Anonymous Trading on SEFs

The 1st November 2020 heralded a fundamental change in swaps markets. SEFs executing trades in specific products were no longer permitted to disclose the identities of the counterparties (to each other) after the trade: At the moment, this rule only applies to MAT swaps – i.e. those products subjected to the execution mandate and required […]

SOFR Swaps on SEFs

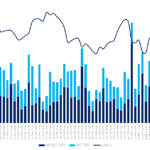

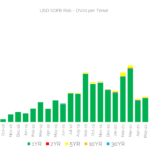

Last week I looked at Swap Volumes in October 2020 and focused primarily on SOFR Swaps and Futures at Clearing Houses, so this week I am going to look at Swap Execution Facilities (SEFs). D2D SEFs Let’s start by using SEFView to look at D2D SEFs, where the main product is SOFR v FedFunds Basis […]

ISDA-Clarus RFR Indicator: SOFR, So Good

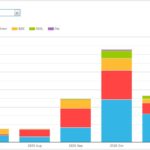

The ISDA-Clarus RFR Adoption Indicator has been published for October 2020. The headlines are: The RFR Adoption Indicator hit 11.6%, a new all time high. This was up from 10.5% the prior month. 9.7% of all USD risk was traded in SOFR vs 5.8% last month, reflecting the increase in SOFR activity as a result of the CCP discounting change. […]

Swap Volumes in October 2020

In the transition from LIBOR to SOFR, the recent change by Clearing Houses to discount swaps using a SOFR curve instead of a FedFunds curve has long been trailed as a key milestone for higher volumes in SOFR derivatives. In today’s blog I look at how SOFR Swap volumes did in October 2020. I also […]

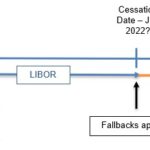

Libor pre-cessation announcement – risk challenges for non-cleared derivatives

In August I looked at the potential for valuation challenges as for non-cleared derivatives. This month I will cover the additional challenges for risk management and reporting that would arise with a pre-cessation announcement. A LIBOR pre-cessation announcement from the FCA could occur by the end of 2020. This was first discussed publicly in June […]

Libor Fallback Trade Valuations – A single trade example

As the financial industry moves towards the replacement of LIBOR the question asked is changing from what does IBOR Reform mean, to how I manage IBOR reform? A key subsequent question is “What is the change in value/change in risk of my LIBOR trade if it goes onto Fallbacks?” I thought that it would be […]