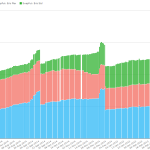

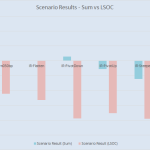

Comparing OTC and Futures Data

Recently we introduced exchange traded derivatives in CCPView, allowing us the ability to start exploring this world alongside the OTC market more holistically. Many of you know we already track some futures in SEFView, however the universe in SEFView is SEF-executed trades; whereas in CCPView we can now look at the entire world of cleared derivatives. […]

FX NDF Trading On SEFs: April 2015 Update

It is more than a year since I last looked at FX NDF Trading On SEFs (Jan 2014) and as that was one of our Top 10 Blogs of 2014, it is long overdue for me to see What the Data Shows. April 2015 Lets start with SDRView and the latest volumes in the four largest currency […]

Data Visualisation for Swaps – a Tufte Approach

Data visualisation is meant to take something complex and make it simple and easy to understand. When I saw this in a blog recently, I immediately thought “Hey, that’s what Clarus do!” Interest piqued, I’ve begun delving into the fast-evolving field. As a Swaps-trader for over ten years, this aspect of the industry pretty much […]

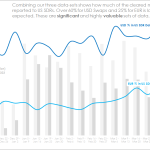

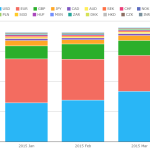

What percentage of the market is in the US SDR data?

We analyse the SDR data in light of the whole market in the cleared Rates space. SDR data is shown to represent over 60% of total-market volumes at a trade-by-trade level. That’s huge! It’s funny how times change. Next month, the BIS will update their semi-annual review of OTC Derivatives. As recently as 2013 I would have to (manually) […]

Canadian Derivatives Reporting to SDRs

Following on from my earlier articles looking at European Trade Reporting and OTC Derivatives Reporting in Japan, I thought I would look at other jurisdictions starting with Canada. Canadian reporting came into force for Dealers on 31 October 2014 and for Non-Dealers will do so on 30 June 2015. Overview of Requirements Key points: OTC Derivatives […]

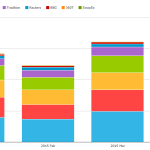

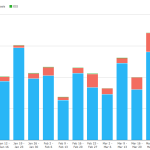

March 2015 Review – Bloomberg out in front

Bloomberg are #1 for SEF liquidity in Q1 2015 whilst Tradeweb saw the highest overall volumes. We saw record USD Swap volumes reported to the SDRs in March 2015, with our review highlighting increasing compression activity. The great month for the industry was rounded-out with over 60% of volumes traded across a SEF. USD IRS On-SEF $1.56trn in notional traded across SEFs during March […]

SEFs in Japan

The G20 commitment of 2009 that “all standard OTC Derivative contracts should be traded on exchanges or electronic platforms” has so far only been implemented in the United States where Swap Execution Facilities (SEFs) have been live since October 2013. In this article I will look at the situation in Japan. Background First lets start with […]

CDS Clearing Data

A few times last week I heard concerns about whether clearing of Single Name CDS will ever take off. It inspired me to examine the data we have on hand for credit derivatives, both index and Single Name, to see what I can make of it. While we’ve written lots of articles on OTC swaps, […]

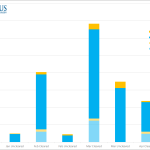

CFTC Residual Interest (and other FCM data)

Much has been written about the demise of the FCM in America. I pulled some numbers to see if I could get my head around it, and to check on the overall health of the ones that remain. CFTC Data The foundation for my analysis is the CFTC monthly reporting showing the capital requirements and amount of funds on […]

OIS Swap Nuances

Overnight Indexed Swaps (OIS) are fixed-float swaps where the floating leg index is a compounded overnight interest rate. For short dated swaps, those less than 1Y, the coupon structure is usually zero coupon. For longer dated swaps, the fixed leg has a similar structure as the fixed leg on a regular LIBOR swap. Some of […]