- $2.5trn in OIS swaps versus Fed Funds were executed in December 2020.

- This compares to $364bn for SOFR OIS.

- We run through the data for the global market, the US market and the basis swap markets.

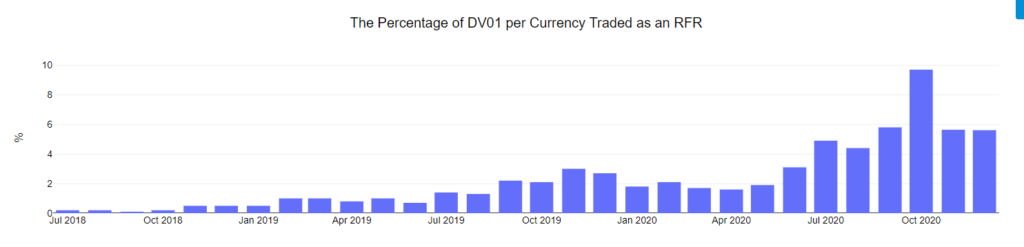

As we continue to compile data for our response to the IBA Cessation of LIBOR consultation, a natural question arises around USD SOFR adoption.

We know from the recently published RFR Adoption Indicator that the past two months have seen over 5.6% of total USD risk traded versus SOFR. This is higher than where we were at the start of 2020, but considerably lower than the discount-driven surge we saw in October 2020:

My take on this is as follows:

- Take-up of USD SOFR is slow.

- The ability of dealer banks to take-down USD SOFR risk is able to scale-up significantly to meet demand.

- The switch to USD discounting has created a new on-going demand for USD SOFR, as discounting risks must be re-hedged when outright rates move.

- However, there has probably not been a demand from other sources looking for SOFR risk management needs.

- Given that the dealer community was successful in scaling-up its risk appetite for SOFR around the discounting switch, this feels to me like clients are not actively transitioning their risk management activities into SOFR yet.

When we calculate our Indicator, we find that the average life of SOFR trades reported to the SDRs is somewhere around 10Y. This speaks to the relatively long-dated nature of discounting hedging needs.

Fed Funds

Of course, SOFR does not exist in a vacuum. USD interest rate risks can be hedged in LIBOR or Fed Funds instruments as well. Whilst the transition story is heavily focused on LIBOR-linked activity, SOFR may well either also:

- Exist in tandem with Fed Funds or;

- See risk management needs transitioning out of Fed Funds into SOFR or;

- Some combination of these two.

Our RFR Adoption Indicator, as per the whitepaper, looks at SOFR adoption relative to both LIBOR and Fed Funds trading, both of which we consider “legacy” rates.

Whilst we spend a lot of time focusing on the LIBOR aspect of this in USD terms, I thought it was also worth highlighting that the Fed Funds derivatives market continues to be orders of magnitude larger than SOFR.

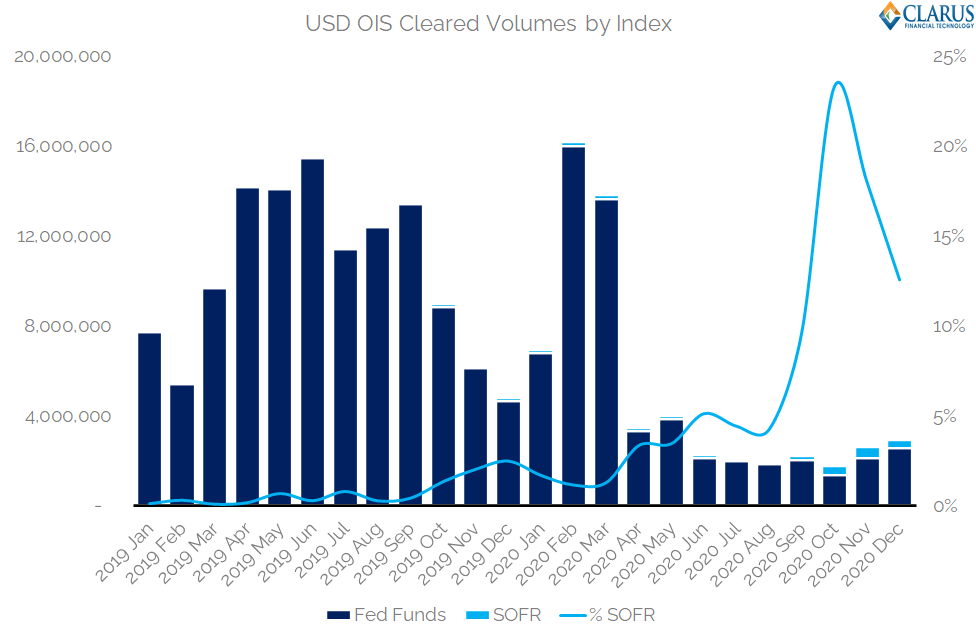

Fed Funds Global Cleared Volumes

For example, simply looking at the notional amounts cleared across CCPs in Fed Funds and SOFR related products shows a huge preference from market participants for Fed Funds related risks:

Showing;

- 57 times more notional was transacted in OTC Fed Funds OIS at CCPs last year than in SOFR!

- Of these OIS-related trades, October saw 23% of total OIS notional transacted in SOFR.

- This has since dropped off to 18% (November) and 12.5% (December).

- This is measured on a notional basis, therefore is somewhat skewed in favour of USD Fed Funds which sees relatively more short-dated activity than SOFR.

- However, this should be a much simpler transition story. If market participants are already transacting compounded in-arrears OIS, why isn’t more of the Fed Funds market actively choosing SOFR as the preferred rate?

- I have looked at the intricacies of the Fed Funds fixing itself in a previous blog here.

- Equally, the intricacies of the SOFR fixing can be found in a previous blog here.

Suffice today, both fixings have their “quirks”. Swapping from one to the other should be less impactful from a risk management perspective than moving from LIBOR to SOFR. And yet, from a notional-traded perspective, this transition has been depressingly slow.

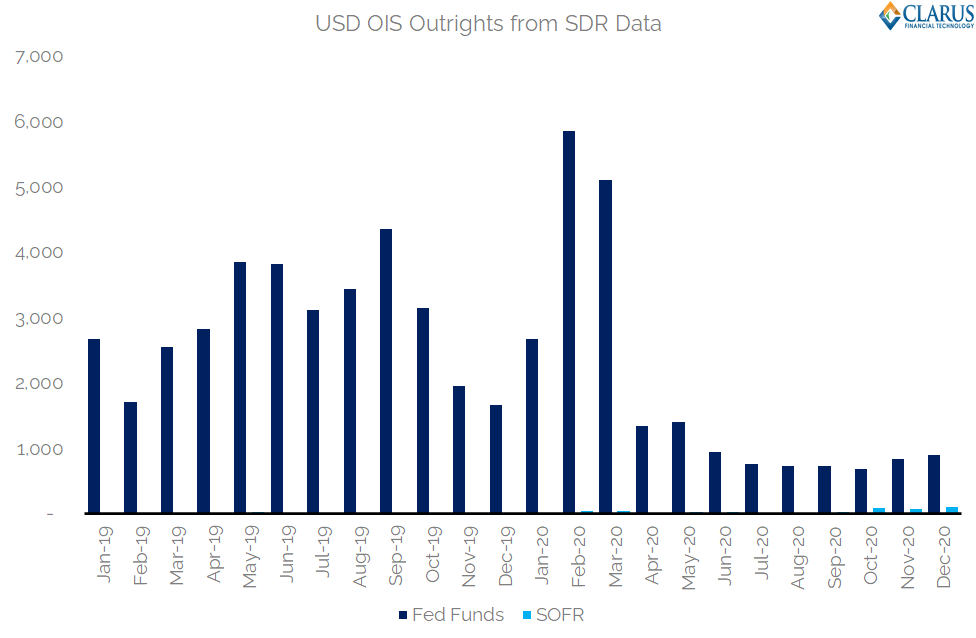

Fed Funds US Market Activity

To shed a bit more analysis on what might be happening in SOFR relative to Fed Funds volumes, I turned to the US-market SDR data. Whilst delivering insights on a (sizable) portion of the global market, SDR data also allows us more granularity into the exact trading activity.

For example, looking at outright OIS only, we find that SOFR is completely dwarfed by Fed Fund trading:

- Fed Fund trading is clearly hugely sensitive to the overall Rates environment. Volumes have dropped off a cliff since rates were cut to zero last year.

- Under ZIRP, it is therefore positive for SOFR volumes that they have managed to grow at all. This shows some positive signs for the transition story.

- In December 2020, notional volumes in Fed Funds swaps reported to US SDRs were 8 times larger than SOFR volumes. That is a much more positive metric than we were able to present for global cleared volumes across the whole of 2020 (57 times!).

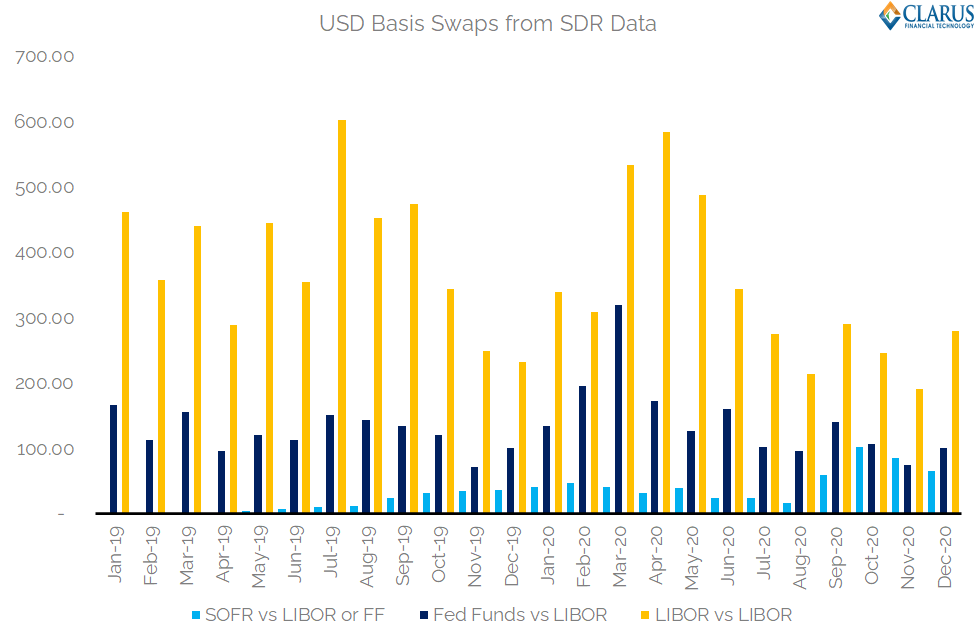

Fed Funds and SOFR Basis Swaps

Finally, as we have stated, OIS do not exist in a vacuum. Basis swaps are alive and kicking, allowing market participants to swap between different floating rates of interest.

The relative activity in basis swaps, as reported to US SDRs, is striking:

Showing;

- Basis swaps involving a SOFR leg were larger than Fed Funds basis swaps in both October and November 2020. This is a very positive sign.

- However, in December 2020, Fed Funds vs LIBOR was a larger generator of notional than SOFR basis swaps. Maybe this is a blip around year-end hedging needs, but it should be monitored.

- The elephant in the room, however, is the continued huge use of LIBOR vs LIBOR basis. These do nothing for the transition story, other than help hedge risks associated with the precise fixing of the fallback spreads.

We hope that all of this LIBOR-LIBOR basis activity is centred on decreasing transition risks, rather than speculative trading centred on profiting from the precise calibration of fallback spreads. Maybe that is too naïve when we operate in a low volatility environment and any opportunity to benefit from rate moves needs to be leveraged?

In Summary

- The Fed Fund swaps market continues to be about 7 times larger than the SOFR swaps market in notional terms.

- This is the case across most metrics, although basis swaps involving a SOFR leg (admittedly also including SOFR vs Fed Funds!) has been the second largest basis swap market in some months.

- From a transition perspective, it is surprising how large the LIBOR vs LIBOR basis swap market continues to be. Is this all related to hedging the calibration risk versus the historic spread?