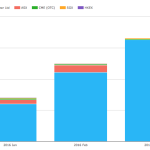

March 2016 Swaps Review

Continuing with our monthly review series, let’s take a look at Interest Rate Swap volumes in March 2016. First the highlights: On SEF USD IRS in March 2016 volume was > $1.25 trillion For price forming trades, DV01 was 10% lower than Feb 2016 Butterfly trade volumes were up and Outright volumes were down USD SEF Compression volumes were exceptional at >$240 billion On SEF vs […]

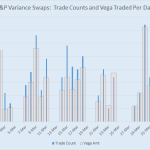

Variance Swaps and Other Equity Derivatives on SDR

You’re likely aware that we’ve been the de-facto “janitors” of the SDR data. However, to date, our focus has been on swaps traded in Interest Rates, Credit, and FX. This week I turned to the world of equity derivatives to see what’s lurking in there. To begin with, I had to grab some raw data. […]

How to identify the CCP of trades from the SDR data

We use Linear Regression on price time-series to identify discontinuities in price These discontinuities represent jumps in price We use these jumps to identify which USD IRS trades are cleared at CME This allows us to extract yet further information from the publicly reported data The methodology is dynamic, and therefore is suitable across a range of products and maturities Forecasting Swap Prices […]