Our Top Blog Articles of 2015

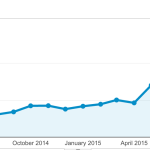

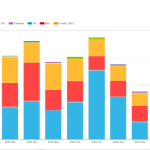

For my last blog article of 2015, I thought it would be appropriate to highlight our top blogs of the year. Like many firms we use Google Analytics to collect web traffic statistics, so lets see what this data shows. Website Users Lets start with a chart of users visiting our website. Showing: Monthly users to www.clarusft.com from […]

Fed Surprise Indicators

We use price and volume data to measure the “surprise factor” of the Fed’s rate hike last week OIS volumes were impressive, near to the highest day all year… …with evidence of a preference towards cash-settling derivative trades We suggest different ways of using the volume data to measure the degree of surprise in the […]

Compression in Swaps

We run a real compression exercise through CHARM… …showing the potential IM reduction from a compression run Depending on the exact portfolio, the ratio of NPV unlocked to the IM released can be highly variable…. …taking a recursive process to accurately assess your capital efficiency. This is exactly why pre-trade analysis of Compression using high quality, high performance engines such […]

Cap and Floor Option Volumes

For a while now I have wanted to look into more detail at Caps and Floors, which are an important but little commented on product type. So it is seems appropriate as we near first the Federal Reserve rate rise since June 2006, to look at a product designed to set a Cap (or Floor) […]

Cap Floor のボリューム

ここしばらくの間、CAP・Floorについてより詳細に調べたいと思っていた。CAP・Floorは重要でありながらあまりコメントされていなかったからだ。2006年6月以来のFRBによる利上げを控える今、将来の金利に上限あるいは下限をセットするためにデザインされたプロダクトを見ておくことは適切だろう。

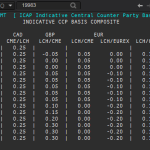

CCP Basis Spreads: What Next?

Given the recent activity in CME-LCH Basis Spreads (see November review or Spreads Blow Out), we often get asked what further developments we see happening and specifically whether a basis will manifest between non-USD currencies and between other Clearing Houses. This article will look at both of these questions. Indicative CCP Basis Quotes Lets start with a […]

Is that a fair price? Measuring Swap Execution

Can we develop a way to understand and measure the execution of any trade? We look at the relationship between Tick Size and Trade Size. The price impact of a trade does vary with trade size…. …therefore a quantitative measure for execution quality is the natural next step. Revisiting the concept of Tick Sizes in USD Swaps, we are going to […]

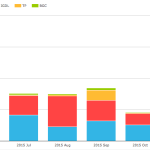

November 2015 Swaps Review – CME-LCH Basis Up, LCH Vols Up, SEF Compression Down

Continuing with our monthly review series, let’s take a look at Interest Rate Swap volumes in Nov 2015. First the highlights: On SEF USD IRS Nov 2015 volume was similar to Oct 2015 and up 25% compared to Nov 2014 USD SEF Compression volumes were down 50% from Oct and the lowest since April 2015 GBP & EUR […]

What did the Australian Regulators say about OTC Derivatives Trading Mandates?

I read last month with interest the report on the Australian OTC Derivatives Market issued by the Council of Financial Regulators (which includes Australian regulators APRA, ASIC, RBA and The Treasury). The full report of which can be found here. Given we already know a lot about the Trade Reporting and Central Clearing developments, I […]

SEF Trading on US Holidays

EUR swaps trading is intriguing on US holidays We don’t have many data points to play with… ….but the data shows continued EUR Swap activity on-SEF on US Holidays. Of this activity, much of it is client trading, which I find surprising. These volumes naturally filter into the data for Client Clearing at LCH on US Holidays.. […]