I was pulling some data recently out of SDRView and stumbled across some interesting metrics in EUR and GBP swaps. It would seem there has been a proliferation of standardized swaps, traded amongst the US-named business and reported to SDRs.

GET OUR BEARINGS

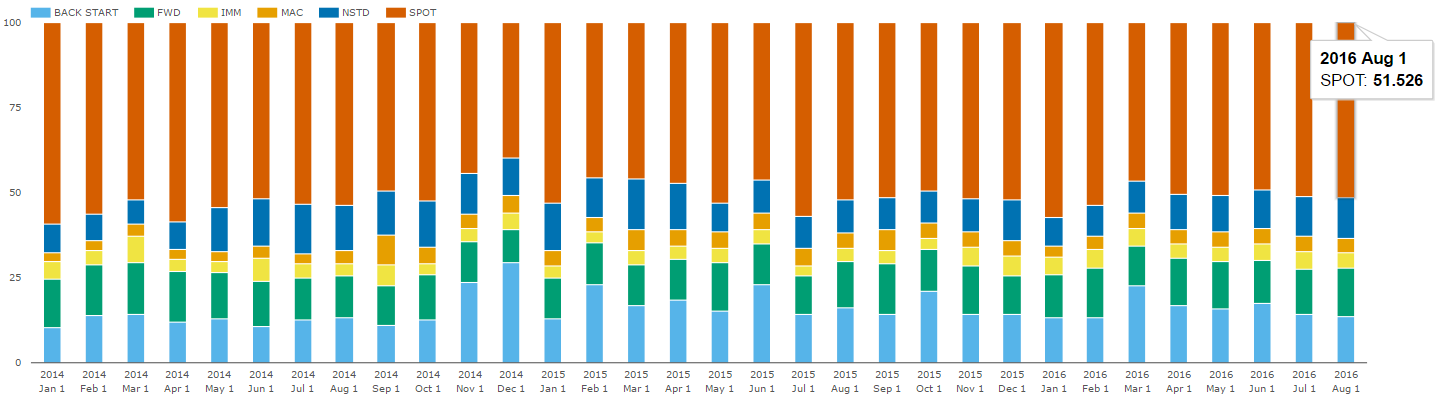

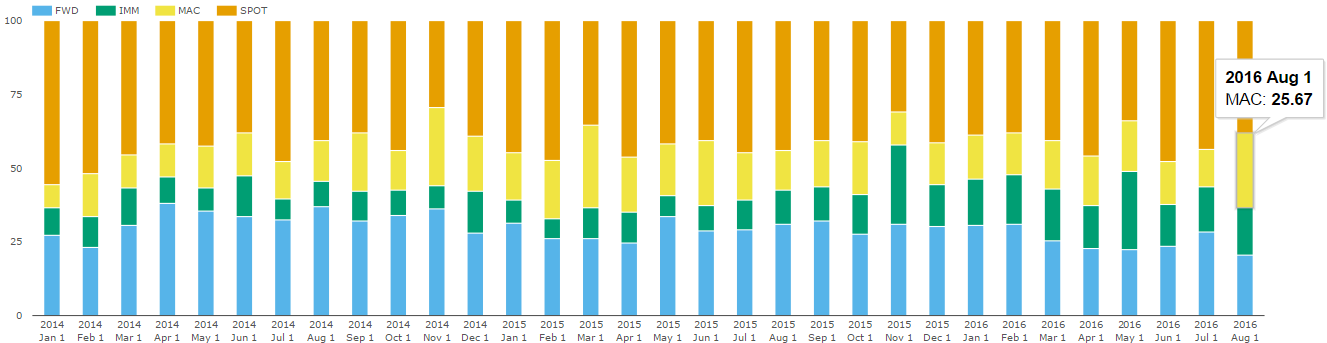

To begin, let’s get our bearings and terminology straight. To do so, I’ll begin with USD swaps. Here is a look at all USD Fixed Float swaps since Jan 2014. This analysis reports by Clarus Subtype:

Let’s remind ourselves what the 6 subtypes are:

- SPOT. This is your vanilla, spot starting swap. As we can see, this accounts for roughly ½ of the USD swap market.

- BACK START. These little devils are the bane of many who try to interrogate the raw data of the SDRs. Generally speaking, these trades of course start on a historical date, often represent lists or packages of trades, and are frequently to do with portfolio cleanup, such as termination or compaction. These are not “price forming” / “new risk” / “risk transfer” trades, depending upon which lingo you prefer.

- NSTD. These “Non-Standard” trades are probably the most tricky to discern. Thankfully they represent a fairly small (~10%) portion of the population. These trades might have various things that effect the economics of the trade, such that the price quoted on the trade is not a par swap rate:

- “Price Effecting Term”. The great SDR catch-all that says “I am not telling you something important about this trade”. Such as an embedded option, notional schedule, rate schedule, etc, etc.

- Up Front Fees.

- Inconsistent payment schedules. Something like 3M Libor that pays every 6M (instead of standard 3M).

- MAC. Standardized, forward IMM start swaps, with standardized coupons.

- IMM. Standardized, forward IMM start swaps, without standardized coupons.

- FWD. All other forward-starting swaps.

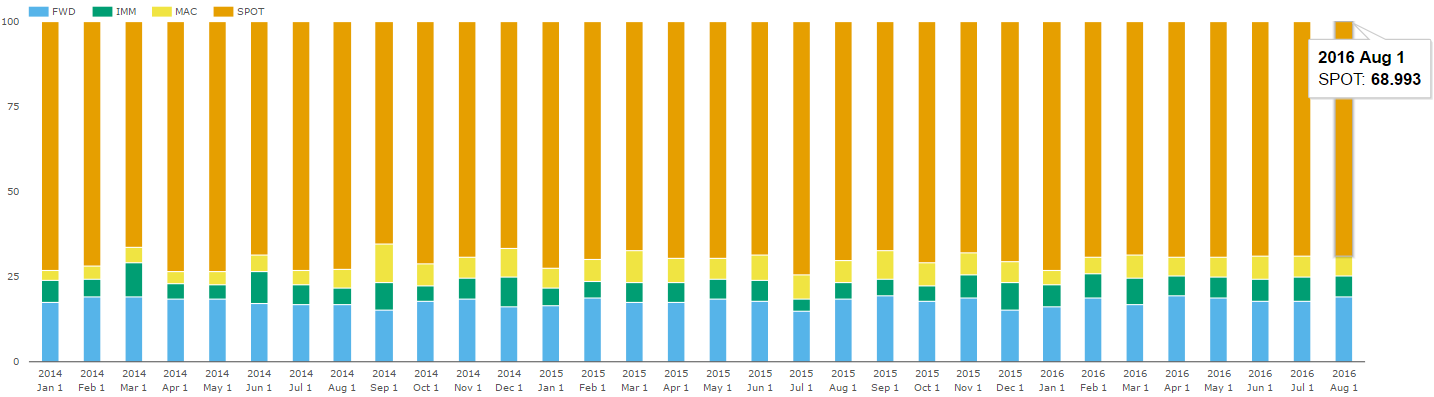

Given all of the above, if we attempt to consolidate our view to price-forming trades, we can remove both the NSTD and BACKSTART subtypes, and get a clearer picture of what is trading in USD swaps:

Perhaps a bit hard to make out, but generally speaking:

- Spot Start hovers right around 70%

- Fwd Start between 15% and 20%

- IMM and MAC swaps bounce between 4% and 10% each, as shown in the diagram below. Not much of a trend.

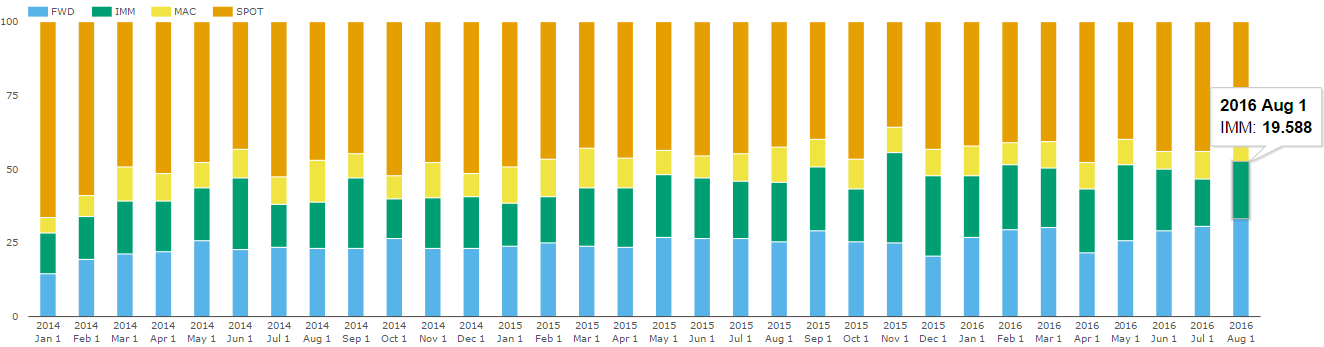

EUR & GBP

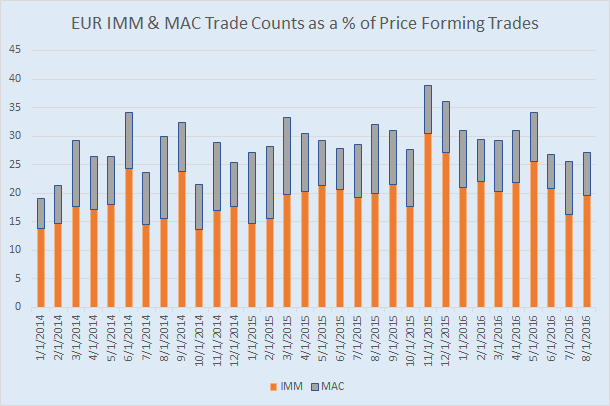

Doing the same with Euro IRS now:

- Spot Start trends down to between 40% and 50% of the market

- Fwd Start trends up slightly to 30%

- IMM and swaps peak at 39%, generally hovering close to 30% of the market

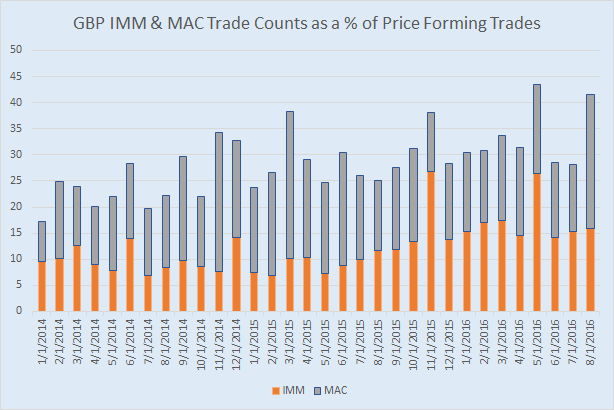

Now for GBP IRS:

- Spot Starting accounts for roughly 40%

- Fwd Start trickled down to 25%

- IMM and MAC swaps touch as high as 43%

SUMMARY & CAVEATS

I was a bit surprised by this data. I should however include a few key caveats:

- This is US SDR-reported trades. So should be considered US-named business. I would not want to extrapolate that the entire EUR and GBP swap market in Europe has a similar profile.

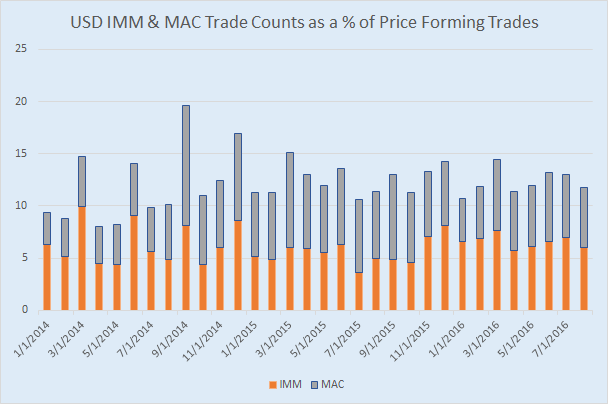

- This analysis was on trade counts. When using trade notional, the story is not as promising. But all that means is that IMM and MAC swaps tend to be smaller in size.

- I haven’t accounted for (removed) packages that are clearly roll trades. Because the IMM and MAC contracts are typically pushed out, this can inflate the amount of transactions. I did however do a quick sanity check and, as you might suspect, it impacts roll months, but it is not terribly significant.

Of course you can use SDRView yourself and tear through the data in much finer detail.

Lastly, I’d note the lack of a significant trend in the data. This has been sitting there for the past couple years, and I’ve been guilty of having my USD blinders on.

Perhaps the charts show a slight pickup in EUR and GBP if you study them closely. If so, this would be good news for the various folks promoting swap futures – CME, Eris, ICE, etc; as the next logical progression from a standardized swap is to an exchange traded future.