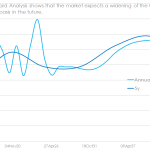

CME-LCH Basis – What does the Term Structure tell us?

We analyse the CME-LCH Basis volumes by tenor and look at what the forward curve implies for prices in the future. There are no signs of normalisation trades in the market, with the basis widening over the past week. We suggest some thoughts as to how this may play out for other Currencies and other […]

Hedging the CME-LCH Basis

Following on from my article on the CME-LCH Basis Spread, I will now look into the details of hedging this basis with CCP Switch trades. Example Portfolio Lets start by constructing an example portfolio of USD Swaps in which we are net receivers in our account at CME and net payers at LCH. Using CHARM […]

CME-LCH Basis Spread

Recently I noticed that the view statistics for my June 2014 blog on LCH-CME Switch Trades were running at 5 times their weekly average, which I thought was odd. Then on 15-May, I read the Risk article, Bank swap books suffer as CME-LCH basis explodes (subs required) and I understood why. So a good time to re-visit this […]

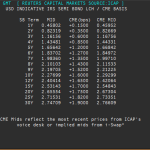

CFTC Swap Success (In Pictures)

They say a picture is worth a thousand words. But if you are like me, it’s hard to quantify, because getting through 1,000 words can be quite tough. By the 100th word you’re skipping ahead to find the bulletpoints, bolded sections, and charts. It occurred to me recently that we at Clarus have reams of data, […]

Mechanics of Asset Swaps and Government Bond Swap Spreads

Last week we looked at the US Markets and Spreadovers, that trade as a spread to underlying US Treasury bonds. These are not the only structures that trade in the market. Other currencies and other strategies yield a variety of alternate structures. Matched Maturity Asset Swap In some markets, government bond issuance is nowhere near as frequent as in […]

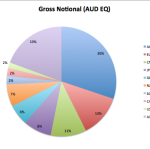

Derivatives Trade Reporting in Australia

Following on from my prior article looking at Canadian Derivatives Reporting to SDRs, I thought I would look next at Australia. The Australian Securities & Investments Commission (ASIC) Derivatives Transaction Reporting requirements began as follows: Phase 1 firms (Swap Dealers) in October 2013 Phase 2 firms in April 2014 and October 2014 Phase 3 firms in April […]

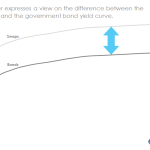

Mechanics and Definitions of Spreadovers (Swap Spreads)

We define the characteristics and mechanics of a Spreadover or Swap Spread (“U.S. Dollar Swap Spread” in CFTC parlance). The inclusion of Spreadovers in our SDR products allows us to look at the volume of Swaps that are traded as a spread to Government Bonds. Spreadover Definition Trading strategy; to take a view on the difference in rates between an Interest Rate Swap and […]

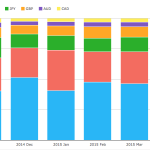

April 2015 Review – Lower Volumes

Continuing with our monthly review series, let’s take a look at Interest Rate Swap volumes in April 2015. First the highlights: April 2015 volumes were the lowest since November 2014 However 2015 YTD volume are up 47% from the same period in 2014 SEF Compression volumes were also down from March FOMC meeting on April 28-29 once again […]

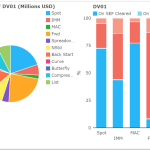

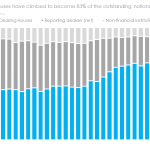

BIS and Clarus Data: The $200 trillion reconciliation

What is the relationship between Clarus data and the Bank for International Settlements (BIS) data? It is a great question to ask. On the whole, BIS data is delayed by nearly six months; Clarus data is available in close to real-time. For Cleared swaps, CCPView data is easily reconciled to the BIS and is shown to be virtually identical. This […]