The Unintended Consequences of Uncleared Margin Rules

or Are UMRs an economic mandate for clearing? Since the introduction of Uncleared Margin Rules six months ago, there has been an increase in Clearing across many markets. We have seen the proportion of trades being cleared across NDFs, OIS, Latam and Inflation Swaps increase significantly. This increase in clearing has been accompanied by an […]

Microservices: FRTB Modellable Risk Factors

FRTB regulations specify that non-modellable risk factors are subject to stressed capital add-ons For a risk factor to be modellable it must pass a specific test for continuously available real prices The Clarus API provides functions for the risk factor modellability test for OTC Derivatives These functions are very easy to call from many popular languages, […]

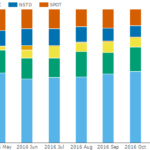

Fed Rate Hikes Are Reducing The Average Life Of USD Swaps

The average maturity of USD OIS swaps has reduced significantly in recent months. OIS swaps now make up almost 20% of all traded risk in USD swaps, up from less than 5% in 2014. As a result of increasing volumes in OIS and their very short maturity, a significant reduction in overall average maturity is […]

Are SEF’s Executing More Non-MAT Trades?

Today we look at any trends in bespoke Fixed/Float swap trading On-SEF. Last year I wrote an article about the longer term trends in the US swaps market by asking “What is Left off-SEF?” We determined that, generally speaking, 2/3rds of the USD Fixed/Float swap market is On-SEF. The Off-SEF world was generally a bunch of […]

Microservices: An FpML Cashflow Generator

The Clarus API has a function to generate cashflows from an FpML description of a trade. The function is very easy to call from many popular languages, including Python, R, Julia, C++, and Java. Many related functions are available, see our API documentation. Calling directly in the browser To appreciate the ease with which the […]

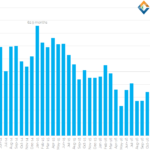

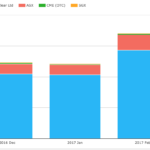

February 2017 Swaps Review

Continuing with our monthly Swaps review series, let’s look at volumes in February 2017. Summary: SDR USD IRS price-forming volume > $2 trillion gross notional 8% lower than a year earlier On SEF vs Off SEF at 65% to 35% SEF Compression activity in USD IRS > $230 billion USD OIS volume at > $3.3 trillion is massively up (3 times Feb […]

House Residual Interest

We often monitor the FCM data within the US, primarily to gauge our quarterly FCM rankings (eg Year End 2017). Avid students of the FCM data will also know that besides sheer customer margins and customer funds reporting, these reports also reveal how much excess funds the FCM’s carry alongside the customer funds (aka Residual […]

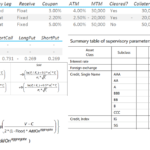

SA-CCR – Explaining the Calculations

Background In March 2014, the Basel Committee on Banking Supervision published bcbs279, the Standardised Approach for measuring Counterparty Credit Risk exposures. SA-CCR replaces the current non-internal model approaches, the Current Exposure Method (CEM) of 1995 and the Standardised Method (SM) of 2005. The majority of banks currently use CEM as relatively few firms have Internal Model Method (This blog […]

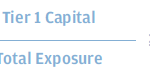

Basel III Leverage Ratio

The Basel III Leverage Ratio, often referred to as the Supplementary Leverage Ratio (SLR), is one of the important new metrics introduced as a response to the Financial Crisis of 2007-08 and one which continues to receive a lot of press coverage and discussion. In this article I will provide an overview and some of the […]

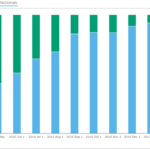

NDF Trading After 1st March

Open Interest of NDFs has set new records recently. Volumes have continued to be elevated compared to 2016. We have not seen a significant change in behaviour since the 1st March VM big bang. Overall, we estimate 15% of the entire market is now cleared. Up to 35% of D2D volumes are being cleared during any […]