To all of our readers who, like me, are responding to the latest ESMA consultation, I thought I would provide a simple list of ways that MIFID II data is being made difficult to access. Hopefully this can help to get transparency right in Europe.

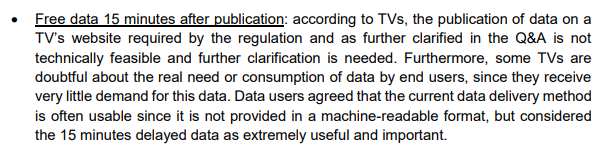

ESMA report that the users of data that they spoke to at roundtable events do indeed find the data unusable:

I assume there is a typo: “Data users agreed that the current data delivery method is often UNusable” from the context of the paragraph

Full disclosure: we work in the data business here at Clarus! We would love to get our hands on more data.

This list looks only at free data which is post-trade, 15 minutes delayed.

1. No data on a public website

I believe that this is the most important aspect of providing free, public post-trade data that is delayed by 15 minutes.

The ESMA consultation asks us to “identify deficiencies” and to be specific. Therefore, can anyone help identify the free, public data from this APA? The transparency link does not take me to any displayed data nor downloadable slice files:

2. No way to programmatically consume data

Delayed post-trade data has no value from a standalone venue or APA. Delayed post-trade data is useful as a way of monitoring a whole market. This particular data is used for research purposes, improving market understanding and to promote transparency.

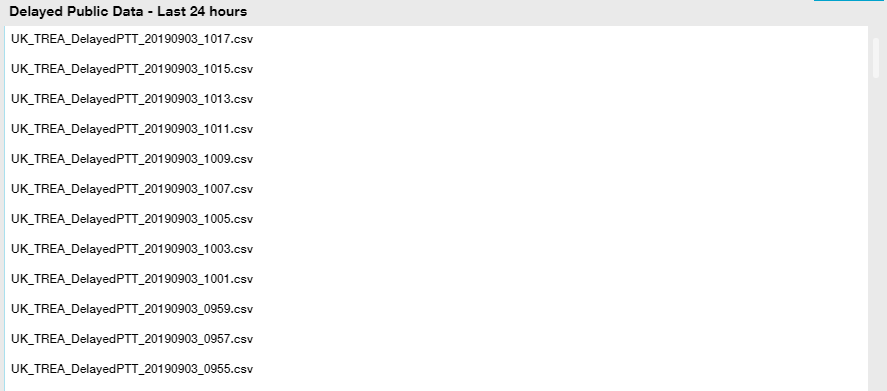

It is therefore vital that public data that is free to access can be aggregated. To do so currently means aggregating across time for a single venue (slice files are typically published), and most importantly aggregating across multiple venues – APAs and Trading Venues.

The Bloomberg APA and MTF make this possible by persisting their slice files and allowing programmatic access to their website. Bravo.

Other APAs do not allow this programmatic access free of charge, making aggregation impossible and making their free post-trade delayed data useless. This does nothing to aid transparency.

3. Arduous data user agreements

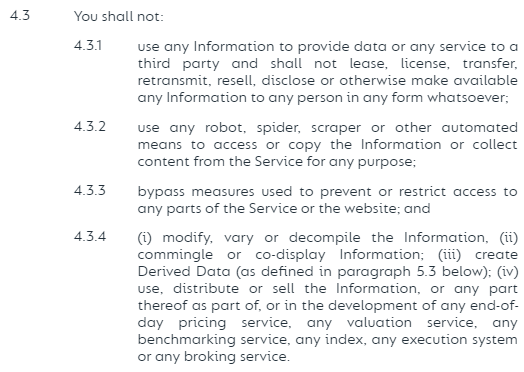

I have lost count of the number of “Click-Through” user agreements that I have blindly accepted just to be able to see data on my screen.

Just reading these agreements alone would be a week’s worth of work. And how do we stay on top of any changes?

The ones I have read make using even delayed post-trade data for anything actually useful completely impossible:

Just to stress – this states that I cannot collect content for ANY purpose?! How can that be?!

I think that ANY reference to delayed, post-trade data should simply be removed from data licences. I understand that existing data vendors don’t want to encroach on their current revenues. This is fair enough from a commercial perspective. But the delayed post-trade data is meant to be free and public. Therefore it needs to be unencumbered to be usable.

4. “Leased Lines”

Only providing data via a Leased Line that the consumer has to pay for, maintain, install and speak to a third party provider about really doesn’t meet the criteria of “public” or “free” to my mind.

It is just putting up a barrier for the sake of it. I cannot think of a particular technological reason for this.

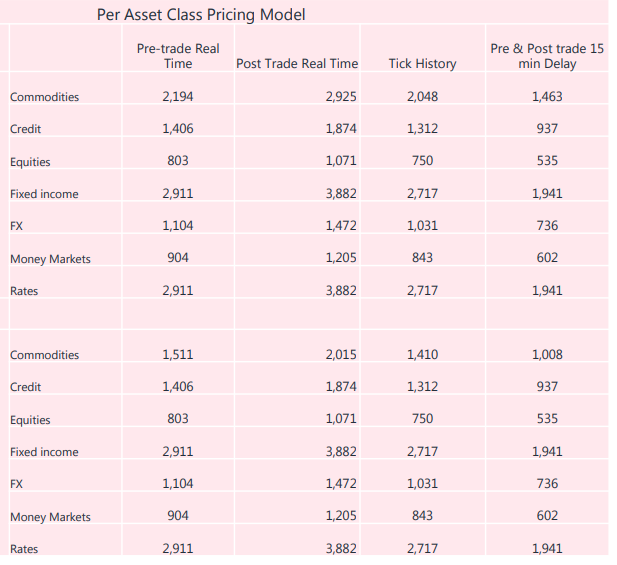

5. Charging for 15 Minute Delayed Data

Prior to MIFID II, I am not aware that any trading venue was making delayed post-trade data for OTC Derivatives available either on a free-to-access or paid-for basis. The practice of monetising this data simply did not exist.

Couldn’t ESMA simply outlaw the final column in this charge card?

This just happened to be the first charge card I downloaded. Many more have similar references to what should be free and public post trade data.

In Summary

We have already lost two years of transparency data in Europe. Delayed, post-trade data was not sold prior to MIFID II for OTC Derivatives.

Therefore, we believe that all APAs and Trading Venues should be providing the data in exactly the same way as Bloomberg.

I hope this blog proves useful for anyone responding to the consultation. The time is now to make ESMA aware of these hurdles to transparency.