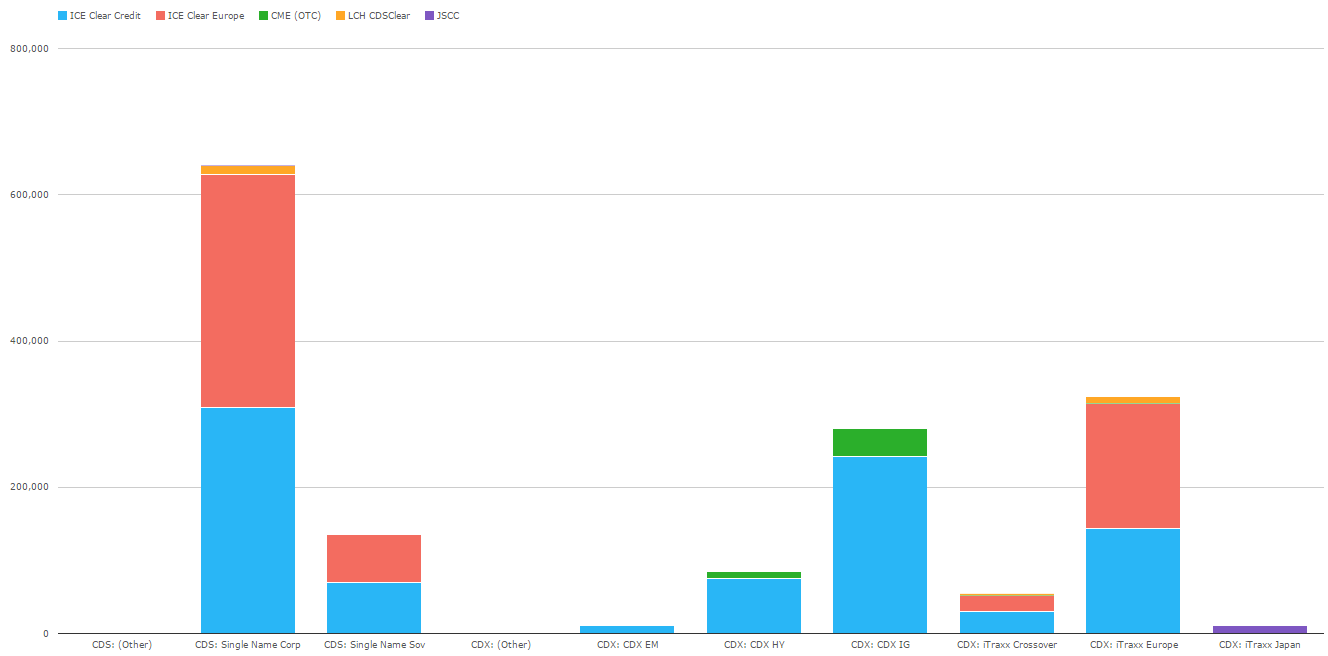

When talking about single name CDS, its often fun to look at open interest, because it nicely demonstrates that while the activity is in the indices, the open interest is in the single names. A very simple explanation would be that there are thousands of “products” in single names (that do not net), hence you get this effect.

INTEREST RATE SWAPS

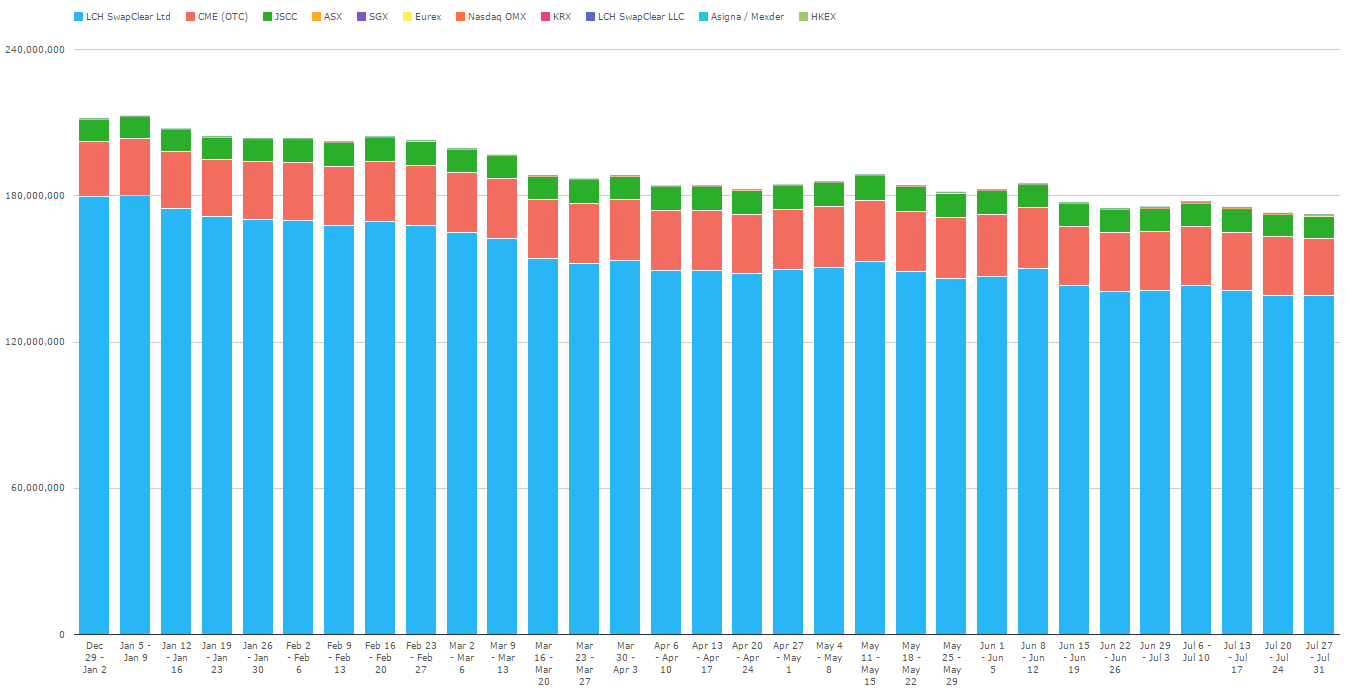

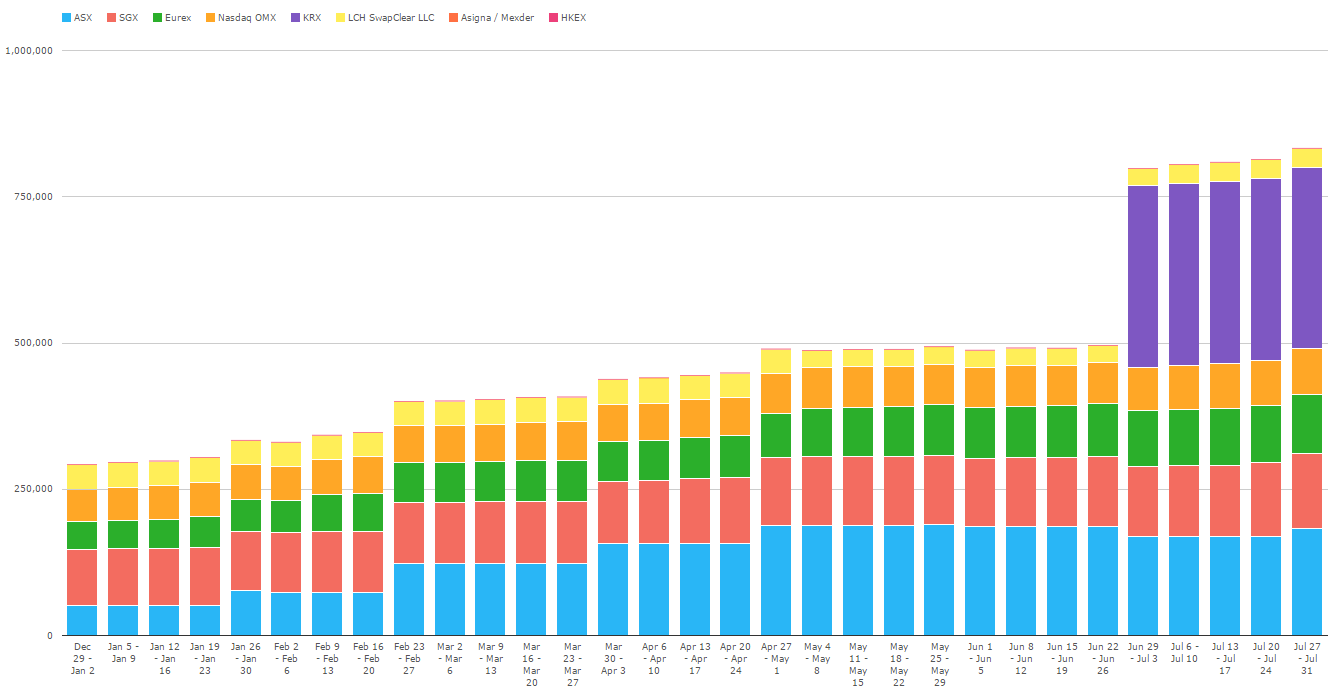

Best to begin with a look at open interest for IRD. We have 11 global venues clearing interest rates, yet the picture is dominated by the usual story that we’ve grown accustomed to:

- LCH out in front

- CME with some success with US clients

- JSCC with local JPY business

Worth noting the downward-trend in this open interest data. It clearly reflects an effort by the industry to compress and terminate trades.

So let’s remove the top 3 so we can observe the tail a bit better. What do we see then?

First, let’s appreciate the change in scale here. We’re still looking at open interest in millions of US dollars. But by removing the top 3, the total open interest has gone from $180 trillion down to a much more tangible $750 billion. Put another way, the 8 “other” IRS clearing houses account for less than 0.5% of the total cleared notional, combined.

But it is interesting to see. ASX has had a successful launch, and the likes of SGX and Eurex are doing probably as good as you can in a world of no mandatory clearing. The other standout here is KRX, who have only once reported clearing activity – hence their sudden inclusion in July figures.

Also worth mentioning that like KRX, some clearing houses only publish monthly data for example ASX, Asigna, and HKEX, hence lending to the binary movement in some of those numbers around month-end.

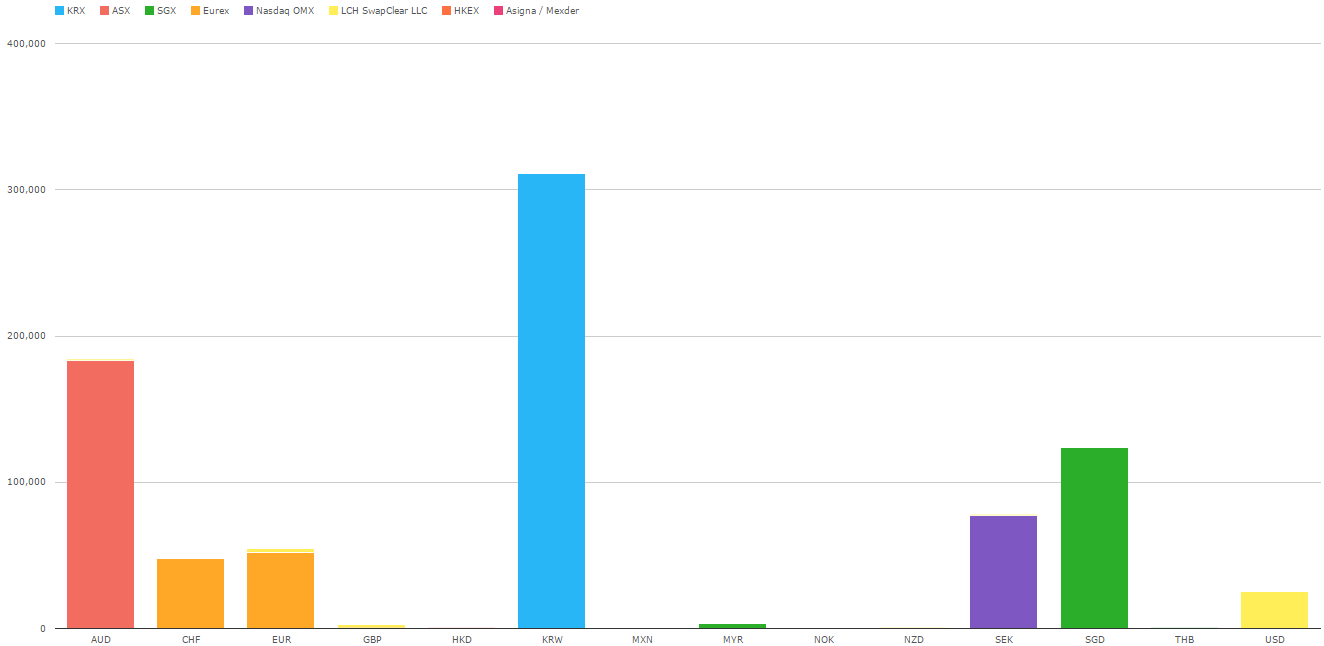

Lastly, let’s have a look at what currencies are active at these “other” clearing houses:

I find this one almost comical, but demonstrates an important point – that the “domestic” clearing houses are really only clearing their domestic currency. I don’t have JSCC in this table, as it would make the others insignificant. But worth noting that they follow this pattern as well, only clearing JPY swaps.

SO WHAT HAVE WE LEARNED

I suppose the takeaways here are:

- FX NDF clearing is small, and what amount we do see is concentrated at LCH

- ICE lives up to the one-horse-race in Credit Derivatives

- Outside of the big 3 names in interest rate derivatives, domestic clearing houses are respectively tiny and focused in the domestic currency

Of course if you want to dig into this data yourself, get in touch.